| ||

Support x ∈ [ μ , ∞ ) {\displaystyle x\in [\mu ,\infty )} PDF c 2 π e − c 2 ( x − μ ) ( x − μ ) 3 / 2 {\displaystyle {\sqrt {\frac {c}{2\pi }}}~~{\frac {e^{-{\frac {c}{2(x-\mu )}}}}{(x-\mu )^{3/2}}}} CDF erfc ( c 2 ( x − μ ) ) {\displaystyle {\textrm {erfc}}\left({\sqrt {\frac {c}{2(x-\mu )}}}\right)} Mean ∞ {\displaystyle \infty } Median c / 2 ( erfc − 1 ( 1 / 2 ) ) 2 {\displaystyle c/2({\textrm {erfc}}^{-1}(1/2))^{2}\,} , for μ = 0 {\displaystyle \mu =0} | ||

In probability theory and statistics, the Lévy distribution, named after Paul Lévy, is a continuous probability distribution for a non-negative random variable. In spectroscopy, this distribution, with frequency as the dependent variable, is known as a van der Waals profile. It is a special case of the inverse-gamma distribution.

Contents

It is one of the few distributions that are stable and that have probability density functions that can be expressed analytically, the others being the normal distribution and the Cauchy distribution.

Definition

The probability density function of the Lévy distribution over the domain

where

where

where y is defined as

The characteristic function of the Lévy distribution is given by

Note that the characteristic function can also be written in the same form used for the stable distribution with

Assuming

which diverges for all n > 0 so that the moments of the Lévy distribution do not exist. The moment generating function is then formally defined by:

which diverges for

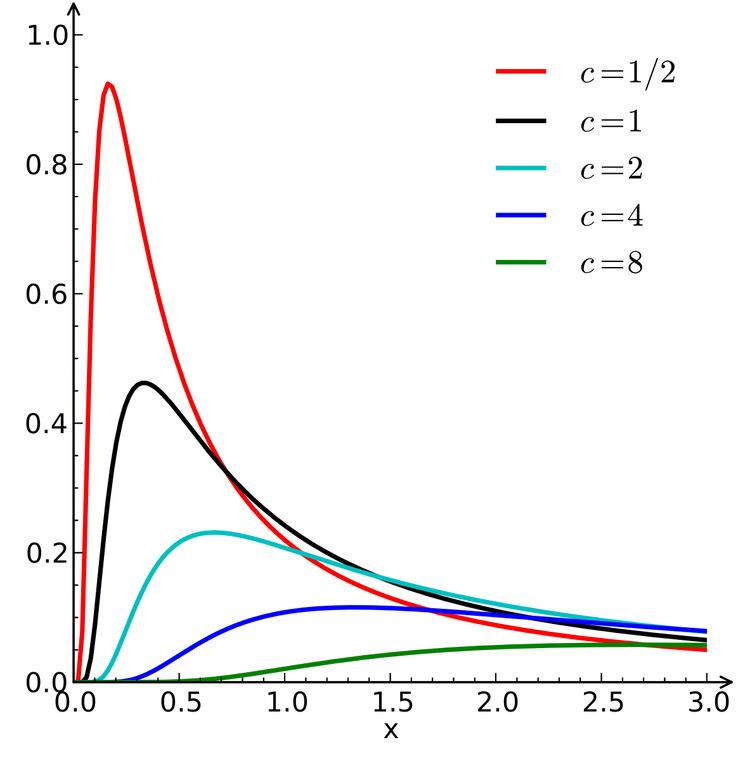

This is illustrated in the diagram below, in which the probability density functions for various values of c and

Differential equation

Properties

The standard Lévy distribution satisfies the condition

where

Related distributions

Random sample generation

Random samples from the Lévy distribution can be generated using inverse transform sampling. Given a random variate U drawn from the uniform distribution on the unit interval (0, 1], the variate X given by

is Lévy-distributed with location