| ||

The United States debt ceiling or debt limit is a legislative limit on the amount of national debt that can be issued by the US Treasury, thus limiting how much money the federal government may borrow. The debt ceiling is an aggregate figure which applies to the gross debt, which includes debt in the hands of the public and in intra-government accounts. (About 0.5% of debt is not covered by the ceiling.) Because expenditures are authorized by separate legislation, the debt ceiling does not directly limit government deficits. In effect, it can only restrain the Treasury from paying for expenditures and other financial obligations after the limit has been reached, but which have already been approved (in the budget) and appropriated.

Contents

- Background

- Relationship to federal budget

- Legislative history

- 1995 debt ceiling crisis

- 2011 debt ceiling crisis

- 2013 debt ceiling crisis

- Debt not covered by ceiling

- Suspension of debt ceiling

- Extraordinary measures

- Default on financial obligations

- Debate on debt ceiling

- References

When the debt ceiling is actually reached without an increase in the limit having been enacted, Treasury will need to resort to "extraordinary measures" to temporarily finance government expenditures and obligations until a resolution can be reached. The Treasury has never reached the point of exhausting extraordinary measures, resulting in default, although on some occasions, Congress appeared like it would allow a default to take place. If this situation were to occur, it is unclear whether Treasury would be able to prioritize payments on debt to avoid a default on its bond obligations, but it would at least have to default on some of its non-bond payment obligations. A protracted default could trigger a variety of economic problems including a financial crisis, and a decline in output that would put the country into an economic recession.

Management of the United States public debt is an important part of the macroeconomics of the United States economy and finance system, and the debt ceiling is a constraint on the executive's ability to manage the U.S. economy. There is debate, however, on how the U.S. economy should be managed, and whether a debt ceiling is an appropriate mechanism for restraining government spending.

Background

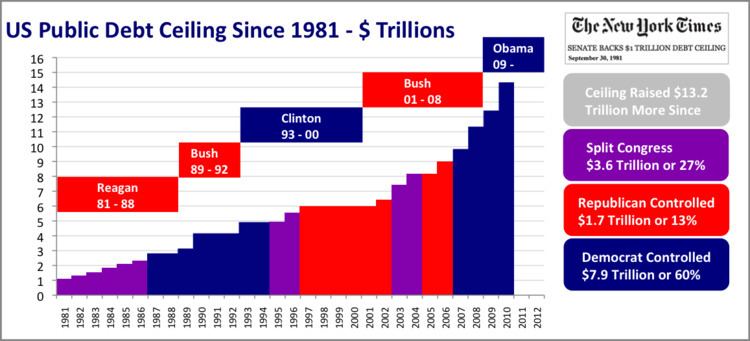

Under Article I Section 8 of the United States Constitution, only Congress can authorise the borrowing of money on the credit of the United States. From the founding of the United States until 1917, Congress directly authorized each individual debt issued. To provide more flexibility to finance the United States' involvement in World War I, Congress modified the method by which it authorized debt in the Second Liberty Bond Act of 1917. Under this Act, Congress established an aggregate limit, or "ceiling," on the total amount of new bonds that could be issued.

The present debt ceiling is an aggregate limit applied to nearly all federal debt, which was substantially established by the Public Debt Acts of 1939 and 1941 which have subsequently been amended to change the ceiling amount.

From time to time, political disputes arise when the Treasury advises Congress that the debt ceiling is about to be reached and indicating that a default is imminent. When the debt ceiling is reached, and pending an increase in the limit, Treasury may resort to "extraordinary measures" to buy more time before the ceiling can be raised by Congress. The United States has never reached the point of default where Treasury was incapable of paying U.S. debt obligations, though it has been close on several occasions. The only exception was during the War of 1812 when parts of Washington D.C. including the Treasury were burned.

In 2011, the United States reached a crisis point of near default on public debt. The delay in raising the debt ceiling resulted in the first downgrade in the United States credit rating, a sharp drop in the stock market, and an increase in borrowing costs. Congress raised the debt limit with the Budget Control Act of 2011, which added to the fiscal cliff when the new ceiling was reached on December 31, 2012.

Another debt ceiling crisis arose in early 2013 when the ceiling was reached again, and Treasury adopted extraordinary measures to avoid a default. The 2013 crisis was resolved, for the time being, on February 4, 2013, President Barack Obama signed the No Budget, No Pay Act of 2013 to, besides other things, suspend the debt ceiling until May 19, 2013. After May 19, the debt ceiling was raised to $16.699 trillion, the level of debt incurred during the suspension, and Treasury resumed extraordinary measures. Treasury Secretary Jack Lew notified Congress that these measures would be exhausted by October 17, 2013. On October 7, 2013 Treasury indicated that the debt ceiling and extraordinary measures will be exhausted and that a default will occur on October 17 when interest payments are due.

The debt ceiling would again have been reached on November 3, 2015. On October 30, 2015 the debt ceiling was again suspended to March 2017.

Relationship to federal budget

The process of setting the debt ceiling is separate and distinct from the United States budget process, and raising the debt ceiling neither directly increases nor decreases the budget deficit, and vice versa. The Government Accountability Office explains, "the debt limit does not control or limit the ability of the federal government to run deficits or incur obligations. Rather, it is a limit on the ability to pay obligations already incurred."

The President formulates a federal budget every year, which Congress must pass, sometimes with amendments, in a concurrent resolution, which does not require the President's signature and is not binding. The budget details projected tax collections and expenditures and, therefore, specifies the amount of borrowing the government would have to do in that fiscal year.

Legislative history

Prior to 1917, the United States had no debt ceiling. Congress either authorized specific loans or allowed Treasury to issue certain debt instruments and individual debt issues for specific purposes. Sometimes Congress gave Treasury discretion over what type of debt instrument would be issued. The United States first instituted a statutory debt limit with the Second Liberty Bond Act of 1917. This legislation set limits on the aggregate amount of debt that could be accumulated through individual categories of debt (such as bonds and bills). In 1939, Congress instituted the first limit on total accumulated debt over all kinds of instruments.

Prior to the Budget and Impoundment Control Act of 1974, the debt ceiling played an important role enabling Congress to hold hearings and debates on the budget. James Surowiecki argued that the debt ceiling lost its usefulness after these reforms to the budget process.

In 1979, noting the potential problems of hitting a default, Dick Gephardt imposed the "Gephardt Rule," a parliamentary rule that deemed the debt ceiling raised when a budget was passed. This resolved the contradiction in voting for appropriations but not voting to fund them. The rule stood until it was repealed by Congress in 1995.

President Ronald Reagan fought bi-partisan resistance from Congress for a 1981 raising of the debt limit.

1995 debt ceiling crisis

The debt-ceiling debate of 1995 led to a showdown on the federal budget, which did not pass, and resulted in the United States federal government shutdown of 1995 and 1996.

2011 debt ceiling crisis

In 2011, Republicans in Congress demanded deficit reduction as part of raising the debt ceiling. The resulting contention was resolved on 2 August 2011 by the Budget Control Act of 2011.

On 5 August 2011, S&P issued the first ever downgrade in the federal government's credit rating, citing their April warnings, the difficulty of bridging the parties and that the resulting agreement fell well short of the hoped-for comprehensive 'grand bargain'. The credit downgrade and debt ceiling debacle contributed to the Dow Jones Industrial Average falling nearly 2,000 points in late July and August. Following the downgrade itself, the DJIA had one of its worst days in history and fell 635 points on August 8.

2013 debt ceiling crisis

Following the increase in the debt ceiling to $16.394 trillion in 2011, the United States again reached the debt ceiling on December 31, 2012 and the Treasury began taking extraordinary measures. The fiscal cliff was resolved with the passage of the American Taxpayer Relief Act of 2012 (ATRA), but no action was taken on the debt ceiling. Following the tax cuts from ATRA, the government needed to raise the debt ceiling by $700 billion to finance operations for the rest of the 2013 fiscal year. Extraordinary measures were expected to be exhausted by February 15. The Treasury had said it is not set up to prioritize payments, and has given the opinion that it is unclear whether it would be legal to do so. Given this situation, the Treasury would simply delay payments if funds could not be raised through extraordinary measures and the debt ceiling not raised. Economists estimated that such an action would cause GDP to contract by 7%, which is larger than the contraction during the Great Recession. The economic damage would worsen as recipients of social security benefits, government contracts, and other government payments cut back on spending in response to having the freeze in their revenue.

Under the No Budget, No Pay Act of 2013, both houses of Congress voted to suspend the debt ceiling from February 4, 2013 until May 19, 2013. On May 19, the debt ceiling was raised to approximately $16.699 trillion to accommodate the borrowing done during the suspension period.

Debt not covered by ceiling

As at October 2013, about 0.5% of debt was not covered by the ceiling. This includes outstanding pre-1917 debt.

In December 2012, Treasury calculated that $239 million in United States Notes were in circulation. These Notes, in accordance the debt ceiling legislation, are excluded from the statutory debt limit. The $239 million excludes $25 million in United States Notes issued prior to July 1, 1929, determined pursuant to Act of June 30, 1961, 31 U.S.C. 5119, to have been destroyed or irretrievably lost.

Debts of the Federal Financing Bank which at August 2013 totalled $73.1 billion are also not subject to the ceiling.

Suspension of debt ceiling

The No Budget, No Pay Act of 2013 suspended, for the first time, the U.S. debt ceiling on February 4, 2013 until May 18, 2013. During the suspension period, Treasury was authorized to borrow to the extent that it "is required to meet existing commitments". On May 19, the debt ceiling was raised by $306 billion to cover the borrowings done during the suspension period, as well as commitments that accrued in the preceding period that extraordinary measures were in place, which commenced on December 31, 2012. The debt ceiling was again suspended on October 17 until February 7, 2014. On February 12, 2014, the Temporary Debt Limit Extension Act was passed, suspending the debt ceiling until March 15, 2015. At that time, the Treasury Department took extraordinary measures. On October 30, 2015 the debt ceiling was again suspended to March 2017.

Extraordinary measures

The Treasury Department is permitted to borrow funds needed to fund government operations, as had been authorized by congressional appropriations, up to the debt ceiling, with some small exceptions. In a letter to Congress of April 4, 2011, Treasury Secretary Timothy Geithner explained that when the debt ceiling is reached, Treasury can declare a "debt issuance suspension period" during which it can take "extraordinary measures" to continue meeting federal obligations provided that it does not involve the issue of new debt. These measures are taken to avoid, as far as resources permit, a partial government shutdown or a default on the debt. These methods have been used on several previous occasions in which federal debt neared its statutory limit.

Extraordinary measures can include suspending investments in the G Fund of the Thrift Savings Plan of individual retirement funds of federal employees. In 2011, extraordinary measures included suspending investments in the Civil Service Retirement and Disability Fund (CSRDF), the Postal Service Retiree Health Benefits Fund (Postal Benefits Fund), and the Exchange Stabilization Fund (ESF). In addition, certain CSRDF investments were also redeemed early. In 1985, the Treasury had also exchanged Treasury securities for non-Treasury securities held by the Federal Financing Bank.

However, these amounts are not sufficient to cover government operations for extended periods. Treasury first implemented these measures on December 16, 2009 to avoid a government shutdown. These measures were implemented again on May 16, 2011, when Treasury Secretary Geithner declared a "debt issuance suspension period". According to his letter to Congress, this period could "last until August 2, 2011, when the Department of the Treasury projects that the borrowing authority of the United States will be exhausted".

The measures were again implemented on December 31, 2012 being the start of the debt ceiling crisis of 2013 with the default trigger date ticking to February 2013. The crisis was deferred with the suspension of the limit on February 4, and the cancellation of the extraordinary measures. The measures were again invoked at the end of the ceiling's suspension on May 19, 2013 with the date of exhaustion of the resources and the default trigger date being estimated by Treasury as October 17. The ceiling was again suspended by legislation on that date until February 4, 2014.

Default on financial obligations

If the debt ceiling is not raised and extraordinary measures are exhausted, the United States government is legally unable to borrow money to pay its financial obligations. At that point, it must cease making payments unless the treasury has cash on hand to cover them. In addition, the government would not have the resources to pay the interest on (and sometime redeem) government securities when due, which would be characterized as a default. A default may affect the United States' sovereign risk rating and the interest rate that it will be required to pay on future debt. The United States has never defaulted on its financial obligations, but the periodic crises relating to the debt ceiling has led to a rating downgrade by several rating agencies and a warning by others. The GAO estimated that the delay in raising the debt ceiling during the debt ceiling crisis of 2011 raised borrowing costs for the government by $1.3 billion in fiscal year 2011 and noted that the delay would also raise costs in later years. The Bipartisan Policy Center extended the GAO's estimates and found that the delay raised borrowing costs by $18.9 billion over ten years.

Some writers have expressed the view that if extraordinary measures are exhausted, the executive branch has the authority to determine which obligations are paid and which are not, though Treasury has argued that all obligations are on equal footing under the law. The writers have argued that the executive branch can choose to prioritize interest payments on bonds, which would avoid an immediate, direct default on sovereign debt. During the debt ceiling crisis of 2011, Treasury Secretary Timothy Geitner argued that prioritization of interest payments would not help since government expenditures would have needed to be cut by an unrealistic 40% if the debt ceiling is not raised. Also, a default on non-debt obligations would still undermine American creditworthiness according to at least one rating agency. In 2011, the Treasury suggested that it could not prioritize certain types of expenditures because all expenditures are on equal footing under the law. In this view, when extraordinary measures are exhausted, no payments could be made except when money (such as tax receipts) is in the treasury, at all and the United States would be in default on all of its obligations. The CBO notes that prioritization would not avoid the technical definition found in Black's Law Dictionary where default is defined as “the failure to make a payment when due.”

Debate on debt ceiling

A vote to increase the debt ceiling has usually been (since the 1950s) a legal budgetary formality between the President and Congress. The debt ceiling has not historically been a political issue that would make the elected government fail to pass a yearly budget. Reports to Congress (from the OMB and other sources) in the 1990s have repeatedly stated that the debt limit is an ineffective means to restrain the growth of debt.

James Surowiecki argues that the debt ceiling originally served a useful purpose. When introduced, presidents had stronger authority to borrow and spend as they pleased. However, after 1974 and the Nixon Administration the US Congress began passing comprehensive budget resolutions that specify exactly how much money the government could spend.

The apparent redundancy of the debt ceiling has led to suggestions that it should be abolished altogether. Several Democratic House members, including Peter Welch, proposed abolishing the debt ceiling. The proposal found support from some economists such as Jacob Funk Kirkegaard, a senior fellow at the Peterson Institute for International Economics.

In January 2013, a survey of 38 highly regarded economists found that 84% agreed that, since Congress already approves spending and taxation, "a separate debt ceiling that has to be increased periodically creates unneeded uncertainty and can potentially lead to worse fiscal outcomes." Only one member of the panel, Luigi Zingales, disagreed with the statement. Rating agency Moody's has stated that "the debt limit creates a high level of uncertainty" and that the government should change "its framework for managing government debt to lessen or eliminate that uncertainty".