| ||

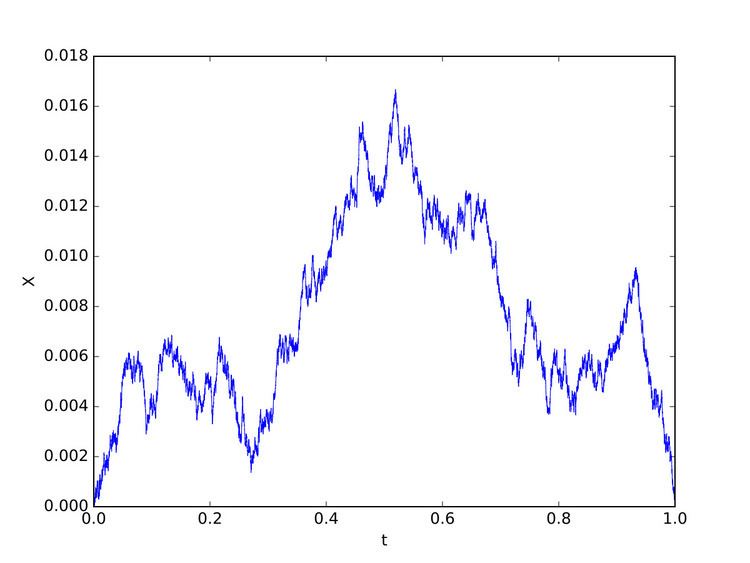

In probability theory a Brownian excursion process is a stochastic processes that is closely related to a Wiener process (or Brownian motion). Realisations of Brownian excursion processes are essentially just realizations of a Wiener process selected to satisfy certain conditions. In particular, a Brownian excursion process is a Wiener process conditioned to be positive and to take the value 0 at time 1. Alternatively, it is a Brownian bridge process conditioned to be positive. BEPs are important because, among other reasons, they naturally arise as the limit process of a number of conditional functional central limit theorems.

Contents

Definition

A Brownian excursion process,

Another representation of a Brownian excursion

Let

Properties

Vervaat's representation of a Brownian excursion has several consequences for various functions of

(this can also be derived by explicit calculations) and

The following result holds:

and the following values for the second moment and variance can be calculated by the exact form of the distribution and density:

Groeneboom (1989), Lemma 4.2 gives an expression for the Laplace transform of (the density) of

Groeneboom (1983) and Pitman (1983) give decompositions of Brownian motion

For an introduction to Itô's general theory of Brownian excursions and the Itô Poisson process of excursions, see Revuz and Yor (1994), chapter XII.

Connections and applications

The Brownian excursion area

arises in connection with the enumeration of connected graphs, many other problems in combinatorial theory; see e.g. , , , , , and the limit distribution of the Betti numbers of certain varieties in cohomology theory . Takacs (1991a) shows that

where

and

They also give higher-order expansions in both cases.

Janson (2007) gives moments of

Brownian excursions also arise in connection with queuing problems, railway traffic, and the heights of random rooted binary trees.