| ||

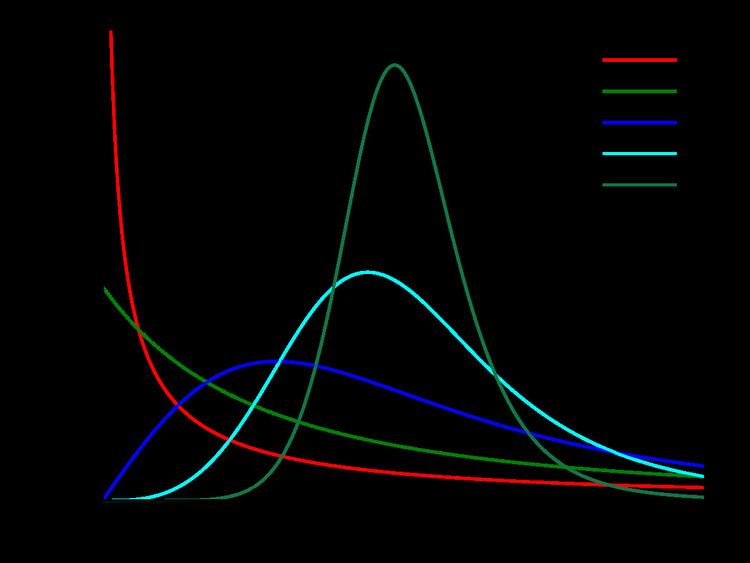

Support x ∈ [ 0 , ∞ ) {\displaystyle x\in [0,\infty )} PDF ( β / α ) ( x / α ) β − 1 ( 1 + ( x / α ) β ) 2 {\displaystyle {\frac {(\beta /\alpha )(x/\alpha )^{\beta -1}}{\left(1+(x/\alpha )^{\beta }\right)^{2}}}} CDF 1 1 + ( x / α ) − β {\displaystyle {1 \over 1+(x/\alpha )^{-\beta }}} Mean α π / β sin ( π / β ) {\displaystyle {\alpha \,\pi /\beta \over \sin(\pi /\beta )}} if β > 1 {\displaystyle \beta >1} , else undefined Median α {\displaystyle \alpha \,} | ||

In probability and statistics, the log-logistic distribution (known as the Fisk distribution in economics) is a continuous probability distribution for a non-negative random variable. It is used in survival analysis as a parametric model for events whose rate increases initially and decreases later, for example mortality rate from cancer following diagnosis or treatment. It has also been used in hydrology to model stream flow and precipitation, in economics as a simple model of the distribution of wealth or income, and in networking to model the transmission times of data considering both the network and the software.

Contents

- Characterisation

- Alternative parameterization

- Moments

- Quantiles

- Survival analysis

- Hydrology

- Economics

- Networking

- Related distributions

- Generalizations

- References

The log-logistic distribution is the probability distribution of a random variable whose logarithm has a logistic distribution. It is similar in shape to the log-normal distribution but has heavier tails. Unlike the log-normal, its cumulative distribution function can be written in closed form.

Characterisation

There are several different parameterizations of the distribution in use. The one shown here gives reasonably interpretable parameters and a simple form for the cumulative distribution function. The parameter

The cumulative distribution function is

where

The probability density function is

Alternative parameterization

An alternative parametrization is given by the pair

Moments

The

where B() is the beta function. Expressions for the mean, variance, skewness and kurtosis can be derived from this. Writing

and the variance is

Explicit expressions for the skewness and kurtosis are lengthy. As

Quantiles

The quantile function (inverse cumulative distribution function) is :

It follows that the median is

Survival analysis

The log-logistic distribution provides one parametric model for survival analysis. Unlike the more commonly used Weibull distribution, it can have a non-monotonic hazard function: when

The survival function is

and so the hazard function is

Hydrology

The log-logistic distribution has been used in hydrology for modelling stream flow rates and precipitation.

Extreme values like maximum one-day rainfall and river discharge per month or per year often follow a log-normal distribution. The log-normal distribution, however, needs a numeric approximation. As the log-logistic distribution, which can be solved analytically, is similar to the log-normal distribution, it can be used instead.

The blue picture illustrates an example of fitting the log-logistic distribution to ranked maximum one-day October rainfalls and it shows the 90% confidence belt based on the binomial distribution. The rainfall data are represented by the plotting position r/(n+1) as part of the cumulative frequency analysis.

Economics

The log-logistic has been used as a simple model of the distribution of wealth or income in economics, where it is known as the Fisk distribution. Its Gini coefficient is

Networking

The log-logistic has been used as a model for the period of time beginning when some data leaves a software user application in a computer and the response is received by the same application after travelling through and being processed by other computers, applications, and network segments, most or all of them without hard real-time guarantees (for example, when an application is displaying data coming from a remote sensor connected to the Internet). It has been shown to be a more accurate probabilistic model for that than the log-normal distribution or others, as long as abrupt changes of regime in the sequences of those times are properly detected.

Related distributions

Generalizations

Several different distributions are sometimes referred to as the generalized log-logistic distribution, as they contain the log-logistic as a special case. These include the Burr Type XII distribution (also known as the Singh-Maddala distribution) and the Dagum distribution, both of which include a second shape parameter. Both are in turn special cases of the even more general generalized beta distribution of the second kind. Another more straightforward generalization of the log-logistic is the shifted log-logistic distribution.