| ||

Introduction to bayesian econometrics

Bayesian econometrics is a branch of econometrics which applies Bayesian principles to economic modelling. Bayesianism is based on a degree-of-belief interpretation of probability, as opposed to a relative-frequency interpretation.

Contents

- Introduction to bayesian econometrics

- Be prelec01 convergence of frequencies to probabilities

- Basics

- History

- Current research topics

- References

The Bayesian principle relies on Bayes' theorem which states that the probability of B conditional on A is the ratio of joint probability of A and B divided by probability of B. Bayesian econometricians assume that coefficients in the model have prior distributions.

This approach was first propagated by Arnold Zellner.

Be prelec01 convergence of frequencies to probabilities

Basics

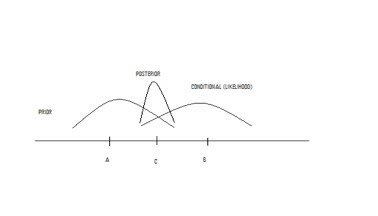

Subjective probabilities have to satisfy the standard axioms of probability theory if one wishes to avoid losing a bet regardless of the outcome. Before the data is observed, the parameter

where

where

The posterior function is given by

History

The ideas underlying Bayesian statistics were developed by Rev. Thomas Bayes during the 18th century and later expanded by Pierre-Simon Laplace. As early as 1950, the potential of the Bayesian inference in econometrics was recognized by Jacob Marschak. The Bayesian approach was first applied to econometrics in the early 1960s by W. D. Fisher, Jacques Drèze, Clifford Hildreth, Thomas J. Rothenberg, George Tiao, and Arnold Zellner. The central motivation behind these early endeavors in Bayesian econometrics was the combination of the parameter estimators with available uncertain information on the model parameters that was not included in a given model formulation. From the mid-1960s to the mid-1970s, the reformulation of econometric techniques along Bayesian principles under the traditional structural approach dominated the research agenda, with Zellner's An Introduction to Bayesian Inference in Econometrics in 1971 as one of its highlights, and thus closely followed the work of frequentist econometrics. Therein, the main technical issues were the difficulty of specifying prior densities without losing either economic interpretation or mathematical tractability and the difficulty of integral calculation in the context of density functions. The result of the Bayesian reformulation program was to highlight the fragility of structural models to uncertain specification. This fragility came to motivate the work of Edward Leamer, who emphatically criticized modelers' tendency to indulge in "post-data model construction" and consequently developed a method of economic modelling based on the selection of regression models according to the types of prior density specification in order to identify the prior structures underlying modelers' working rules in model selection explicitly. Bayesian econometrics also became attractive to Christopher Sims' attempt to move from structural modeling to VAR modeling due to its explicit probability specification of parameter restrictions. Driven by the rapid growth of computing capacities from the mid-1980s on, the application of Markov chain Monte Carlo simulation to statistical and econometric models, first performed in the early 1990s, enabled Bayesian analysis to drastically increase its influence in economics and econometrics.

Current research topics

Since the beginning of the 21st century, research in Bayesian econometrics has concentrated on: