| ||

Valuation using discounted cash flows is a method for determining the current value of a company using future cash flows adjusted for time value. The future cash flow set is made up of the cash flows within the determined forecast period and a continuing value that represents the cash flow stream after the forecast period. Discounted Cash Flow valuation was used in industry as early as the 1700s or 1800s, widely discussed in financial economics in the 1960s, and became widely used in U.S. Courts in the 1980s and 1990s.

Contents

Basic formula for firm valuation using DCF model

value of firm =

where

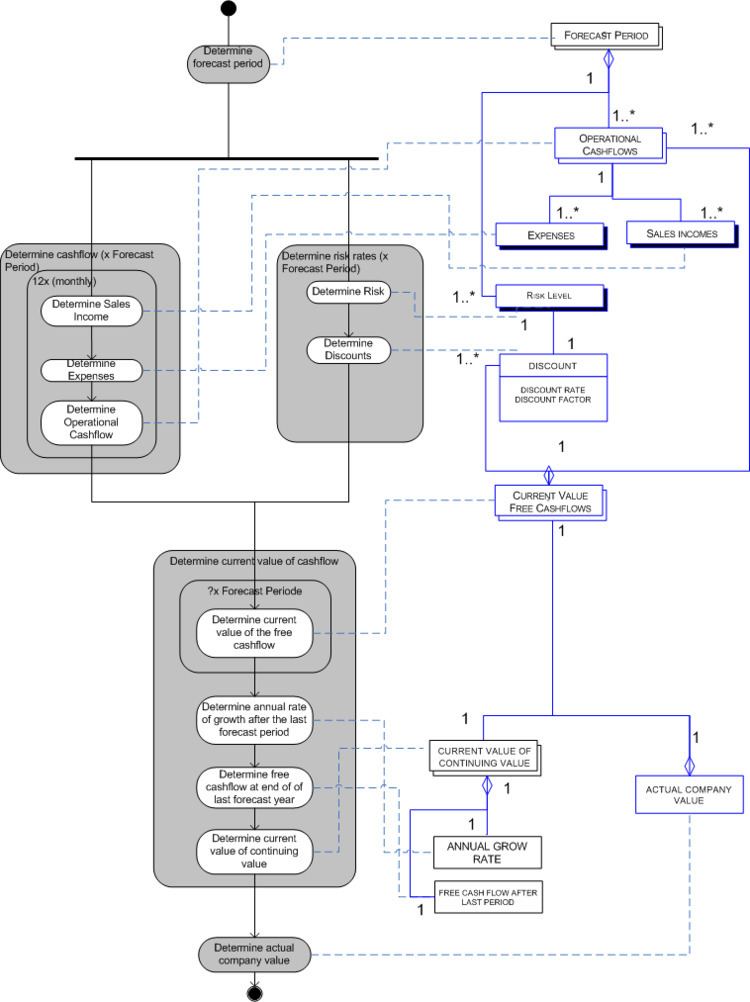

Process Data Diagram

The following diagram shows an overview of the process of company valuation. All activities in this model are explained in more detail in section 3: Using the DCF method.

Determine Forecast Period

The forecast period is the time period for which the individual yearly cash flows are input to the DCF formula. Cash flows after the forecast period can only be represented by a fixed number such as annual growth rates. There are no fixed rules for determining the duration of the forecast period.

Example:

‘MedICT’ is a medical ICT startup that has just finished their business plan. Their goal is to provide medical professionals with software solutions for doing their own bookkeeping. Their only investor is required to wait for 5 years before making an exit. Therefore MedICT is using a forecast period of 5 years.

Determine the yearly Cash Flow

Cash flow

Example: MedICT has chosen to use only operational cash flows in determining their estimated yearly cash flow:

In thousand $

Determine Discount Factor / Rate

Determine the appropriate discount rate and discount factor for each year of the forecast period based on the risk level associated with the company and its market.

Example:

MedICT has chosen their discount rates based upon their company maturity.

Determine Current Value

Calculate the current value of the future cash flows by multiplying each yearly cash flow by the discount factor for the year in question. This is known as the time value of money.

Example:

Total current value = 62.14

Determine the Continuing Value

Calculating cash flows after the forecast period is much more difficult as uncertainty, and therefore the risk factor rises with each additional year into the future. The continuing value, or terminal value, is a solution that represents the cash flows after the forecast period.

Example:

MedICT has chosen the perpetuity growth model to calculate the value of cash flows after the forecast period. They estimate that they will grow at about 6% for the rest of these years.

(182*1.06 / (0.25-0.06)) = 1015.34 This value however is a future value that still needs to be discounted to a current value: 1015.34 * 1/(1.25)^5 = 332.72

Determining Equity Value

The value of the equity can be calculated by subtracting any outstanding debts from the total of all discounted cash flows.

Example:

MedICT doesn’t have any debt so it only needs to add up the current value of the continuing value and the current value of all cash flows during the forecast period:

62.14 + 332.72= 394.86 The equity value of MedICT : $394.86