| ||

Parameters η , b > 0 {\displaystyle \eta ,b>0\,\!} Support x ∈ [ 0 , ∞ ) {\displaystyle x\in [0,\infty )\!} PDF b η e b x e η exp ( − η e b x ) {\displaystyle b\eta e^{bx}e^{\eta }\exp \left(-\eta e^{bx}\right)} CDF 1 − exp ( − η ( e b x − 1 ) ) {\displaystyle 1-\exp \left(-\eta \left(e^{bx}-1\right)\right)} Mean ( 1 / b ) e η Ei ( − η ) {\displaystyle (1/b)e^{\eta }{\text{Ei}}\left(-\eta \right)} where Ei ( z ) = ∫ − z ∞ ( e − v / v ) d v {\displaystyle {\text{where Ei}}\left(z\right)=\int \limits _{-z}^{\infty }\left(e^{-v}/v\right)dv} Median ( 1 / b ) ln [ ( − 1 / η ) ln ( 1 / 2 ) + 1 ] {\displaystyle \left(1/b\right)\ln \left[\left(-1/\eta \right)\ln \left(1/2\right)+1\right]} | ||

In probability and statistics, the Gompertz distribution is a continuous probability distribution, named after Benjamin Gompertz (1779 - 1865). The Gompertz distribution is often applied to describe the distribution of adult lifespans by demographers and actuaries. Related fields of science such as biology and gerontology also considered the Gompertz distribution for the analysis of survival. More recently, computer scientists have also started to model the failure rates of computer codes by the Gompertz distribution. In Marketing Science, it has been used as an individual-level simulation for customer lifetime value modeling. In network theory, particularly the Erdős–Rényi model, the walk length of a random self-avoiding walk (SAW) is distributed according to the Gompertz distribution.

Contents

Probability density function

The probability density function of the Gompertz distribution is:

where

Cumulative distribution function

The cumulative distribution function of the Gompertz distribution is:

where

Moment generating function

The moment generating function is:

where

Properties

The Gompertz distribution is a flexible distribution that can be skewed to the right and to the left. Its hazard function is a convex function of

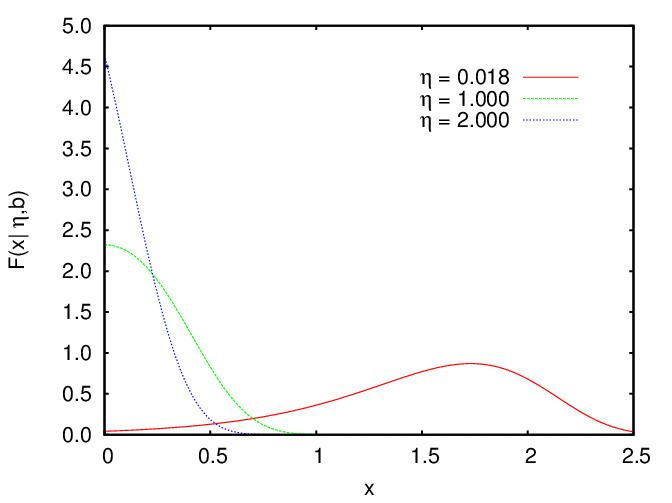

Shapes

The Gompertz density function can take on different shapes depending on the values of the shape parameter

Kullback-Leibler divergence

If

where