| ||

Money creation (also known as credit creation) is the process by which the money supply of a country or a monetary region (such as the Eurozone) is increased. A central bank may introduce new money into the economy (termed "expansionary monetary policy", or by detractors "printing money") by purchasing financial assets or lending money to financial institutions. However, in most countries today, most of the money supply is in the form of bank deposits, which is created by private banks in a fractional reserve banking system. Bank lending increases the amount of broad money beyond the amount of base money originally created by the central bank. Reserve requirements, capital adequacy ratios, and other policies of the central bank influence this process.

Contents

- Money creation by the central bank

- Physical currency

- Quantitative easing

- Monetary financing

- Money creation by commercial banks

- Re lending

- Money multiplier

- Alternative theories

- References

Central banks monitor the amount of money in the economy by measuring monetary aggregates such as M2. The effect of monetary policy on the money supply is indicated by comparing these measurements on various dates. For example, in the United States, money supply measured as M2 grew from $6.407 trillion in January 2005, to $8.319 trillion in January 2009.

Money creation by the central bank

Monetary policy regulates a country's money supply, the amount of broad currency in circulation. Almost all modern nations have central banks such as the United States Federal Reserve System, the European Central Bank (ECB), and the People's Bank of China for conducting monetary policy. Charged with the smooth functioning of the money supply and financial markets, these institutions are generally independent of the government executive.

The primary tool of monetary policy is open market operations: the central bank buys and sells financial assets such as treasury bills, government bonds, or foreign currencies from private parties. Purchases of these assets result in currency entering market circulation, while sales of these assets remove currency. Usually, open market operations are designed to target a specific short-term interest rate. For example, the U.S. Federal Reserve may target the federal funds rate, the rate at which member banks lend to one another overnight. In other instances, they might instead target a specific exchange rate relative to some foreign currency, the price of gold, or indices such as the consumer price index.

Other monetary policy tools to expand the money supply include decreasing interest rates by fiat; increasing the monetary base; and decreasing reserve requirements. Some other means are: discount window lending (as lender of last resort); moral suasion (cajoling the behavior of certain market players); and "open mouth operations" (publicly asserting future monetary policy). The conduct and effects of monetary policy and the regulation of the banking system are of central concern to monetary economics.

Physical currency

In modern economies, relatively little of the supply of broad money is in physical currency. For example, in December 2010 in the United States, of the $8.853 trillion in broad money supply (M2), only about 10% (or $915.7 billion) consisted of physical coins and paper money. The manufacturing of new physical money is usually the responsibility of the central bank, or sometimes, the government's treasury.

Contrary to popular belief, money creation in a modern economy does not directly involve the manufacturing of new physical money, such as paper currency or metal coins. Instead, when the central bank expands the money supply through open market operations (e.g., by purchasing government bonds or commercial bank assets), it credits the accounts that the government or commercial banks hold at the central bank (termed high-powered money). Governments or commercial banks may draw on these accounts to withdraw physical money from the central bank. Commercial banks may also return soiled or spoiled currency to the central bank in exchange for new currency.

Quantitative easing

Quantitative easing (QE) involves the creation of a significant amount of new base money by a central bank by the buying of assets that it usually does not buy. Usually, a central bank will conduct open market operations by buying short-term government bonds or foreign currency. However, during a financial crisis, the central bank may buy other types of financial assets as well. The central bank may buy long-term government bonds, company bonds, asset-backed securities, stocks, or even extend commercial loans. The intent is to stimulate the economy by increasing liquidity and promoting bank lending, even when interest rates cannot be pushed any lower.

Quantitative easing increases reserves in the banking system (i.e., deposits of commercial banks at the central bank), giving depository institutions the ability to make new loans. Quantitative easing is usually used when lowering the discount rate is no longer effective because interest rates are already close to or at zero. In such a case, normal monetary policy cannot further lower interest rates, and the economy is in a liquidity trap.

Monetary financing

In principle, central banks can create money de novo in order to finance public spending. This concept is known somewhat misleadingly as debt monetization.

Monetary financing used to be standard monetary policy in many countries including Canada or France. Under the influence of Monetarism, monetary financing has been gradually prohibited by law in many countries, under the rationale that monetary financing is always inflationary.

In the Eurozone for example, article 123 of the Lisbon Treaty explicitly prohibits the European Central Bank from financing public institutions.

Money creation by commercial banks

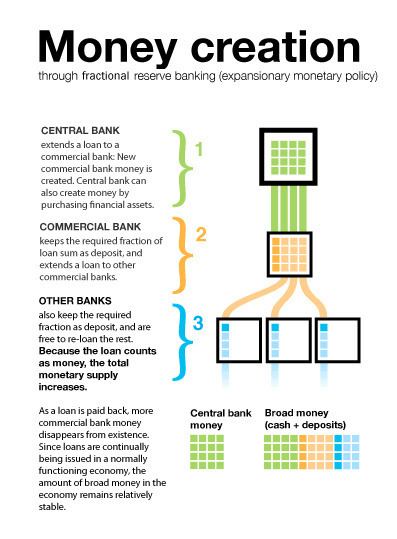

In contemporary monetary systems, most money in circulation exists not as cash or coins created by the central bank, but as bank deposits. Commercial bank lending expands the amount of bank deposits. Through fractional reserve banking, the modern banking system expands the money supply of a country beyond the amount initially created by the central bank, creating most of the broad money in the system.

There are two types of money in a fractional-reserve banking system: currency originally issued by the central bank, and bank deposits at commercial banks:

- Central bank money (all money created by the central bank regardless of its form, e.g., banknotes, coins, electronic money)

- Commercial bank money (money created in the banking system through borrowing and lending) – sometimes referred to as checkbook money

When a commercial bank loan is extended, new commercial bank money is created if the loan proceeds are issued in the form of an increase in a customer's demand deposit account (that is, an increase in the bank's demand deposit liability owed to the customer). As a loan is paid back through reductions in the demand deposit liabilities the bank owes to a customer, that commercial bank money disappears from existence. Because loans are continually being issued in a normally functioning economy, the amount of broad money in the economy remains relatively stable. Because of this money creation process by the commercial banks, the money supply of a country is usually a multiple larger than the money issued by the central bank; that multiple was traditionally determined by the reserve requirements and now essentially by other financial ratios (primarily the capital adequacy ratio that limits the overall credit creation of a bank) set by the relevant banking regulators in the jurisdiction.

Re-lending

An early table, featuring reinvestment from one period to the next and a geometric series, is found in the tableau économique of the Physiocrats, which is credited as the "first precise formulation" of such interdependent systems and the origin of multiplier theory.

Money multiplier

The most common mechanism used to measure this increase in the money supply is typically called the money multiplier. It calculates the maximum amount of money that an initial deposit can be expanded to with a given reserve ratio – such a factor is called a multiplier. It is the maximum amount of money commercial banks can legally create for a given quantity of reserves.

It is calculated as

Where

In the re-lending model, this is alternatively calculated as a geometric series under repeated lending of a geometrically decreasing quantity of money: reserves lead loans. In endogenous money models, loans lead reserves, and it is not interpreted as a geometric series. In practice, because banks often have access to lines of credit, and the money market, and can use day time loans from central banks, there is often no requirement for a pre-existing deposit for the bank to create a loan and have it paid to another bank.

If banks accumulate excess reserves, as occurred in such financial crises as the Great Depression and the Financial crisis of 2007–2008 – in the United States since October 2008, the relationship between base money and broad money breaks down, and central bank money creation may not result in commercial bank money creation, instead remaining as unlent (excess) reserves. However, the central bank may shrink commercial bank money by shrinking central bank money, since reserves are required – thus fractional-reserve money creation is likened to a string, since the central bank can always pull money out by restricting central bank money, hence reserves, but cannot always push money out by expanding central bank money, since this may result in excess reserves, a situation referred to as "pushing on a string".

Alternative theories

There are also heterodox theories of how money is created. These include: