| ||

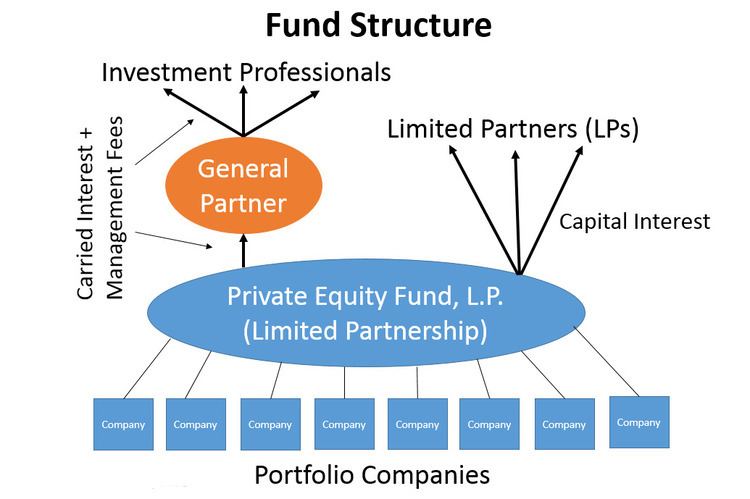

Carried interest or carry, in finance is a share of the profits of an investment paid to the investment manager in excess of the amount that the manager contributes to the partnership, specifically in alternative investments i.e., private equity and hedge funds. It is a performance fee rewarding the manager for enhancing performance.

Contents

The manager's carried-interest allocation varies depending on the type of investment fund and the demand for the fund from investors. In private equity, the standard carried-interest allocation historically has been 20% for funds making buyout and venture investments. Notable examples of private equity firms with carried interest of 25% to 30% include Bain Capital and Providence Equity Partners. In private equity, the distribution of carried interest is directed by a distribution waterfall: in order to receive carried interest, the manager must first return all capital contributed by the investors, and, in certain cases, a previously agreed-upon rate of return (the "hurdle rate" or "preferred return") to investors. Private equity funds distribute carried interest to the manager only upon a successful exit from an investment, which may take years. The customary hurdle rate in private equity is 7–8% per annum.

In a hedge fund environment, carried interest is usually referred to as a "performance fee" and because they invest in liquid investments, are often able to pay carried interest annually if the fund has generated a profit. They have historically centered on 20%, but have had greater variability than those of private equity funds. In extreme cases performance fees reach as high as 44% of a fund's profits, although usually it is between 15% and 20%.

Definition and history

Carried interest is a share of the profits of an investment paid to the investment manager in excess of the amount that the manager contributes to the partnership, specifically in alternative investments i.e., private equity and hedge funds. It is a performance fee rewarding the manager for enhancing performance.

The origin of carried interest can be traced to the 16th century, when European ships were crossing to Asia and the Americas. The captain of the ship would take a 20% share of the profit from the carried goods, to pay for the transport and the risk of sailing over oceans.

Difference from a "management fee"

Historically, carried interest has served as the primary source of income for manager and firm in both private equity and hedge funds. Both private equity and hedge funds tended to have a small annual management fee of 1% to 2% of committed capital per year; the management fee is to cover the costs of investing and managing the fund rather than for wealth creation for the manager. As the sizes of both private equity and hedge funds have increased, management fees have become a more meaningful portion of the value proposition for fund managers as evidenced by the 2007 initial public offering of the Blackstone Group.

Taxation

The taxation of carried interest has been an issue since the mid-2000s, particularly as the compensation earned by certain investors increased along with the sizes of private equity and hedge funds. Historically, carried interest has been treated as a capital gain for tax purposes in most jurisdictions. The reason for this treatment is that a fund manager would make a substantial commitment of his own capital into the fund and carried interest would represent a portion of the manager's return on that investment. While hedge funds typically trade their investments actively, private equity firms tend to hold their investments for many years. Thus, capital gains from private equity funds typically qualify as long-term capital gains, which receive favorable tax treatment in many jurisdictions. Critics of this tax treatment seek to disaggregate the returns directly related to the capital contributed by the fund manager from the carried interest allocated from the other investors in the fund to the fund manager.

United States

Because the manager is compensated with carried interest, the bulk of his income from the fund is taxed as a return on investment and not as compensation for services. This tax treatment originated in the oil and gas industry of the early 20th century, when the actual oil exploration companies which used financial partners' investments, had their profits taxed at the capital gains rate. This has been lower than the rate for ordinary income for much of the 20th century, in order to encourage risk and entrepreneurship. The logic was that the financial partners’ sweat equity had entailed the risk of loss, if their exploration did not pan out.

Typically, a partner is not taxed upon receipt of a carried interest because it is difficult to measure the present value of an interest in future profits. In 1993, the Internal Revenue Service adopted this approach as a general administrative rule, and again in regulations proposed in 2005. Instead, the partner is taxed as the partnership earns income. In the case of a hedge fund, this means that the partner defers taxation on the income the hedge fund earns, which is typically ordinary income or possibly short-term capital gains, which are taxed the same as ordinary income due to the nature of the investments most hedge funds make. Private equity funds, however, typically invest on a longer horizon, with the result that their income is long-term capital gain, taxable to individuals at a maximum 20% rate. Because this compensation can reach enormous figures in the case of the most successful funds, concern has been raised in both the U.S. Congress and the media, that managers are taking advantage of tax loopholes to receive what is effectively a salary without paying the ordinary 39.6% marginal income tax rates a high-income person would have to pay on such income. As of September 2016 the loophole’s total tax benefit for private-equity partners is estimated to be about $2 billion per year up to 14 or 16 billion dollars.

To address this concern, U.S. Representative Sander M. Levin introduced H

In 2009, the Obama Administration included a line item on taxing carried interest at ordinary income rates in the 2009 Budget Blueprint. On April 2, 2009, Congressman Levin introduced a revised version of the carried interest legislation as H

Favorable taxation for carried interest became an issue during the 2012 Republican primary race for president, because 31% of presidential candidate Mitt Romney's 2010 and 2011 income was carried interest. On May 28, 2010, the House approved carried interest legislation as part of amendments to the Senate-passed version of H

On February 26, 2014, House Committee on Ways and Means chairman Dave Camp (R-MI) released draft legislation to raise the tax on carried interest from the current 23.8 percent to 35 percent. In June 2015, Sander Levin (D-MI) introduced the Carried Interest Fairness Act of 2015 (H.R. 2889) to tax investment advisers with ordinary income tax rates.

As of 2015 some in the private equity and hedge fund industries had been lobbying against changes, being among the biggest political donors on both sides of the aisle. whereas during the presidential race Wall Street supported only Hillary Clinton.

In June 2016 Hillary Clinton said that "if Congress does not act, as president she'll ask the Treasury Department to use its regulatory authority to end a tax advantage".

United Kingdom

The Finance Act 1972 provided that gains on investments acquired by reason of rights or opportunities offered to individuals as directors or employees were, subject to various exceptions, taxed as income and not capital gains. This may strictly have applied to the carried interests of many venture-capital executives, even if they were partners and not employees of the investing fund, because they were often directors of the investee companies. In 1987, the Inland Revenue and the British Venture Capital Association (BVCA) entered into an agreement which provided that in most circumstances gains on carried interest were not taxed as income.

The Finance Act 2003 widened the circumstances in which investment gains were treated as employment-related and therefore taxed as income. In 2003 the Inland Revenue and the BVCA entered into a new agreement which had the effect that, notwithstanding the new legislation, most carried-interest gains continued to be taxed as capital gains and not as income. Such capital gains were generally taxed at 10% as opposed to a 40% rate on income.

In 2007, the favorable tax rates on carried interest attracted political controversy. It was said that cleaners paid taxes at a higher rate than the private-equity executives whose offices they cleaned. The outcome was that the capital-gains tax rules were reformed, increasing the rate on gains to 18%, but carried interest continued to be taxed as gains and not as income.