| ||

U.S. savings bonds are debt securities issued by the U.S. Department of the Treasury to help pay for the U.S. government’s borrowing needs. U.S. savings bonds are considered one of the safest investments because they are backed by the full faith and credit of the U.S. government.

Contents

Overview

History

On February 1, 1935, President Franklin D. Roosevelt signed legislation that allowed the U.S. Department of the Treasury to sell a new type of security, thus the savings bond was born. One month later, the first Series A savings bond proceeded to be issued with a face value of $25. At first, the main purpose was to help finance World War II, these were referred to as Defensive Bonds. On April 30, 1941 Roosevelt purchased the first bond from Treasury Secretary Henry Morgenthau, Jr.. The next day, they were made available to the public. After the attack on Pearl Harbor, Defensive Bonds were informally known as War Savings Bonds, citizens could buy the bonds for a dime. All the revenue coming in from the bonds went directly to support the war. Even after the war ended, savings bonds became popular with families. Unlike before, people started to just wait to cash them so the bonds would grow in value. To help sustain post-war sales, they were advertised on television, films, and commercials. When John F. Kennedy was president, he encouraged Americans to purchase them, which stimulated a large enrollment in savings bonds. By 1976, President Ford helped celebrate the 35th anniversary of the U.S. Savings Bond Program. The film, "An American Partnership" honored the role of citizens in financing the nation's growth. In 1990, Congress created the Education Savings Bond program which helped Americans finance a college education. A bond purchased on or after January 1, 1990, is tax-free (subject to income limitations) if used to pay tuition and fees at an eligible institution.

In 2002, the Department of the Treasury's Bureau of the Public Debt made savings bonds available for purchasing and redeeming online. Finally, on January 1, 2012 banks and other financial institutions terminated their sales of bonds. Currently, Americans can only buy U.S. savings bonds online at http://www.treasurydirect.gov/.

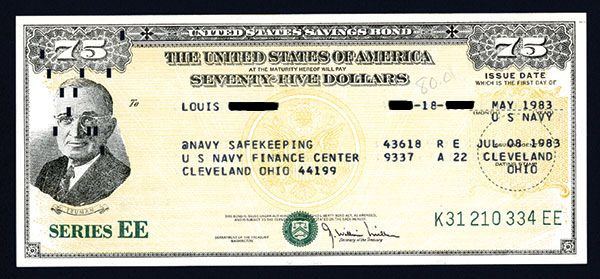

General information

Savings bonds come in eight denominations: $25, $50, $75, $100, $200, $500, $1,000, and $5,000. After purchase, the holder must wait at least six months before cashing it in, when they will receive the capital plus some interest. The maturity periods can vary. For example, if you buy a bond with a value of $50 for $25, you'll have to wait at least 17 years to get back your investment from the government, depending on the interest rate. The longer you wait, the greater interest you earn, however savings bonds have a 30-year maximum of interest accrual. After that the bond no longer accrues interest. Savings bonds are protected because they are secured by the U.S. government. The principal and earned interest are registered with the Treasury Department, so if a bond is lost, stolen, or destroyed they can be replaced at no cost. Savings bonds can also have value as a collectible since the government stopped issuing them in paper form.

Tax benefits of savings bonds

Savings bond interest is tax deferred. This means that you pay tax only when the bond is cashed (or stops earning interest after 30 years). Interest is taxable by the federal government but not state or local governments. Using the money from a cashed savings bond for higher education may keep you from paying federal income tax on your interest.

Current bond types

There are two types of savings bonds, EE-Bonds and I-Bonds.

Purchasing

Bonds require the purchaser to have a Treasury Direct account, which requires a social security number, a checking or savings account, and an email address. The purchaser can select the owner of the security, and the amount of the savings bond. After submitting an order, a message confirms the money will be taken out of the account within one day. A record of the savings bond purchase is placed in the purchaser's account, as paper bonds are no longer issued.

Bonds can be purchased as gifts. The social security number of the receiver need not be known at the time of purchase. A receiver must create a treasurydirect.gov account in order to receive the gift.

Converting paper savings bonds to electronic form

Paper savings bonds can be converted to electronic form. Advantages of converting to electronic form are: