| ||

The Economic and Monetary Union (EMU) is an umbrella term for the group of policies aimed at converging the economies of member states of the European Union at three stages. The policies cover the 19 eurozone states, as well as non-euro European Union states.

Contents

- History

- Stage One 1 July 1990 to 31 December 1993

- Stage Two 1 January 1994 to 31 December 1998

- Stage Three 1 January 1999 and continuing

- Criticism

- Monetary policy inflexibility

- Plans for reformed Economic and Monetary Union

- First EMU reform plan 2012 15

- Second EMU reform plan 2015 25 The Five Presidents Report

- References

Each stage of the EMU consists of progressively closer economic integration. Only once a state participates in the third stage it is permitted to adopt the euro as its official currency. As such, the third stage is largely synonymous with the eurozone. The euro convergence criteria are the set of requirements that needs to be fulfilled in order for a country to join the eurozone. An important element of this is participation for a minimum of two years in the European Exchange Rate Mechanism ("ERM II"), in which candidate currencies demonstrate economic convergence by maintaining limited deviation from their target rate against the euro.

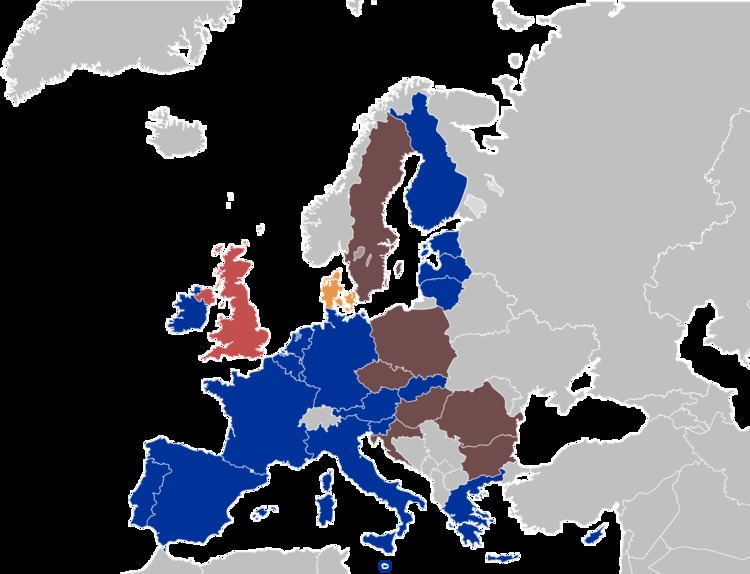

Nineteen EU member states, including most recently Lithuania, have entered the third stage and have adopted the euro as their currency. All new EU member states must commit to participate in the third stage in their treaties of accession. Only Denmark and the United Kingdom, whose EU membership predates the introduction of the euro, have legal opt outs from the EU Treaties granting them an exemption from this obligation. The remaining seven non-euro member states are obliged to enter the third stage once they comply with all convergence criteria.

History

The idea of an economic and monetary union in Europe was first raised well before establishing the European Communities. For example, the Latin Monetary Union existed from 1865-1927. In the League of Nations, Gustav Stresemann asked in 1929 for a European currency against the background of an increased economic division due to a number of new nation states in Europe after World War I.

A first attempt to create an economic and monetary union between the members of the European Communities goes back to an initiative by the European Commission in 1969, which set out the need for "greater co-ordination of economic policies and monetary cooperation," which was followed by the decision of the Heads of State or Government at their summit meeting in The Hague in 1969 to draw up a plan by stages with a view to creating an economic and monetary union by the end of the 1970s.

On the basis of various previous proposals, an expert group chaired by Luxembourg’s Prime Minister and Finance Minister, Pierre Werner, presented in October 1970 the first commonly agreed blueprint to create an economic and monetary union in three stages (Werner plan). The project experienced serious setbacks from the crises arising from the non-convertibility of the US dollar into gold in August 1971 (i.e., the collapse of the Bretton Woods System) and from rising oil prices in 1972. An attempt to limit the fluctations of European currencies, using a snake in the tunnel, failed.

The debate on EMU was fully re-launched at the Hannover Summit in June 1988, when an ad hoc committee (Delors Committee) of the central bank governors of the twelve member states, chaired by the President of the European Commission, Jacques Delors, was asked to propose a new timetable with clear, practical and realistic steps for creating an economic and monetary union. This way of working was derived from the Spaak method.

The Delors report of 1989 set out a plan to introduce the EMU in three stages and it included the creation of institutions like the European System of Central Banks (ESCB), which would become responsible for formulating and implementing monetary policy.

The three stages for the implementation of the EMU were the following:

Stage One: 1 July 1990 to 31 December 1993

Stage Two: 1 January 1994 to 31 December 1998

Stage Three: 1 January 1999 and continuing

Criticism

There have been debates as to whether the Eurozone countries constitute an optimum currency area.

There has also been a lot of doubt if all eurozone states really fulfilled a "high degree of sustainable convergence" as demanded by the Maastricht treaty as condition to join the Euro without getting into financial trouble later on.

Monetary policy inflexibility

Since membership of the eurozone establishes a single monetary policy for the respective states, they can no longer use an isolated monetary policy, e.g. to increase their competitiveness at the cost of other eurozone members by printing money and devalue, or to print money to finance excessive government deficits or pay interest on unsustainable high government debt levels. As a consequence, if member states do not manage their economy in a way that they can show a fiscal discipline (as they were obliged by the Maastricht treaty), they will sooner or later risk a sovereign debt crisis in their country without the possibility to print money as an easy way out. This is what happened to Greece, Ireland, Portugal, Cyprus, and Spain.

Plans for reformed Economic and Monetary Union

Being of the opinion that the pure austerity course was not able to solve the Euro-crisis, French President François Hollande reopened the debate about a reform of the architecture of the Eurozone. The intensification of work on plans to complete the existing EMU in order to correct its economic errors and social upheavals soon introduced the keyword "genuine" EMU. At the beginning of 2012, a proposed correction of the defective Maastricht currency architecture comprising: introduction of a fiscal capacity of the EU, common debt management and a completely integrated banking union, appeared unlikely to happen. Additionally, there were widespread fears that a process of strengthening the Union's power to intervene in eurozone member states and to impose flexible labour markets and flexible wages, might constitute a serious threat to Social Europe.

First EMU reform plan (2012-15)

In December 2012, at the height of the European sovereign debt crisis, which revealed a number of weaknesses in the architecture of the EMU, a report entitled "Towards a genuine Economic and Monetary Union" was issued by the four presidents of the Council, European Commission, ECB and Eurogroup. The report outlined the following roadmap for implementing actions being required to ensure the stability and integrity of the EMU:

Second EMU reform plan (2015-25) : The Five President's Report

In June 2015, a follow-up report entitled "Completing Europe's Economic and Monetary Union" (often referred to as the ""Five Presidents Report") was issued by the presidents of the Council, European Commission, ECB, Eurogroup and European Parliament. The report outlined a roadmap for further deepening of the EMU, meant to ensure a smooth functioning of the currency union and to allow the member states to be better prepared for adjusting to global challenges:

- Deepening the Economic Union by ensuring a new boost to convergence, jobs and growth across the entire eurozone. This shall be achieved by:

- Creation of a eurozone system of Competitiveness Authorities:

Each eurozone state shall (like Belgium and Netherlands already did) create an independent national body in charge of tracking its competitiveness performance and policies for improving competitiveness. The proposed "Eurozone system of Competitiveness Authorities" would bring together these national bodies and the Commission, which on an annual basis would coordinate the "recommendation for actions" being issued by the national Competitiveness Authorities. - Strengthened implementation of the Macroeconomic Imbalance Procedure:

(A) Its corrective arm (Excessive Imbalance Procedure) is currently only triggered if excessive imbalances are identified while the state subsequently also fails to deliver a National Reform Programme sufficiently addressing the found imbalances, and the reform implementation surveillance reports published for states with excessive imbalance but without EIP only work as a non-legal peer-pressure instrument. In the future, the EIP should be triggered as soon as excessive imbalances are identified, so that the Commission more forcefully within this legal framework can require implementation of structural reforms - followed by a period of extended reform implementation surveillance in which continued incompliance can be sanctioned.

(B) The Macroeconomic Imbalance Procedure should also better capture imbalances (external deficits) for the eurozone as a whole - not just for each individual country, and also require implementation of reforms in countries accumulating large and sustained current account surpluses (if caused by insufficient domestic demand or low growth potential). - Greater focus on employment and social performance in the European Semester:

There is no "one-size-fits-all" standard template to follow, meaning that no harmonized specific minimum standards are envisaged to be set up as compliance requirements in this field. But as the challenges often are similar across Member States, their performance and progress on the following indicators could be monitored in the future as part of the annual European Semester: (A) Getting more people of all ages into work; (B) Striking the right balance between flexible and secure labour contracts; (C) Avoiding the divide between "labor market insiders" with high protection and wages and "labor market outsiders"; (D) Shifting taxes away from labour; (E) Delivering tailored support for the unemployed to re-enter the labour market; (F) Improving education and lifelong learning; (G) Ensure that every citizen has access to an adequate education; (H) Ensure that an effective social protection system and "social protection floor" are in place to protect the most vulnerable in society; (I) Implementation of major reforms to ensure pension and health systems can continue functioning in a socially just way while coping with the rising economic expenditure pressures stemming from the rapidly ageing populations in Europe - in example by aligning the retirement age with life expectancy. - Stronger coordination of economic policies within a revamped European Semester:

(A) The Country-Specific Recommendations which are already in place as part of the European Semester, need to focus more on "priority reforms", and shall be more concrete in regards of their expected outcome and time-frame for delivery (while still granting the Member State political maneuver room on how the exact measures shall be designed and implemented).

(B) Periodic reporting on national reform implementation, regular peer reviews or a "comply-or-explain" approach should be used more systematically to hold the Member States accountable for the delivery of their National Reform Programme commitments. The Eurogroup could also play a coordinating role in cross-examining performance, with increased focus on benchmarking and pursuing best practices within the Macroeconomic Imbalance Procedure (MIP) framework.

(C) The annual cycle of the European Semester should be supplemented by a stronger multi-annual approach in line with the renewed convergence process. - Completing and fully exploiting the Single Market by creating an Energy Union and Digital Market Union.

- Complete construction of the banking union. This shall be achieved by:

- Setting up a bridge financing mechanism for the Single Resolution Fund (SRF):

Building up SRF with sufficient funds, is an ongoing process to be conducted through eight years of annual contributions made by the financial sector, as regulated by the Bank Recovery and Resolution Directive. The bridge financing mechanism is envisaged to be made available as a supplementing instrument, in order to make SRF capable straight from the first day it becomes operational (1 January 2016) to conduct potential large scale immediate transfers for resolution of financial institutions in critical need. The mechanism will only exist temporarily, until a certain level of funds have been collected by SRF. - Implementing concrete steps towards the common backstop to the SRF:

An ultimate common backstop should also be established to the SRF, for the purpose of handling rare severe crisis events featuring a total amount of resolution costs beyond the capacity of the funds held by SRF. This could be done through the issue of an ESM financial credit line to SRF, with any potential draws from this extra standby arrangement being conditioned on simultaneous implementation of extra ex-post levies on the financial industry, to ensure full repayment of the drawn funds to ESM over a medium-term horizon. - Agreeing on a common European Deposit Insurance Scheme (EDIS):

A new common deposit insurance would be less vulnerable than the current national deposit guarantee schemes, towards eruption of local shocks (in particular when both the sovereign and its national banking sector is perceived by the market to be in a fragile situation). It would also carry less risk for needing injection of additional public money to service its payment of deposit guarantees in the event of severe crisis, as failing risks would be spread more widely across all member states while its private sector funds would be raised over a much larger pool of financial institutions. EDIS would just like the national deposit guarantee schemes be privately funded through ex ante risk-based fees paid by all the participating banks in the Member States, and be devised in a way that would prevent moral hazard. Establishment of a fully-fledged EDIS will take time. A possible option would be to devise the EDIS as a re-insurance system at the European level for the national deposit guarantee schemes. - Improving the effectiveness of the instrument for direct bank recapitalisation in the European Stability Mechanism:

The ESM instrument for direct bank recapitalisation was launched in December 2014, but should soon be reviewed for the purpose of loosening its restrictive eligibility criteria (currently it only applies for systemically important banks of countries unable to function as alternative backstop themselves without endangering their fiscal stability), while there should be made no change to the current requirement for a prior resolution bail-in by private creditors and regulated SRF payment for resolution costs first to be conducted before the instrument becomes accessible. - Launch a new Capital Markets Union (CMU):

- Reinforce the European Systemic Risk Board, so that it becomes capable of detecting risks to the financial sector as a whole.

- Launch a new advisory European Fiscal Board:

- Revamp the European Semester by reorganizing it to follow two consecutive stages. The first stage (stretching from November to February) shall be devoted to the eurozone as a whole, and the second stage (stretching from March to July) then subsequently feature a discussion of country specific issues.

- Strengthen parliamentary control as part of the European Semester. This shall be achieved by:

- Plenary debate at the European Parliament first on the Annual Growth Survey and then on the Country-Specific Recommendations.

- More systematic interactions between Commissioners and national Parliaments on Country-Specific Recommendations and on national budgets.

- More systematic consultation by governments of national Parliaments and social partners before submitting National Reform and Stability Programmes.

- Increase the level of cooperation between the European Parliament and national Parliaments.

- Reinforce the steer of the Eurogroup:

- Take steps towards a consolidated external representation of the eurozone:

- Integrate intergovernmental agreements into the framework of EU law. This includes the Treaty on Stability, Coordination and Governance, the relevant parts of the Euro Plus Pact; and the Intergovernmental Agreement on the Single Resolution Fund.

- The intergovernmental European Stability Mechanism should be moved into becoming part of the EU treaty law applying automatically for all eurozone member states (something which is possible to do within existing paragraphs of the current EU treaty), in order to simplify and institutionalize its governance.

- More far-reaching measures (i.e. commonly agreed "convergence benchmark standards" of a more binding legal nature, and a treasury for the eurozone), could also be agreed to complete the EMU's economic and institutional architecture, for the purpose of making the convergence process more binding.

- Significant progress towards these new common "convergence benchmark standards" (focusing primarily on labour markets, competitiveness, business environment, public administrations, and certain aspects of tax policy like i.e. the corporate tax base) – and a continued adherence to them once they are reached – would need to be verified by regular monitoring and would be among the conditions for each eurozone Member State to meet in order to become eligible for participation in a new fiscal capacity referred to as the "economic shock absorption mechanism", which will be established for the eurozone as a last element of this second stage. The fundamental idea behind the "economic shock absorption mechanism", is that its conditional shock absorbing transfers shall be triggered long before there is a need for ESM to offer the country a conditional macroeconomic crisis support programme, but that the mechanism at the same time never shall result in permanent annual transfers - or income equalizing transfers - between countries. A first building block of this "economic shock absorption mechanism", could perhaps be establishment of a permanent version of the European Fund for Strategic Investments, in which the tap by a country into the identified pool of financing sources and future strategic investment projects could be timed to occur upon the periodic eruption of downturns/shocks in its economic business cycle.

- Another important pre-condition for the launch of the "economic shock absorption mechanism", is expected to be, that the eurozone first establish an increasing degree of "common decision-making on national budgets" and an "enhanced coordination of economic policies" (i.e. of the specific taxation and employment policies implemented by the National Job Plan of each Member State - which is published as part of their annual National Reform Programme).

All of the above three stages are envisaged to bring further progress on all four dimensions of the EMU:

- Economic union: Focusing on convergence, prosperity, and social cohesion.

- Financial union: Completing the banking union and constructing a capital markets union.

- Fiscal union: Ensuring sound and integrated fiscal policies

- Political Union: Enhancing democratic accountability, legitimacy and institutional strengthening of the EMU.