| ||

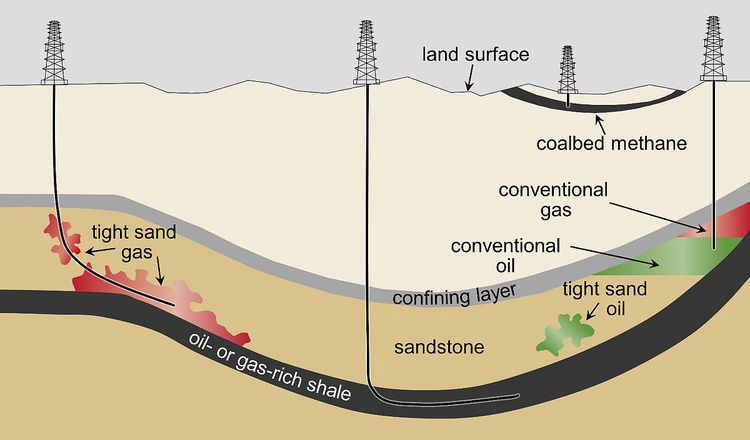

Tight oil (also known as shale oil or light tight oil, abbreviated LTO) is petroleum that consists of light crude oil contained in petroleum-bearing formations of low permeability, often shale or tight sandstone. Economic production from tight oil formations requires the same hydraulic fracturing and often uses the same horizontal well technology used in the production of shale gas. While sometimes called "shale oil", tight oil should not be confused with oil shale, which is shale rich in kerogen, or shale oil, which is oil produced from oil shales. Therefore, the International Energy Agency recommends to use the term "light tight oil" for oil produced from shales or other very low permeability formations, while World Energy Resources 2013 report by the World Energy Council uses the term "tight oil".

Contents

In May 2013 the International Energy Agency in its Medium-Term Oil Market Report (MTOMR) said that the North American oil production surge led by unconventional oils - US light tight oil (LTO) and Canadian oil sands - had produced a global supply shock that would reshape the way oil is transported, stored, refined and marketed.

Inventory and examples

Tight oil formations include the Bakken Shale, the Niobrara Formation, Barnett Shale, and the Eagle Ford Shale in the United States, R'Mah Formation in Syria, Sargelu Formation in the northern Persian Gulf region, Athel Formation in Oman, Bazhenov Formation and Achimov Formation of West Siberia in Russia, Arckaringa Basin in Australia, Chicontepec Formation in Mexico, and the Vaca Muerta oil field in Argentina. In June 2013 the U.S. Energy Information Administration published a global inventory of estimated recoverable tight oil and tight gas resources in shale formations, "Technically Recoverable Shale Oil and Shale Gas Resources: An Assessment of 137 Shale Formations in 41 Countries Outside the United States." The inventory is incomplete due to exclusion of tight oil and gas from sources other than shale such as sandstone or carbonates, formations underlying the large oil fields located in the Middle East and the Caspian region, off shore formations, or about which there is little information. Amounts include only high quality prospects which are likely to be developed.

In 2012, at least 4,000 new producing shale oil (tight oil) wells were brought online in the United States. By comparison, the number of new producing oil and gas wells (both conventional and unconventional) completed in 2012 globally outside the United States and Canada is less than 4,000.

Characteristics

Tight oil shale formations are heterogeneous and vary widely over relatively short distances. Thus, even in a single horizontal drill hole, the amount recovered may vary, as may recovery within a field or even between adjacent wells. This makes evaluation of plays and decisions regarding the profitability of wells on a particular lease difficult. Production of oil from tight formations requires at least 15 to 20 percent natural gas in the reservoir pore space to drive the oil toward the borehole; tight reservoirs which contain only oil cannot be economically produced. Formations which formed under marine conditions contain less clay and are more brittle, and thus more suitable for fracking than formations formed in fresh water which may contain more clay. Formations with more quartz and carbonate are more brittle.

The natural gas and other volatiles in LTO make it more hazardous to handle, store, and transport. This was an aggravating factor in the series of fatal explosions after the Lac-Mégantic derailment.

Exploitation

Prerequisites for exploitation include being able to obtain rights to drill, easier in the United States and Canada where private owners of subsurface rights are motivated to enter into leases; the availability of expertise and financing, easier in the United States and Canada where there are many independent operators and supporting contractors with critical expertise and suitable drilling rigs; infrastructure to gather and transport oil; and water resources for use in hydraulic fracturing.

Analysts expect that $150 billion will be spent on further developing North American tight oil fields in 2015. The large increase in tight oil production is one of the reasons behind the price drop in late 2014.

Outside the United States and Canada, development of shale oil (tight oil) resources may be limited by the lack of available drilling rigs: 2/3 of the world's active drill rigs are in the US and Canada, and rigs elsewhere are less likely to be equipped for horizontal drilling. Drilling intensity may be another constraint, as tight-oil development requires far more completed wells than does conventional oil. Leonardo Maugeri considers this will be "an insurmountable environmental hurdle in Europe".