| ||

In mathematical finance, the Cox–Ingersoll–Ross model (or CIR model) describes the evolution of interest rates. It is a type of "one factor model" (short rate model) as it describes interest rate movements as driven by only one source of market risk. The model can be used in the valuation of interest rate derivatives. It was introduced in 1985 by John C. Cox, Jonathan E. Ingersoll and Stephen A. Ross as an extension of the Vasicek model.

Contents

The model

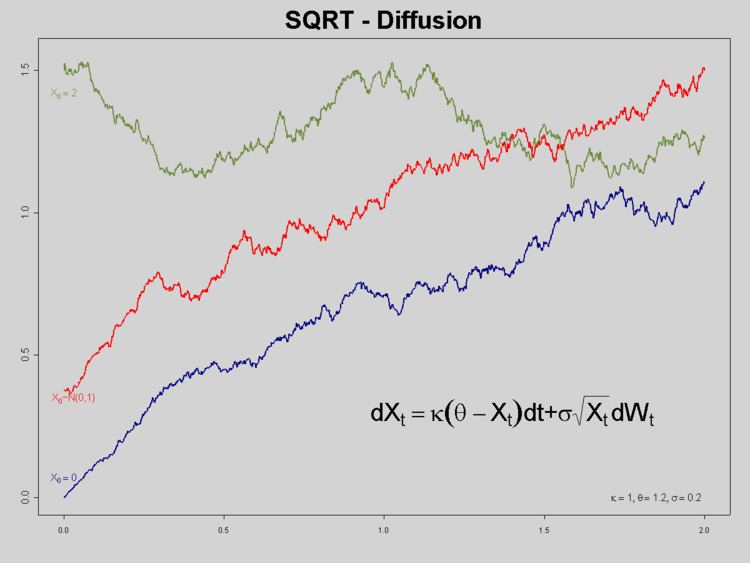

The CIR model specifies that the instantaneous interest rate follows the stochastic differential equation, also named the CIR Process:

where

The standard deviation factor,

is met. More generally, when the rate (

This process can be defined as a sum of squared Ornstein–Uhlenbeck process. The CIR is an ergodic process, and possesses a stationary distribution. The same process is used in the Heston model to model stochastic volatility.

Distribution

The distribution of future values of a CIR process can be computed in closed form:

where

where

Due to mean reversion, as time becomes large, the distribution of

where

Properties

Calibration

The continuous SDE can be discretized as follows

which is equivalent to

Simulation

Stochastic simulation of the CIR process can be achieved using two variants:

Bond pricing

Under the no-arbitrage assumption, a bond may be priced using this interest rate process. The bond price is exponential affine in the interest rate:

where

Extensions

Time varying functions replacing coefficients can be introduced in the model in order to make it consistent with a pre-assigned term structure of interest rates and possibly volatilities. The most general approach is in Maghsoodi (1996). A more tractable approach is in Brigo and Mercurio (2001b) where an external time-dependent shift is added to the model for consistency with an input term structure of rates. A significant extension of the CIR model to the case of stochastic mean and stochastic volatility is given by Lin Chen (1996) and is known as Chen model. A CIR process is a special case of a basic affine jump diffusion, which still permits a closed-form expression for bond prices.