| ||

Uncertainty theory is a branch of mathematics based on normality, monotonicity, self-duality, countable subadditivity, and product measure axioms. It was founded by Baoding Liu in 2007 and refined in 2009.

Contents

- Four axioms

- Uncertain variables

- Uncertainty distribution

- Independence

- Operational law

- Expected Value

- Variance

- Critical value

- Entropy

- Inequalities

- Convergence concept

- Conditional uncertainty

- References

Mathematical measures of the likelihood of an event being true include probability theory, capacity, fuzzy logic, possibility, and credibility, as well as uncertainty.

Four axioms

Axiom 1. (Normality Axiom)

Axiom 2. (Self-Duality Axiom)

Axiom 3. (Countable Subadditivity Axiom) For every countable sequence of events Λ1, Λ2, ..., we have

Axiom 4. (Product Measure Axiom) Let

Principle. (Maximum Uncertainty Principle) For any event, if there are multiple reasonable values that an uncertain measure may take, then the value as close to 0.5 as possible is assigned to the event.

Uncertain variables

An uncertain variable is a measurable function ξ from an uncertainty space

Uncertainty distribution

Uncertainty distribution is inducted to describe uncertain variables.

Definition:The uncertainty distribution

Theorem(Peng and Iwamura, Sufficient and Necessary Condition for Uncertainty Distribution) A function

Independence

Definition: The uncertain variables

for any Borel sets

Theorem 1: The uncertain variables

for any Borel sets

Theorem 2: Let

Theorem 3: Let

for any real numbers

Operational law

Theorem: Let

where

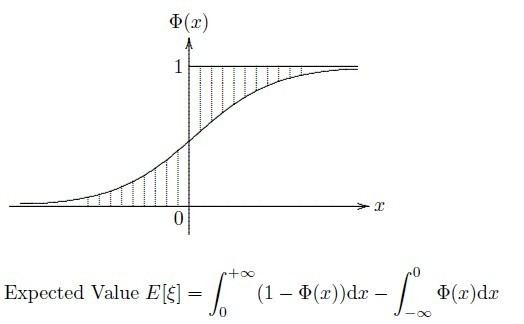

Expected Value

Definition: Let

provided that at least one of the two integrals is finite.

Theorem 1: Let

Theorem 2: Let

Theorem 3: Let

Variance

Definition: Let

Theorem: If

Critical value

Definition: Let

is called the α-optimistic value to

is called the α-pessimistic value to

Theorem 1: Let

Theorem 2: Let

Theorem 3: Suppose that

Entropy

Definition: Let

where

Theorem 1(Dai and Chen): Let

Theorem 2: Let

Theorem 3: Let

Inequalities

Theorem 1(Liu, Markov Inequality): Let

Theorem 2 (Liu, Chebyshev Inequality) Let

Theorem 3 (Liu, Holder’s Inequality) Let

Theorem 4:(Liu [127], Minkowski Inequality) Let

Convergence concept

Definition 1: Suppose that

for every

Definition 2: Suppose that

for every

Definition 3: Suppose that

Definition 4: Suppose that

Theorem 1: Convergence in Mean

Conditional uncertainty

Definition 1: Let

Theorem 1: Let

Definition 2: Let

Definition 3: The conditional uncertainty distribution

provided that

Theorem 2: Let

Theorem 3: Let

Definition 4: Let

provided that at least one of the two integrals is finite.