| ||

In the United States of America, individuals and corporations pay U.S. federal income tax on the net total of all their capital gains. The tax rate depends on both the investor's tax bracket and the amount of time the investment was held. Short-term capital gains are taxed at the investor's ordinary income tax rate and are defined as investments held for a year or less before being sold. Long-term capital gains, on dispositions of assets held for more than one year, are taxed at a lower rate.

Contents

- Current 2016 law

- Additional taxes

- Cost basis

- Depreciation

- Inherited property

- Capital losses

- Return of capital

- History

- Summary of recent history

- Incidence

- Existence of the tax

- Preferential rate

- Holding period

- Carried interest

- Effects

- Measuring the effect on the economy

- Factors that complicate measurement

- Strategic losses

- Versus purchase

- Primary residence

- Deferral strategies

- Simpson Bowles

- In the 2016 campaign

- References

Current (2016) law

As of 2016, the United States taxes short-term capital gains at the same rate as it taxes ordinary income. Long-term capital gains are taxed at generally lower rates, shown in color in the table below:

The dollar amounts ("tax brackets") are adjusted each year based on inflation, and are after deductions and exemptions, which means that there is another bracket, of income below that shown as $0 in the table, on which no tax is due.

Additional taxes

There may be taxes in addition to the tax rates shown in the above table.

However, capital gains do not push ordinary income into a higher income bracket. The Capital Gains and Qualified Dividends Worksheet in the Form 1040 instructions puts both of these types of income into a tax bracket as though they were the last income received, then applies the lower capital gains tax rate as shown in the above table.

Cost basis

The capital gain that is taxed is the excess of the sale price over the cost basis of the asset. The taxpayer reduces the sale price and increases the cost basis (reducing the capital gain on which tax is due) to reflect transaction costs such as brokerage fees, certain legal fees, and the transaction tax on sales.

Depreciation

In contrast, when a business is entitled to a depreciation deduction on an asset used in the business (such as for each year's wear on a piece of machinery), it reduces the cost basis of that asset by that amount, potentially to zero. The reduction in basis occurs whether or not the business claims the depreciation.

If the business then sells the asset for a gain (that is, for more than its adjusted cost basis), this part of the gain is called depreciation recapture. When selling certain real estate, it may be treated as capital gain. When selling equipment, however, depreciation recapture is generally taxed as ordinary income, not capital gain. Further, when selling some kinds of assets, none of the gain qualifies as capital gain.

Inherited property

Under the stepped-up basis rule, for an individual who inherits a capital asset, the cost basis is "stepped up" to its fair market value of the property at the time of the inheritance. When eventually sold, the capital gain or loss is only the difference in value from this stepped-up basis. Increase in value that occurred before the inheritance (such as during the life of the decedent) is never taxed.

Capital losses

If a taxpayer realizes both capital gains and capital losses in the same year, the losses offset (cancel out) the gains. The amount remaining after offsetting is the net gain or net loss used in the calculation of taxable gains.

For individuals, a net loss can be claimed as a tax deduction against ordinary income, up to $3,000 per year ($1,500 in the case of a married individual filing separately). Any remaining net loss can be carried over and applied against gains in future years. However, losses from the sale of personal property, including a residence, do not qualify for this treatment.

Corporations with net losses of any size can re-file their tax forms for the previous three years and use the losses to offset gains reported in those years. This results in a refund of capital gains taxes paid previously. After the carryback, a corporation can carry any unused portion of the loss forward for five years to offset future gains.

Return of capital

Corporations may declare that a payment to shareholders is a return of capital rather than a dividend. Dividends are taxable in the year that they are paid, while returns of capital work by decreasing the cost basis by the amount of the payment, and thus increasing the shareholder's eventual capital gain. Although most qualified dividends receive the same favorable tax treatment as long-term capital gains, the shareholder can defer taxation of a return of capital indefinitely by declining to sell the stock.

History

From 1913 to 1921, capital gains were taxed at ordinary rates, initially up to a maximum rate of 7 percent. The Revenue Act of 1921 allowed a tax rate of 12.5 percent gain for assets held at least two years. From 1934 to 1941, taxpayers could exclude percentages of gains that varied with the holding period: 20, 40, 60, and 70 percent of gains were excluded on assets held 1, 2, 5, and 10 years, respectively. Beginning in 1942, taxpayers could exclude 50 percent of capital gains on assets held at least six months or elect a 25 percent alternative tax rate if their ordinary tax rate exceeded 50 percent. From 1954 to 1967, the maximum capital gains tax rate was 25 percent. Capital gains tax rates were significantly increased in the 1969 and 1976 Tax Reform Acts. In 1978, Congress reduced capital gains tax rates by eliminating the minimum tax on excluded gains and by increasing the exclusion to 60 percent, thereby reducing the maximum rate to 28 percent. The 1981 tax rate reductions further reduced capital gains rates to a maximum of 20 percent.

The Tax Reform Act of 1986 repealed the exclusion of long-term gains, raising the maximum rate to 28 percent (33 percent for taxpayers subject to phaseouts). When the top ordinary tax rates were increased by the 1990 and 1993 budget acts, an alternative tax rate of 28 percent was provided. Effective tax rates exceeded 28 percent for many high-income taxpayers, however, because of interactions with other tax provisions. The new lower rates for 18-month and five-year assets were adopted in 1997 with the Taxpayer Relief Act of 1997. In 2001, President George W. Bush signed the Economic Growth and Tax Relief Reconciliation Act of 2001, into law as part of a $1.35 trillion tax cut program.

In 2003, the Jobs and Growth Tax Relief Reconciliation Act of 2003 reduced the rate on qualified dividends and long-term capital gains to 15%, and to 5% for individuals in the lowest two income tax brackets through 2008.

The 15% tax rate was extended through 2010 as a result of the Tax Increase Prevention and Reconciliation Act of 2005, and through 2012 in legislation signed on December 17, 2010. The American Taxpayer Relief Act of 2012 (signed on January 2, 2013) made qualified dividends a permanent part of the tax code but added a 20% rate on income in the new highest 39.6% tax bracket.

The Emergency Economic Stabilization Act of 2008 caused the IRS to introduce Form 8949, Sales and Other Dispositions of Capital Assets, and to introduce radical changes to Form 1099-B. These changes forced brokers to report not just the amounts of sales proceeds but purchases to the IRS, enabling the IRS to check reported capital gains.

Section 2011 of the Small Business Jobs Act of 2010 exempted 100% of the taxes on capital gains for angel and venture capital investors on small business stock investments if held for 5 years. It was a temporary measure but was extended further through 2011 by the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 as a jobs stimulus.

In 2013, provisions of the Patient Protection and Affordable Care Act ("Obama-care") took effect that imposed the Medicare tax of 3.8% (formerly a payroll tax) on capital gains of high-income taxpayers.

Summary of recent history

The following table summarizes the changes to the long-term capital gains tax rates made since 1998. (Short-term capital gains have been taxed at the same rate as ordinary income for this entire period.)

* The 2001 rates are listed first, the 2002 – May 2003 rates second.

** The 8% and 18% rates were for capital gains from certain assets held for more than five years.

*** The gain may also be subject to the 3.8% Medicare tax.

Incidence

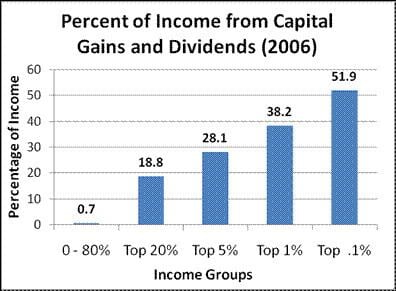

Capital gains taxes are disproportionately paid by high-income households, since they are more likely to own assets that generate the taxable gains. While this supports the argument that payers of capital gains taxes have more "ability to pay," it also means that the payers are especially able to defer or avoid the tax, as it only comes due if and when the owner sells the asset. The disproportionate incidence on high-income households means that most debate on tax rates is partisan. The Republican Party favors lower rates, whereas the Democratic Party favors higher rates.

Even though the incidence of the tax is on high-income taxpayers, low-income taxpayers who do not file capital gains taxes may wind up paying them through changed prices as the actual payers pass through the cost of paying the tax. Another factor complicating the use of capital gains taxes to address income inequality is that capital gains are usually not recurring income. A taxpayer may be "high-income" in the single year in which he or she sells an asset or invention.

Existence of the tax

The existence of the capital gains tax is controversial on partisan grounds. In 1995, to support the Contract with America legislative program of House Speaker Newt Gingrich, Stephen Moore and John Silvia wrote a study for the Cato Institute. In the study, they proposed halving of capital gains taxes, arguing that this move would "substantially raise tax collections and increase tax payments by the rich" and that it would increase economic growth and job creation. They wrote that the tax "is so economically inefficient...that the optimal economic policy...would be to abolish the tax entirely." More recently, Moore has written that the capital gains tax constitutes double taxation. "First, most capital gains come from the sale of financial assets like stock. But publicly held companies have to pay corporate income tax....Capital gains is a second tax on that income when the stock is sold."

Preferential rate

The fact that the long-term capital gains rate is lower than the rate on ordinary income is regarded by the political left, such as Sen. Bernie Sanders, as a "tax break" that excuses investors from paying their "fair share." The tax benefit for a long-term capital gain is sometimes referred to as a "tax expenditure" that government could elect to stop spending. By contrast, Republicans favor lowering the capital gain tax rate as an inducement to saving and investment. Also, the lower rate partly compensates for the fact that some capital gains are illusory and reflect nothing but inflation between the time the asset is bought and the time it is sold. Moore writes, "when inflation is high....the tax rate can even rise above 100 percent", as when a taxpayer owes tax on a capital gain that does not result in any increase in real wealth.

Holding period

The one-year threshold between short-term and long-term capital gains is arbitrary and has changed over time. Short-term gains are disparaged as speculation and are perceived as self-interested, myopic, and destabilizing, while long-term gains are characterized as investment, which supposedly reflects a more stable commitment that is in the nation's interest. Others call this a false dichotomy. The holding period to qualify for favorable tax treatment has varied from six months to ten years (see History above). There was special treatment of assets held for five years during the Presidency of George W. Bush. In her 2016 Presidential campaign, Hillary Clinton advocated holding periods of up to six years with a sliding scale of tax rates.

Carried interest

Carried interest is the share of any profits that the general partners of private equity funds receive as compensation, despite not contributing any initial funds. The manager may also receive compensation that is a percentage of the assets under management. Tax law provides that when such managers take, as a fee, a portion of the gain realized in connection with the investments they manage, the manager's gain is afforded the same tax treatment as the client's gain. Thus, where the client realizes long-term capital gains, the manager's gain is a long-term capital gain -- generally resulting in a lower tax rate for the manager than would be the case if the manager's income were not treated as a long-term capital gain. Under this treatment, the tax on a long-term gain does not depend on how investors and managers divide the gain.

This tax treatment is often called the "hedge-fund loophole", even though it is private equity funds that benefit from the treatment; hedge funds usually do not have long-term gains. It has been criticized as "indefensible" and a "gross unfairness", because it taxes management services at a preferential rate intended for long-term gains. Warren Buffett has used the term "coddling the super rich". One counterargument is that the preferential rate is warranted because a grant of carried interest is often deferred and contingent, making it less reliable than a regular salary.

Effects

The capital gains tax raises money for government but penalizes investment (by reducing the final rate of return). Proposals to change the tax rate from the current rate are accompanied by predictions on how it will affect both results. For example, an increase of the tax rate would be more of a disincentive to invest in assets, but would seem to raise more money for government. However, the Laffer curve suggests that the revenue increase might not be linear and might even be a decrease, as Laffer's "economic effect" begins to outweigh the "arithmetic effect." For example, a 10% rate increase (such as from 20% to 22%) might raise less than 10% additional tax revenue by inhibiting some transactions. Laffer postulated that a 100% tax rate results in no tax revenue.

Another economic effect that might make receipts differ from those predicted is that the United States competes for capital with other countries. A change in the capital gains rate could attract more foreign investment, or drive United States investors to invest abroad.

Congress sometimes directs the Congressional Budget Office (CBO) to estimate the effects of a bill to change the tax code. It is contentious on partisan grounds whether to direct the CBO to use dynamic scoring (to include economic effects), or static scoring that does not consider the bill's effect on the incentives of taxpayers. Republicans mandated dynamic scoring in the Budget and Accounting Transparency Act of 2014. The Act was passed by the House on a party-line vote but did not become law.

Measuring the effect on the economy

Supporters of cuts in capital gains tax rates may argue that the current rate is on the falling side of the Laffer curve (past a point of diminishing returns) — that it is so high that its disincentive effect is dominant, and thus that a rate cut would "pay for itself." However, correlation between top tax rate and total economic growth is inconclusive.

Mark LaRochelle wrote on the conservative website Human Events that cutting the capital gains rate increases employment. He presented a U.S. Treasury chart to assert that "in general, capital gains taxes and GDP have an inverse relationship: when the rate goes up, the economy goes down". He also cited statistical correlation based on tax rate changes during the presidencies of George W. Bush, Bill Clinton, and Ronald Reagan.

However, comparing capital gains tax rates and economic growth in America from 1950 to 2011, Brookings Institution economist Leonard Burman found "no statistically significant correlation between the two", even after using "lag times of five years." Burman's data are shown in the chart at right.

Economist Thomas L. Hungerford of the liberal Economic Policy Institute found "little or even a negative" correlation between capital gains tax reduction and rates of saving and investment, writing: "Saving rates have fallen over the past 30 years while the capital gains tax rate has fallen from 28% in 1987 to 15% today .... This suggests that changing capital gains tax rates have had little effect on private saving". Hungerford also studied top marginal tax rates from 1945 to 2010 and likewise found no correlation with saving, investment and productivity growth.

Factors that complicate measurement

Researchers usually use the top marginal tax rate to characterize policy as high-tax or low-tax. This figure measures the disincentive on the largest transactions per additional dollar of taxable income. However, this might not tell the complete story. The table Summary of recent history above shows that, although the marginal rate is higher now than at any time since 1998, there is also a substantial bracket on which the tax rate is 0%.

Another reason it is hard to prove correlation between the top capital gains rate and total economic output is that changes to the capital gains rate do not occur in isolation, but as part of a tax reform package. They may be accompanied by other measures to boost investment, and Congressional consensus to do so may derive from an economic shock, from which the economy may have been recovering independent of tax reform. A reform package may include increases and decreases in tax rates; the Tax Reform Act of 1986 increased the top capital gains rate, from 20% to 28%, as a compromise for reducing the top rate on ordinary income from 50% to 28%.

Strategic losses

The ability to use capital losses to offset capital gains in the same year is discussed above. Toward the end of a tax year, some investors sell assets that are worth less than the investor paid for them to obtain this tax benefit.

A wash sale, in which the investor sells an asset and buys it (or a similar asset) right back, cannot be treated as a loss at all, although there are other potential tax benefits as consolation.

In January, a new tax year begins; if stock prices increase, analysts may attribute the increase to an absence of such end-of-year selling and say there is a January effect. A Santa Claus rally is an increase in stock prices at the end of the year, perhaps in anticipation of a January effect.

Versus purchase

A taxpayer can designate that a sale of corporate stock corresponds to a specified purchase. For example, the taxpayer holding 500 shares may have bought 100 shares each on five occasions, probably at a different price each time. The individual lots of 100 shares are typically not held separate; even in the days of physical stock certificates, there was no indication which stock was bought when. If the taxpayer sells 100 shares, then by designating which of the five lots is being sold, the taxpayer will realize one of five different capital gains or losses. The taxpayer can maximize or minimize the gain depending on an overall strategy, such as generating losses to offset gains, or keeping the total in the range that is taxed at a lower rate or not at all.

To use this strategy, the taxpayer must specify at the time of a sale which lot is being sold (creating a "contemporaneous record"). This "versus purchase" sale is versus (against) a specified purchase. On brokerage websites, a "Lot Selector" may let the taxpayer specify the purchase to which a sell order corresponds.

Primary residence

The law lets an individual exclude from gross income up to $250,000 ($500,000 for a married couple filing jointly) of capital gains on the sale of real property if the owner used it as primary residence for two of the five years before the date of sale. The two years of residency do not have to be continuous. An individual may meet the ownership and use tests during different 2-year periods. A taxpayer can move and claim the primary-residence exclusion every two years if living in an area where home prices are rising rapidly.

The tests may be waived for military service, disability, partial residence, unforeseen events, and other reasons. Moving to shorten one's commute to a new job is not an unforeseen event. Bankruptcy of an employer that induces a move to a different city is likely an unforeseen event, but the exclusion will be pro-rated if one has stayed in the home less than two years.

The amount of this exclusion is not increased for home ownership beyond five years. One is not able to deduct a loss on the sale of one's home.

Deferral strategies

Taxpayers can defer capital gains taxes to a future tax year using the following strategies:

Although 1031 treatment is not available for personal real estate, the taxpayer can reside in the property. For example, a homeowner could move out of the primary residence, rent it out temporarily, exchange it for a new house, rent that house out temporarily, and then move into it.

Simpson-Bowles

In 2011, President Barack Obama signed Executive Order 13531 establishing the National Commission on Fiscal Responsibility and Reform (the "Simpson-Bowles Commission") to identify "policies to improve the fiscal situation in the medium term and to achieve fiscal sustainability over the long run". The overview in the Commission's final report described its recommendations on taxes as to "Sharply reduce rates, broaden the base, simplify the tax code, and reduce the deficit by reducing the many 'tax expenditures'—another name for spending through the tax code. Reform corporate taxes to make America more competitive, and cap revenue to avoid excessive taxation." It proposed to eliminate the preferential tax rate for long-term capital gains.

Supporters described it as a "compromise" though "Anyone ... will no doubt find elements that they disagree with." Regarding taxes, it used the same approach as the 1986 reform: higher rates for long-term capital gains versus a lower top rate on ordinary income.

The Commission's tax proposals were not enacted. Republicans, who did not control the Senate, wanted Obama to rally his fellow Democrats on fiscal policy; 2012 presidential candidate Mitt Romney faulted Obama for "missing the bus" on his own Commission. Obama countered that his own tax plan "made some adjustments to" Simpson-Bowles and was "before the Congress," but Politifact called both assertions "half true", as "we don’t expect the GOP-led Congress to pursue it."

In the 2016 campaign

Tax policy was a part of the 2016 presidential campaign, as candidates proposed changes to the tax code that affect the capital gains tax.

President Donald Trump's main proposed change to the capital gains tax was to repeal the 3.8% Medicare surtax that took effect in 2013. He also proposed to repeal the Alternative Minimum Tax, which would reduce tax liability for taxpayers with large incomes including capital gains. His maximum tax rate of 15% on businesses could result in lower capital gains taxes. However, as well as lowering tax rates on ordinary income, he would lower the dollar amounts for the remaining tax brackets, which would subject more individual capital gains to the top (20%) tax rate. Other Republican candidates proposed to lower the capital gains tax (Ted Cruz proposed a 10% rate), or eliminate it entirely (such as Marco Rubio).

Democratic nominee Hillary Clinton proposed to increase the capital gains tax rate for high-income taxpayers by "creating several new, higher ordinary rates", and proposed a sliding scale for long-term capital gains, based on the time the asset was owned, up to 6 years. Gains on assets held from one to two years would be reclassified short-term and taxed as ordinary income, at an effective rate of up to 43.4%, and long-term assets not held for a full 6 years would also be taxed at a higher rate. Clinton also proposed to treat carried interest (see above) as ordinary income, increasing the tax on it, to impose a tax on "high-frequency" trading, and to take other steps. Bernie Sanders proposed to treat many capital gains as ordinary income, and increase the Medicare surtax to 6%, resulting in a top effective rate of 60% on some capital gains.