| ||

The Puerto Rican debt crisis is an ongoing financial crisis related to the amount of debt owed by the government of Puerto Rico. The island has more than $70 billion USD of outstanding debt, with a debt-to-GDP ratio of about 68%. In February 2014, various American credit rating agencies downgraded the government's debt to non-investment grade.

Contents

- Background

- Tax policy

- Disparity in federal social funding

- Triple tax exemption

- Mismanagement and disparity

- Economic depression

- Downgrade

- 2015 forbearance

- Local market

- US municipal market

- Skepticism

- Restructuring of debt

- Debt nullification

- More autonomy

- Bailout by the US federal government

- Bankruptcy

- 2016 Federal response PROMESA

- 2017 developments

- References

The crisis has caused Puerto Rico's government to adopt policies that will ideally reduce costs drastically, increase revenues, and spark economic growth so that it can better fund its debt obligations. Puerto Rico's economy has been described as precarious, weak, and fragile, and aggravated by social distrust and unpleasantness.

On August 3, 2015, Puerto Rico defaulted on a $58 million bond payment to the Public Financing Corporation, a subsidiary of the Government Development Bank, while other financial obligations were met.

In early 2017, the bond debt was again posing serious problems for the government; it was at $70 billion or $12,000 per capita at a time with 12.4% unemployment. By mid January, the cash strapped government was having difficulty maintaining health care funding. In late January, the federal control board set up under PROMESA gave the government until February 28 to present a fiscal plan (including negotiations with creditors) to solve the problems. A moratorium on lawsuits by debtors was extended to May 31.

Background

In the beginning of the 16th century, the Spaniards colonized Puerto Rico. In 1898, Puerto Rico was ceded to the United States, at the end of the Spanish–American War. Prior to that, the people of Puerto Rico had Spanish citizenship; after Puerto Rico was no longer part of Spain, the people of Puerto Rico effectively lacked citizenship from a sovereign country after it was ceded: the people of Puerto Rico were neither Puerto Rican citizens, nor American citizens, nor Spanish citizens. Because of this, on April 12, 1900, the U.S. Congress enacted the Foraker Act, establishing Puerto Rican citizenship for people born in Puerto Rico.

Four years later, the U.S. Supreme Court reaffirmed Puerto Rican citizenship in 1904 by its ruling on Gonzales v. Williams which denied that Puerto Ricans were United States citizens and labeled them as non-citizen US nationals. This ruling effectively restricted Puerto Ricans from being conscripted to US military service. Because of this and other local and mainland interests, Congress enacted the Jones–Shafroth Act on March 2, 1917, on the brink of World War I. This act granted American citizenship to the people of Puerto Rico, which allowed them to be drafted into military service.

Among the rights granted through the legislation, the Jones-Shaforth Act exempted interest payments from bonds issued by the government of Puerto Rico and its subdivisions from federal, state, and local income taxes (so called "triple tax exemption") regardless of where the bond holder resides. This right made Puerto Rican bonds attractive to municipal investors. This advantage strives from the restriction typically imposed by municipal bonds enjoying triple tax exemption where such exemptions solely apply for bond holders that reside in the state or municipal subdivision that issues them.

This factor led Puerto Rico to issue bonds that were always attractive to municipal investors, regardless of Puerto Rico's account balances. Puerto Rico thus began to issue debt to balance its budget, a practice repeated for four decades since 1973. The island also began to issue debt to repay older debt, as well as refinancing older debt possessing low interest rates with debt possessing higher interest rates.

It was not until Puerto Rico enlarged its outstanding debt to $71 billion USD —an amount approximately equal to 68% of Puerto Rico's gross domestic product (GDP)—that Puerto Rican bonds were downgraded to non-investment grade (better known as "junk status" or speculative grade) by three bond credit rating agencies between February 4–11, 2014. This downgrade triggered bond acceleration clauses that required Puerto Rico to repay certain debt instruments within months rather than years. Investors were concerned that Puerto Rico would eventually default on its debt. Such default would reduce Puerto Rico's ability to issue bonds in the future. Puerto Rico currently states that it is unable to maintain its current operations unless it takes drastic measures that may lead to civil unrest. There have already been protests over the austerity measures. These events, along with a series of governmental financial deficits and a recession, have led to Puerto Rico's current debt crisis.

Tax policy

A federal statute that contributed to the crisis was the expiration of section 936 of the U.S. Internal Revenue Code, which applied to Puerto Rico. This section was critical for the economy of the island as it established tax exemptions for U.S. corporations that settled in Puerto Rico and allowed its subsidiaries operating in the island to send their earnings to the parent corporation at any time, without paying federal tax on corporate income. The whole economy of the island based itself around this privilege, and has been unable to recoup after its loss.

Disparity in federal social funding

More than 60% of Puerto Rico's population receives Medicare or Medicaid services, with about 40% enrolled in Mi Salud, the Puerto Rican Medicaid program. There is a significant disparity in federal funding for these programs when compared to the 50 states, a situation started by Congress in 1968 when it placed a cap on Medicaid funding for United States territories. This has led to a situation where Puerto Rico might typically receive $373 million federal funding a year, while, for instance, Mississippi receives $3.6 billion. Not only does this situation lead to an exodus of underpaid health care workers to the mainland, but the disparity has had a major impact on the finances of Puerto Rico.

Triple tax exemption

Interest income paid to owners of bonds issued by the government of Puerto Rico and its subdivisions are exempt from federal, state, and local taxes (so called "triple tax exemption"). Unlike most other US triple tax exempt bonds, Puerto Rican bonds retain tax exemption regardless of where the bond holder resides in the United States, a marketing and sales advantage consequent to the restriction typically imposed on municipal bonds with triple tax exemption in which exemptions are available to bond holders that reside within the state or municipal subdivision that issues the bonds. Triple tax exempt bonds are considered subsidized because bond issuers can offer a lower interest rate to satisfy bond holders; as a result, Puerto Rico can issue more debt.

Mismanagement and disparity

The local government has proven to be highly inefficient in terms of management and planning; with some newspapers, such as El Vocero, stating that the main problem is inefficiency rather than lack of funds. As an example, the Department of Treasury of Puerto Rico is incapable of collecting 44% of the Puerto Rico Sales and Use Tax (or about $900 million USD), did not match what taxpayers reported to the department with the income reported by the taxpayer's employer through Form W-2's, and did not collect payments owned to the department by taxpayers that submitted tax returns without their corresponding payments. The Treasury department also tends to publish its comprehensive annual financial report (CAFR) late, sometimes 15 months after a fiscal year ends, while the government as a whole constantly fails to comply with its continuing disclosure obligations on a timely basis. Furthermore, the government's accounting, payroll and fiscal oversight information systems and processes also have deficiencies that significantly affect its ability to forecast expenditures.

Similarly, salaries for government employees tend to be quite disparate when compared to the private sector and other positions within the government itself. For example, a public teacher's base salary starts at $24,000 while a legislative advisor starts at $74,000. The government has also been unable to set up a system based on meritocracy, with many employees, particularly executives and administrators, simply lacking the competencies required to perform their jobs.

There was a similar situation at the municipal level with 36 out of 78 municipalities experiencing a budget deficit, putting 46% of the municipalities in financial stress. Just like the central government, the municipalities would issue debt through the Puerto Rico Municipal Financing Agency to stabilize its finances rather than make adjustments. In total, the combined debt carried by the municipalities of Puerto Rico account for $3.8 billion USD or about 5.5% of Puerto Rico's outstanding debt.

Economic depression

Puerto Rico has been experiencing an economic depression for 12 consecutive years, starting in late 2005 after a series of deficits and the expiration of the section 936 that applied to Puerto Rico of the U.S. Internal Revenue Code. The government has also experienced 17 consecutive government deficits since 2000, exacerbating its fragile economic situation as the government issued new debt to fund the payment for maturing debt.

Downgrade

Puerto Rico was effectively downgraded to non-investment grade on February 4, 2014 by Standard & Poor's when it downgraded Puerto Rico's general obligation debt (GO) from BBB- status to BB+, one level below investment grade. The agency cited liquidity concerns for its downgrade and maintained a negative outlook on its watch. Moody's would follow three days later by downgrading Puerto Rico's GO debt on February 7, 2014 from Baa3 to Ba2, two levels below investment grade. Moody's, however, cited lack of economic growth for its downgrade while assigning a negative outlook to the government's ratings. Fitch Ratings would be the last to downgrade on February 11, 2014 by downgrading Puerto Rico's GO debt from BBB- to BB, two levels below investment grade. Fitch cited both liquidity concerns and lack of economic growth for its downgrade while assigning a negative outlook to the government's ratings.

Each and every one of these downgrades triggered several acceleration clauses which forced Puerto Rico to repay certain debt instruments within months rather than years.

2015 forbearance

On June 28, 2015, in a surprising turn of events, Governor García Padilla admitted publicly that, "the debt is not payable", and that, "[if his administration doesn't make the economy grow] we will be in a death spiral". Previous to García Padilla's admittance, various government instrumentalities had already entered into forbearance agreements with their lenders but the warning still provoked a drop in Puerto Rican bonds and stocks.

Local market

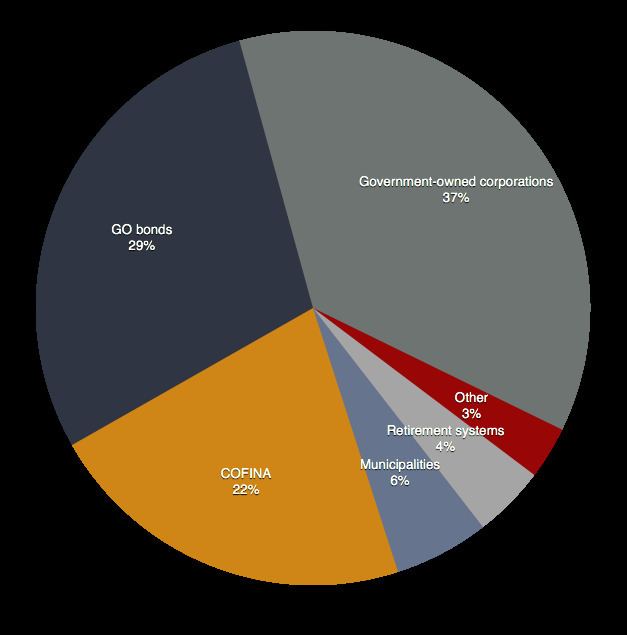

Around $30 billion or about 42% of Puerto Rico's outstanding debt is owned by residents of Puerto Rico.

The residents of Puerto Rico and its business people have been the ones bearing the hike in taxes and cuts performed by the government in order to stabilize its finances. Michele Caruso from CNBC reported on January 24, 2014 that, "Taxes and fees went up on nearly everything and everyone. Personal income taxes, corporate taxes, sales taxes, sin taxes, and taxes on insurance premiums were hiked or newly imposed. Retirement age for teachers was raised from as low as 47 to at least 55 for current teachers, and 62 for new teachers."—a significant cost to bear for a country with a purchasing power parity (PPP) per capita of $16,300 USD and with 41% of its population living below the poverty line.

The Legislative Assembly, together with the governor, also reduced operating deficits, and reformed the public employee's, teacher's, and judicial pension system. They also announced the intent to further reduce appropriations in the current fiscal year by $170 million and budget for balanced operations for the upcoming fiscal year.

As another countermeasure, the 17th Legislative Assembly of Puerto Rico enacted a bill on March 3, 2014 allowing the Puerto Rico Government Development Bank to issue $3.5 billion USD in bonds to recover its liquidity. The governor promptly signed the bill the day after, effectively becoming law as Act 34 of 2014 (Pub.L. 2014-34).

U.S. municipal market

Nearly 70% of U.S.-based municipal bond funds own Puerto Rican bonds or have some kind of exposure to Puerto Rico. A notable cause for this tendency is the fact that Puerto Rican bonds are triple tax-exempt in all of the states regardless of where the bond holder resides. Despite the expected impact, preemptive measures actually slowed the damage of the downgrade's fallout. When the downgrade began being perceived as imminent, investors were warned that it would affect the municipal market in general and concerns surrounding a worst-case default scenario were already being considered. However, by the end of February 2014, municipal bond funds that relied on specific debt were already experiencing the backlash, leaving portfolio managers with fewer options in the market. Organizations such as First Investors made it clear that they didn't intend to invest in Puerto Rico for a prolonged time period, at least until Puerto Rican bonds were restored to investment grade.

Skepticism

Several experts, including Senator Ángel Rosa, have expressed that Puerto Rico's debt is simply impossible to repay, and have thus recommended that Puerto Rico should instead negotiate payback terms with bond holders. Others, such as economist Joaquin Villamil, have found necessary that Puerto Rico issues debt at least once more to return liquidity to the Puerto Rico Government Development Bank and be henceforth able to repay back its debt.

Some, like House Minority Whip Jennifer González, claim the crisis is mere propaganda created so that the incumbent political party can enact, amend, and repeal laws that would otherwise be unable to justify. Others, such as the President of the Senate of Puerto Rico, Eduardo Bhatia, claim the crisis was created by ruthless investors wishing to profit from credit downgrades.

Restructuring of debt

The government of Puerto Rico commissioned an analysis of its financial problems asking for solutions that resulted in the "Krueger Report" published in June 2015. The report called for structural and fiscal reforms as well as for a restructuring of outstanding debts.

One month later, a report was published that rejected the need for debt restructuring. It was commissioned by a group of 34 hedge funds that specialize in distressed debt —sometimes referred to as vulture funds— who had hired economists with an IMF background. Their report indicated that Puerto Rico has a fixable deficit problem, not a debt problem. It recommended to improve tax collection and reduce public spending. The report also recommended to consider public private partnerships and to monetize government-owned buildings and ports. The report made use of data of the Krueger Report and warned that the costs of default would be high. One of the authors opined that Puerto Rico has been "massively overspending on education". Detractors remark that Puerto Rico's spending on education is only 79% of U.S. average per pupil while supporters remark that when compared to Puerto Rico's GDP such spending is extraordinarily high.

In response to the hedge fund report, Víctor Suárez Meléndez, chief of staff of the governor of Puerto Rico, indicated that "extreme austerity [alone] is not a viable solution for an economy already on its knees".

On October 14, 2015, The Wall Street Journal reported that "U.S. and Puerto Rican authorities were discussing the possibility of issuing a "superbond" as part of a restructuring package". This plan would have a designated third party administer an account holding some of the island's tax collections and those funds would be used to pay holders of the superbond. The existing Puerto Rican bondholders would take a haircut on the value of their current bond holdings.

Debt nullification

Manuel Natal and some other lawmakers have proposed not to pay that part of the debt that may have been issued in violation the Puerto Rican constitution. This strategy of "debt nullification" has been used elsewhere in the U.S. and is likely to lead to a legal challenge by creditors.

More autonomy

As Puerto Rico's financial problems are closely related to its ambiguous legal status under U.S. law, a proposed solution called to reconsider its political status so that either its autonomy would be enhanced or it would be entitled to have similar protections and rights as bestowed by statehood.

Bailout by the US federal government

On October 15, 2015, White House spokesman Josh Earnest denied reports that the US Treasury will bail out Puerto Rico.

Bankruptcy

Puerto Rico or any of its political subdivisions and agencies cannot file for debt relief under chapter 9 of the federal Bankruptcy Code because it applies only to municipalities on the mainland. Puerto Rico's nonvoting representative in the US House of Representatives, Pedro Pierluisi, introduced H.R. 870 in February 2015 seeking to give Puerto Rico's public agencies and municipalities access to chapter 9. In the US Senate, members submitted similar legislation in July 2015. But, neither bill was enacted. In December 2015, the New York Times addressed investments in Puerto Rico securities by major distressed-debt and other hedge funds. John Paulson’s firm Paulson & Co., Appaloosa Management founded by David Tepper, Marathon Asset Management, BlueMountain Capital Management and Monarch Alternative Capital were amongst purchasers of bonds in March 2014. The Times also traced opposition from the hedge funds, US Senator Marco Rubio, and Jenny Beth Martin of Tea Party Patriots to Congressional bills which would expand public-authority bankruptcy restructuring options.

2016 Federal response: PROMESA

On June 30, 2016 President Obama signed the Puerto Rico Oversight, Management and Economic Stability Act, or PROMESA, a law creating a federal oversight board that would negotiate the restructuring of Puerto Rico's debt. With the protection this bill gave from lawsuits, the governor of Puerto Rico, Alejandro Garcia Padilla, suspended payments due on July 1.

PROMESA enables the island's government to enter a bankruptcy-like restructuring process and halts litigation in case of default. The task of the oversight board is to facilitate negotiations, or, if these fail, bring about a court-supervised process akin to a bankruptcy. The board is also responsible for overseeing and monitoring sustainable budgets.

2017 developments

By mid January 2017, the bond debt had reached $70 billion or $12,000 per capita in a territory with a 45 percent poverty rate and double digit unemployment (12.4%, Dec. 2016) that is more than twice the mainland U.S. average. The debt had been increasing during a decade long recession.

The Commonwealth defaulted on many debts, including bonds, since 2015. The cash strapped government was having difficulty maintaining health care funding. "Without action before April, Puerto Rico’s ability to execute contracts for Fiscal Year 2018 with its managed care organizations will be threatened, thereby putting at risk beginning July 1, 2017 the health care of up to 900,000 poor U.S. citizens living in Puerto Rico," according to a letter sent to Congress by the Secretary of the Treasury and the Secretary of Health and Human Services. They also said that "Congress must enact measures recommended by both Republicans and Democrats that fix Puerto Rico’s inequitable health care financing structure and promote sustained economic growth."

Newly elected governor Ricardo Rosselló discussed the situation in an interview with the international Financial Times in January and indicated that he would seek an amicable resolution with creditors and also make fiscal reforms. "There will be real fiscal oversight and we are willing to sit down. We are taking steps to make bold reforms. ... What we are asking for is runway to establish these reforms and have Washington recognize that they have a role to play." He had instructed Puerto Rican government agencies to cut operating expenses by 10 per cent and reduce political appointees by 20 percent. With debt payments due, he faced the risk of a government shutdown.

Initially, the oversight board created under PROMESA called for Puerto Rico's governor to deliver a fiscal turnaround plan by January 28. Puerto Rico must reach restructuring deals with its creditors to avoid a bankruptcy-like process under PROMESA. In late January 2017, the control board extended the deadline it gave the government to February 28 to present a fiscal plan which including negotiations with creditors for restructuring debt. A moratorium on lawsuits by debtors was extended to May 31.

Governor Rosselló hired investment expert Rothschild & Co in January 2017 to assist in convincing creditors to take deeper losses than they had expected on Puerto Rico's debts. The company also explored the possibility of convincing insurers that had guaranteed some of the bonds against default, to contribute more to the restructuring, according to reliable sources. The governor also planned to negotiate restructuring of about $9 billion of electric utility debt, a plan that could result "in a showdown with insurers". Political observers suggest that his negotiation of the electrical utility debt indicated Rosselló's intention to take a harder line with creditors. Puerto Rico has received authority from the federal government to reduce its debt with legal action and this may make creditors more willing to negotiate instead of becoming embroiled in a long and costly legal battle.