PDF (see article) | ||

| ||

Parameters m {\displaystyle m} location ( 0 ≤ m < 2 π ) {\displaystyle (0\leq m<2\pi )} λ > 0 {\displaystyle \lambda >0} scale (real) κ > 0 {\displaystyle \kappa >0} asymmetry (real) Support 0 ≤ θ < 2 π {\displaystyle 0\leq \theta <2\pi } Mean m {\displaystyle m} (circular) Variance 1 − λ 2 ( 1 κ 2 + λ 2 ) ( κ 2 + λ 2 ) {\displaystyle 1-{\frac {\lambda ^{2}}{\sqrt {\left({\frac {1}{\kappa ^{2}}}+\lambda ^{2}\right)\left(\kappa ^{2}+\lambda ^{2}\right)}}}} (circular) CF λ 2 e i m n ( n − i λ / κ ) ( n + i λ κ ) {\displaystyle {\frac {\lambda ^{2}e^{imn}}{\left(n-i\lambda /\kappa \right)\left(n+i\lambda \kappa \right)}}} | ||

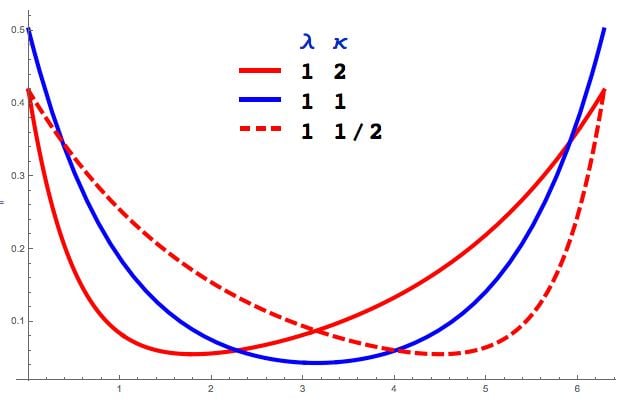

In probability theory and directional statistics, a wrapped asymmetric Laplace distribution is a wrapped probability distribution that results from the "wrapping" of the asymmetric Laplace distribution around the unit circle. For the symmetric case (asymmetry parameter κ = 1), the distribution becomes a wrapped Laplace distribution. The distribution of the ratio of two circular variates (Z) from two different wrapped exponential distributions will have a wrapped asymmetric Laplace distribution. These distributions find application in stochastic modelling of financial data.

Contents

Definition

The probability density function of the wrapped asymmetric Laplace distribution is:

where

Characteristic function

The characteristic function of the wrapped asymmetric Laplace is just the characteristic function of the asymmetric Laplace function evaluated at integer arguments:

which yields an alternate expression for the wrapped asymmetric Laplace PDF in terms of the circular variable z=ei(θ-m) valid for all real θ and m:

where

Circular moments

In terms of the circular variable

The first moment is then the average value of z, also known as the mean resultant, or mean resultant vector:

The mean angle is

and the length of the mean resultant is

The circular variance is then 1 − R

Generation of random variates

If X is a random variate drawn from an asymmetric Laplace distribution (ALD), then

Since the ALD is the distribution of the difference of two variates drawn from the exponential distribution, it follows that if Z1 is drawn from a wrapped exponential distribution with mean m1 and rate λ/κ and Z2 is drawn from a wrapped exponential distribution with mean m2 and rate λκ, then Z1/Z2 will be a circular variate drawn from the wrapped ALD with parameters ( m1 - m2 , λ, κ) and