| ||

The Stability and Growth Pact (SGP) is an agreement, among the 28 Member states of the European Union, to facilitate and maintain the stability of the Economic and Monetary Union (EMU). Based primarily on Articles 121 and 126 of the Treaty on the Functioning of the European Union, it consists of fiscal monitoring of members by the European Commission and the Council of Ministers, and the issuing of a yearly recommendation for policy actions to ensure a full compliance with the SGP also in the medium-term. If a Member State breaches the SGP's outlined maximum limit for government deficit and debt, the surveillance and request for corrective action will intensify through the declaration of an Excessive Deficit Procedure (EDP); and if these corrective actions continue to remain absent after multiple warnings, the Member State can ultimately be issued economic sanctions. The pact was outlined by a resolution and two council regulations in July 1997. The first regulation "on the strengthening of the surveillance of budgetary positions and the surveillance and coordination of economic policies", known as the "preventive arm", entered into force 1 July 1998. The second regulation "on speeding up and clarifying the implementation of the excessive deficit procedure", known as the "dissuasive arm", entered into force 1 January 1999.

Contents

- Criticism

- Reform 2005

- Reform 2011 and hints to the new European economic governance

- Member states by SGP criteria

- 1999 2005

- After the 2005 reform

- References

The purpose of the pact was to ensure that fiscal discipline would be maintained and enforced in the EMU. All EU member states are automatically members of both the EMU and the SGP, as this is defined by paragraphs in the EU Treaty itself. The fiscal discipline is ensured by the SGP by requiring each Member State, to implement a fiscal policy aiming for the country to stay within the limits on government deficit (3% of GDP) and debt (60% of GDP); and in case of having a debt level above 60% it should each year decline with a satisfactory pace towards a level below. As outlined by the "preventive arm" regulation, all EU member states are each year obliged to submit a SGP compliance report for the scrutiny and evaluation of the European Commission and the Council of Ministers, that will present the country's expected fiscal development for the current and subsequent three years. These reports are called "stability programmes" for eurozone Member States and "convergence programmes" for non-eurozone Member States, but despite having different titles they are identical in regards of the content. After the reform of the SGP in 2005, these programmes have also included the Medium-Term budgetary Objectives (MTO's), being individually calculated for each Member State as the medium-term sustainable average-limit for the country's structural deficit, and the Member State is also obliged to outline the measures it intends to implement to attain its MTO. If the EU Member State does not comply with both the deficit limit and the debt limit, a so-called "Excessive Deficit Procedure" (EDP) is initiated along with a deadline to comply, which basically includes and outlines an "adjustment path towards reaching the MTO". This procedure is outlined by the "dissuasive arm" regulation.

The SGP was initially proposed by German finance minister Theo Waigel in the mid-1990s. Germany had long maintained a low-inflation policy, which had been an important part of the German economy's strong performance since the 1950s. The German government hoped to ensure the continuation of that policy through the SGP, which would ensure the prevalence of fiscal responsibility, and limit the ability of governments to exert inflationary pressures on the European economy. As such, it was also described to be a key tool for the Member States adopting the euro, to ensure that they did not only meet the Maastricht convergence criteria at the time of adopting the euro, but kept on to comply with the fiscal criteria for the following years.

Criticism

The Pact has been criticised by some as being insufficiently flexible and needing to be applied over the economic cycle rather than in any one year. They fear that by limiting governments' abilities to spend during economic slumps it may hamper growth. In contrast, other critics think that the Pact is too flexible; economist Antonio Martino writes: "The fiscal constraints introduced with the new currency must be criticized not because they are undesirable—in my view they are a necessary component of a liberal order—but because they are ineffective. This is amply evidenced by the “creative accounting” gimmickry used by many countries to achieve the required deficit to GDP ratio of 3 percent, and by the immediate abandonment of fiscal prudence by some countries as soon as they were included in the euro club. Also, the Stability Pact has been watered down at the request of Germany and France."

Some remark that it has been applied inconsistently: the Council of Ministers failed to apply sanctions against France and Germany, while punitive proceedings were started (but fines never applied) when dealing with Portugal (2002) and Greece (2005). In 2002 the European Commission President (1999–2004) Romano Prodi described it as "stupid", but was still required by the Treaty to seek to apply its provisions.

The Pact has proved to be unenforceable against big countries such as France and Germany, which were its strongest promoters when it was created. These countries have run "excessive" deficits under the Pact definition for some years. The reasons that larger countries have not been punished include their influence and large number of votes on the Council of Ministers, which must approve sanctions; their greater resistance to "naming and shaming" tactics, since their electorates tend to be less concerned by their perceptions in the European Union; their weaker commitment to the euro compared to smaller states; and the greater role of government spending in their larger and more enclosed economies. The Pact was further weakened in 2005 to waive France's and Germany's violations.

Reform 2005

In March 2005, the EU Council, under the pressure of France and Germany, relaxed the rules; the EC said it was to respond to criticisms of insufficient flexibility and to make the pact more enforceable.

The Ecofin agreed on a reform of the SGP. The ceilings of 3% for budget deficit and 60% for public debt were maintained, but the decision to declare a country in excessive deficit can now rely on certain parameters: the behaviour of the cyclically adjusted budget, the level of debt, the duration of the slow growth period and the possibility that the deficit is related to productivity-enhancing procedures.

The pact is part of a set of Council Regulations, decided upon the European Council Summit 22–23 March 2005.

Reform 2011 and hints to the new European economic governance

In March 2011, following the 2010 European sovereign debt crisis, the EU member states adopted a new reform under the Open Method of Coordination, aiming at straightening the rules e.g. by adopting an automatic procedure for imposing of penalties in case of breaches of either the deficit or the debt rules. The new "Euro Plus Pact" is designed as a more stringent successor to the Stability and Growth Pact, which has not been implemented consistently. The measures are controversial not only because of the closed way in which it was developed but also for the goals that it postulates.

The four broad strategic goals are:

An additional fifth issue is:

Overall - looking at the new European economic governance framework, it seems to be in front of a "mixture" of different acts adopted at various territorial levels and characterized by a different legal nature. In particular, three acts shall be ascribed to the international norms’ realm: (1) the European Financial Stability Facility (EFSF), created by the Euro area Member States following the decisions taken on 9 May 2010 within the framework of the ECOFIN Council. Particularly, the EFSF’s mandate is to safeguard financial stability in Europe by providing financial assistance to the Eurozone’s macro-economic adjustment programme ; (2) the Treaty establishing the European Stability Mechanism (ESM) was signed on 2 February 2012, after a decision taken by the European Council (December 2010). Designed as a permanent crisis resolution mechanism for the countries of the Euro area, the ESM issues debt instruments in order to finance loans and other forms of financial assistance to the involved Member States; finally, (3) the Treaty on Stability, Coordination and Governance (TSCG), whose final version was signed on 2 March 2012 by the leaders of all euro area members and eight other EU member states, and entered into force on 1 January 2013. The TSCG has been commonly labeled "Fiscal Compact ", originally intended to promote the launch of a new international economic cooperation enforced by those EU Member States which are also part of the so-called.

Strictly speaking, those mentioned are "legal" mechanisms which have been newly introduced, and therefore have to be distinguished from the measures instead representing an adaptation of pre-existing rules. The latter are "customary" EU secondary norms contributing to the formation of the legal structure underlying the new European economic governance:

- in the case of the so-called "Six-Pack", five regulations and one directive are at stake as of 13 December 2011, with a view to strengthening the Stability and Growth Pact (SGP) – that is a rule-based framework for the coordination of national fiscal policies in the European Union whose details would be mentioned below. - given the higher potential for spillover effects of budgetary policies in a common currency area, in November 2011 the Commission proposed two further regulations to strengthen euro area budgetary surveillance. This reform package, the so-called "Two-Pack ", entered into force on 30 May 2013 in all Euro area Member States. The new measures were meant to increase transparency on their budgetary decisions and stronger coordination within the 2014 budgetary cycle, as well as to recognize the special needs of Euro area Member States under severe financial pressure . - the "Euro Plus" pact, agreed in Spring 2011 by the 17 Member States of the Euro area (and joined by Bulgaria, Denmark, Latvia, Lithuania, Poland and Romania), is intended to reinforce the economic pillar of the monetary union and achieve a new quality of economic policy coordination, with the objective of improving competitiveness and thereby leading to a higher degree of convergence reinforcing social market economy

- the "European Semester" has been introduced by the ECOFIN deliberation dated 7 September 2010. It was specifically meant to better an ex ante coordination of economic and budget policies of member states – integrating the specifications on the implementation of the Stability and Growth Pact . The latteer governs fiscal discipline in the EU, with the purpose of ensuring fiscal discipline in the Union within Europe2020. Although the Pact applies to all EU members, it has stricter enforcement mechanisms for Euro area members:

-"the preventive arm" is part of the European Semester. In particular – every year in April, Euro area member states submit Stability Programmes, while member states outside the euro area submit Convergence Programmes. These documents outline the main elements of the member states’ budgetary plans and are assessed by the Commission. An important part of the assessment addresses compliance with the minimum annual benchmark figure set for each individual country’s structural budget balance . Based on its assessment on the Stability and Convergence Programmes, the Commission draws up country-specific recommendations on which the Council adopts opinions in July. These include recommendations for appropriate policy actions. Furthermore, the Council adopts recommendations on economic policies that apply to the euro area as a whole.

-the "corrective" part entails the Excessive Deficit Procedure (EDP). This procedure is triggered if a member state's budget deficit exceeds 3% of GDP. The European Commission (DG Eurostat) is responsible for providing the data used for the EDP. Council Regulation (EC) 479/2009 requires that "In the event of a doubt regarding the correct implementation of the ESA 95 [now to be understood as ESA 2010] accounting rules, the Member State concerned shall request clarification from the Commission (Eurostat). The Commission (Eurostat) shall promptly examine the issue and communicate its clarification to the Member State concerned and, when appropriate, to the CMFB. For cases which are either complex or of general interest in the view of the Commission or the Member State concerned, the Commission (Eurostat) shall take a decision after consultation of the CMFB." When the Council, on the basis of Eurostat data, decides that the deficit is excessive, it makes recommendations to the member state concerned and sets a deadline for bringing the deficit back below the reference value. The Council can grant extensions to this deadline if it is found that the country concerned has made good progress in implementing the initial recommendations but has not been able to fully correct its deficit because of an exceptional economic context. When it addresses decisions and recommendations to euro area member states, only euro area ministers have the right to vote.

Before the establishment of those measures, however, the coordination of economic and employment policies still went through the ECOFIN Council’s guidelines – which were established on a triennial basis.

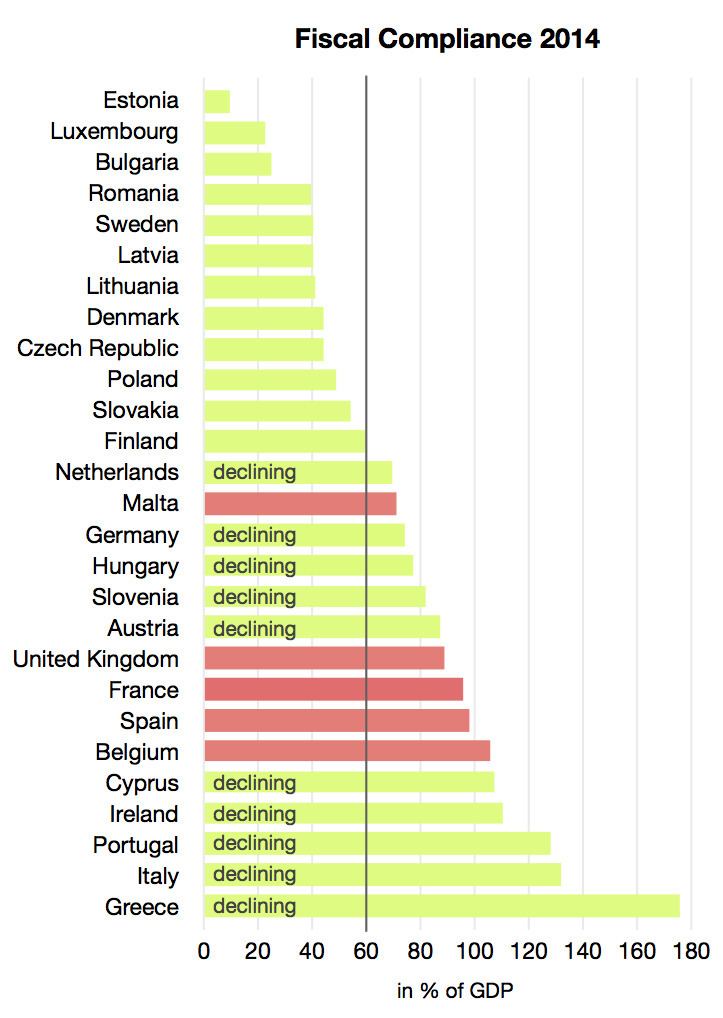

Member states by SGP criteria

The deficit and debt criterion is applied to both Eurozone and non-Eurozone EU member states. Data in the table are for the fiscal year 2011, being published as part of the European Commission's economic forecast in May 2012. And the past years with SGP breaches, were identified by the annexed table 53B and 55B from the report.

Notes

1999-2005

Across the first seven years, since the entry into force of the Stability and Growth Pact, all EU Member States were required to strive towards a common MTO being "to achieve a budgetary position of close to balance or in surplus over a complete business cycle - while providing a safety margin towards continuously respecting the government's 3% deficit limit". The first part of this MTO, was interpreted by the Commission Staff Service to mean continuously achievement each year throughout the business cycle of a "cyclically-adjusted budget balance net of one-off and temporary measures" (also referred to as the "structural balance") at minimum 0.0%. In 2000, the second part was interpreted and operationalized into a calculation formula for the MTO also to respect the so-called "Minimal Benchmark" (later referred to as "MTO Minimum Benchmark"). When assessing the annual Convergence/Stability programmes of the Member States, the Commission Staff Service checked whether the structural balance of the state complied with both the common "close to balance or surplus" criteria and the country-specific "Minimal Benchmark" criteria. The last round under this assessment scheme took place in Spring 2005, while all subsequent assessments were conducted according to a new reformed scheme - introducing the concept of a single country-specific MTO as the overall steering anchor for the fiscal policy.

After the 2005-reform

In order to ensure long-term compliance with the SGP deficit and debt criteria, the member states have since the SGP-reform in March 2005 striven towards achieving their country-specific Medium-Term budgetary Objective (MTO). The MTO is the set limit, that the structural balance relative to GDP needs to equal or be above for each year in the medium-term. Each state select its own MTO, but it needs to equal or be better than a calculated minimum requirement (Minimum MTO) ensuring sustainability of the government accounts throughout the long-term (calculated on basis of both future potential GDP growth, future cost of government debt, and future increases in age-related costs). The structural balance is calculated by the European Commission as the cyclically-adjusted balance minus "one-off measures" (i.e. one-off payments due to reforming a pension scheme). The cyclically-adjusted balance is calculated by adjusting the achieved general government balance (in % of GDP) compared to each years relative economic growth position in the business cycle (referred to as the "output gap"), which is found by subtraction of the achieved GDP growth with the potential GDP growth. So if a year is recorded with average GDP growth in the business cycle (equal to the potential GDP growth rate), the output gap will then be zero, meaning that the "cyclically-adjusted balance" then will be equal to the "government budget balance". In this way, because it is resistant to GDP growth changes, the structural balance is considered to be neutral and comparable across an entire business cycle (including both recession years and "overheated years"), making it perfect to be used consistently as a medium-term budgetary objective.

Whenever a country does not reach its MTO, it is required in the subsequent year(s) to implement annual improvements for its structural balance equal to minimum 0.5% of GDP, although it should be noted that several sub-rules (including the "expenditure benchmark") has the potential slightly to alter this requirement. When Member States are in this process of improving their structural balance until it reaches its MTO, they are referred to as being on the "adjustment path", and they shall annually report an updated target year for when they expect to reach their MTO. It is the responsibility of each Member State through a note in their annual Convergence/Stability report, to select their contemporary MTO at a point being equal to or above the "minimum MTO" calculated every third year by the European Commission (most recently in October 2012). The "minimum MTO" that the "nationally selected MTO" needs to respect, is equal to the strictest of the following three limits (which since a method change in 2012 now automatically is rounded to the lowest ¼-value, if calculated to a figure with the last two digits after punctuation differing from 00/25/50/75, i.e. -0.51% will be rounded to -0.75%):

(1) MTOMB (the Minimum Benchmark, adds a public budget safety margin to ensure the 3%-limit will be respected during economic downturns)

(2) MTOILD (the minimum value ensuring long-term sustainability of public budgets taking into account the Implicit Liabilities and Debt, aiming to ensure convergence across a long-term horizon of debt ratios towards prudent levels below 60% with due consideration to the forecast budgetary impact of ageing populations)

(3) MTOea/erm2/fc (the SGP regulation explicitly defined a -1.0% limit applying for eurozone states or ERM2 members already in 2005, but if having committed to a stricter requirement through ratification of the Fiscal Compact - then this stricter limit will replace it).

The third minimum limit listed above (MTOea/erm2/fc), mean that EU member states having ratified the Fiscal Compact and being bound by its fiscal provisions, are obliged to select a MTO which does not exceed a structural deficit of 1.0% of GDP at maximum if they have a debt-to-GDP ratio significantly below 60%, and of 0.5% of GDP maximum if they have a debt-to-GDP ratio above 60%. As of January 2015, the following six states are not bound by the fiscal provisions of the Fiscal Compact (note that for non-Eurozone states to be bound by the fiscal provisions, it is not enough just to ratify the Fiscal Compact, they also need to attach a declaration of intent to be bound by the fiscal provisions, before this is the case): UK, Czech Republic, Croatia, Poland, Sweden, Hungary. Those of the non-eurozone states neither being ERM-2 members nor having committed to respect the fiscal provisions of the Fiscal Compact, will still be required to set a national MTO respecting the calculated "minimum MTO" being equal to the strictest of requirement (1)+(2). The only EU member state being exempted to comply with this MTO procedure is the UK, as it per a protocol to the EU treaty is exempted from complying with the SGP. In other words, while all other member states are obliged nationally to select at MTO respecting their calculated Minimum MTO, the calculated Minimum MTO for the UK is only presented for advice, with no obligation for it to set a compliant national MTO in structural terms.

The Minimum MTOs are recalculated every third year by the Alternates of the Economic and Financial Committee, based on the above described procedure and formulas, that among others require the prior publication of the Commission's triennial Ageing Report. A Member State can also have its Minimum MTO updated outside the ordinary schedule, if it implement structural reforms with a major impact on the long-term sustainability of the public finances (i.e. a major pension reform) - and subsequently submit a formal request for an extraordinary recalculation. The collapsed table below, display the input data and calculated Minimum MTOs from the three latest ordinary recalculations (April 2009, October 2012 and September 2015).

Nationally selected MTOs

Whenever a "Minimum MTO" gets recalculated for a country, the announcement of a "nationally selected MTO" that is equal to or above this recalculated "Minimum MTO" shall occur as part of the following ordinary stability/convergence report, while only taking effect compliance-wise for the fiscal account(s) in the years after the new "nationally selected MTO" has been announced. The tables below have listed all country-specific MTOs selected by national governments throughout 2005-2015, and colored each year red/green to display whether or not the "nationally selected MTO" was achieved, according to the latest revision of the structural balance data as calculated by the "European Commission method". Some states, i.e. Denmark and Latvia, apply a national method to calculate the structural balance figures reported in their convergence report (which greatly differs from the results of the Commission's method), but for the sake of presenting comparable results for all Member States, the "MTO achieved" coloring of the tables (and if not met also the noted forecast year of reaching it) is decided solely by the results of the Commission's calculation method.

Note A: Setting country-specific MTOs only became mandatory starting from the 2006 fiscal year. However, Denmark and Sweden by own initiative already did so for 2005. For states without a country-specific MTO in 2005, the green/red compliance color in this specific year indicate, if the structural balance of the state complied with both the common "close to balance or surplus" (min. 0.0%) target and the country-specific "minimum benchmark". The latter only being stricter for two states in 2005, effectively setting a +0.8% target for Finland, +0.1% target for Luxembourg, and a 0.0% target for the rest of the states to respect.

Note B: Due to Eurostat implementing a significant method change for the calculation of budget balances (classifying "funded defined-contribution pension schemes" outside of the government's budget balance), which technically reduced revenues and budget balance data by 1% of GDP for states with such schemes, the earliest MTOs presented by Sweden and Denmark were technically adjusted to be 1% lower, in order to be comparable with the structural balance data calculated by the latest Eurostat method. When MTO-target compliance is checked for in 2005-07, by looking at the structural balance data calculated by the latest Eurostat method, this compliance check is conducted of the "technically-adjusted MTO-targets" rather than the "originally reported MTO-targets" for Denmark and Sweden.

Note about UK: Paragraph 4 of Treaty Protocol No 15, exempts UK from the obligation in Article 126(1+9+11) of the Treaty on the Functioning of the European Union to avoid excessive general government deficits, for as long as the state opts not to adopt the euro. Paragraph 5 of the same protocol however still provides that the "UK shall endeavour to avoid an excessive government deficit". On one hand, this means that the Commission and Council still approach the UK with EDP recommendations whenever excessive deficits are found, but on the other hand, they legally can not launch any sanctions against the UK if they do not comply with the recommendations. Due to its special exemption, the UK also did not incorporate the additional MTO adjustment rules introduced by the 2005 SGP reform and six-pack reform. Instead, the UK defined their own budget concept comprising a "Golden rule" and "Sustainable investment rule", effectively running throughout 1998-2008, which was UK's national interpretation how the SGP-regulation text should be understood.

Note about UK: Paragraph 4 of Treaty Protocol No 15, exempts UK from the obligation in Article 126(1+9+11) of the Treaty on the Functioning of the European Union to avoid excessive general government deficits, for as long as the state opts not to adopt the euro. Paragraph 5 of the same protocol however still provides that the "UK shall endeavour to avoid an excessive government deficit". On one hand, this means that the Commission and Council still approach the UK with EDP recommendations whenever excessive deficits are found, but on the other hand, they legally can not launch any sanctions against the UK if they do not comply with the recommendations. Due to its special exemption, the UK also did not incorporate the additional MTO adjustment rules introduced by the 2005 SGP reform and six-pack reform. Instead, the UK defined their own budget concept, which was operated by a "Golden rule" and "Sustainable investment rule" throughout 1998-2008 (described in detail by the table note further above), and since then by a "temporary operating rule".