| ||

Taxation in New Mexico takes several different forms. The principal taxes levied in the U.S. state of New Mexico include state income tax on personal and corporate income, a state gross receipts tax, gross receipts taxes in local jurisdictions, state and local property taxes, and several taxes related to production and processing of oil, gas, and other natural resources.

Contents

The New Mexico Taxation and Revenue Department is the state agency with primary responsibility for tax administration.

Income tax

New Mexico residents are subject to the state's personal income tax. Additionally, the personal income tax applies to nonresidents who work in the state or derive income from property there. Regular military salaries of New Mexico residents serving in the U.S. military are subject to the income tax, but since 2007, active-duty military salaries have been exempt from the state income tax.

Personal income tax rates for New Mexico range from 1.7% to 4.9%, within four income brackets. The individual income tax rates are listed in the table below.

Corporations that generate income from activities or sources in New Mexico and that are required to file federal income tax returns as corporations must pay corporate income tax to the state. Corporate income is taxed at the rate of 4.8% for the first $500,000, 6.4% for the next $500,000 (up to total income of $1 million), and 7.6% for income above the first million.

Gross receipts tax

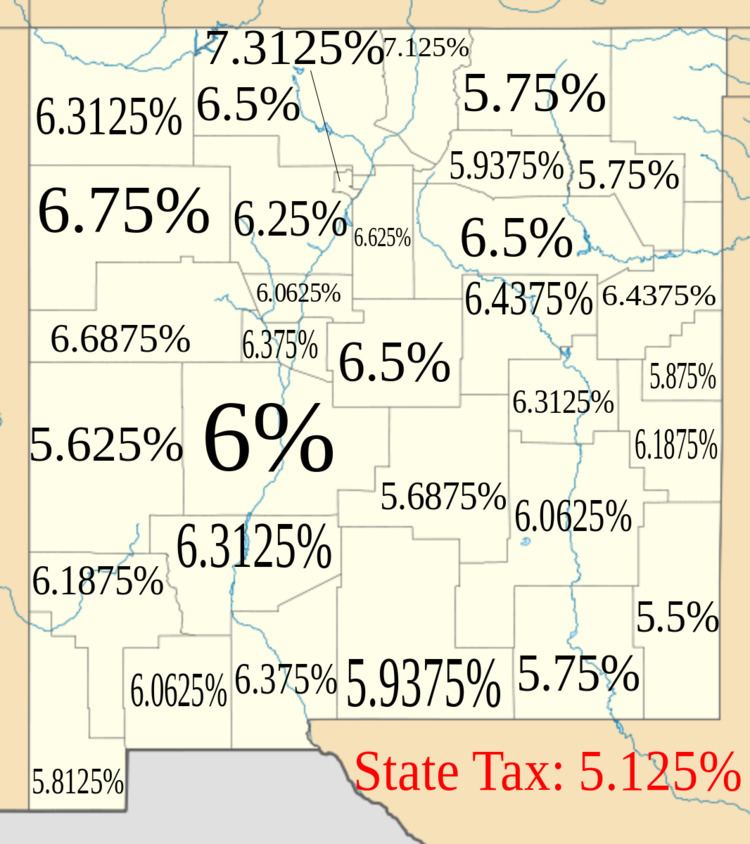

New Mexico does not have a state sales tax. However, the state imposes a gross receipts tax (GRT) on many business transactions. This resembles a sales tax, but unlike most states' sales taxes it applies to services, as well as tangible goods. Normally, the provider or seller passes the tax on to the purchaser, but legal incidence and burden apply to the business, as an excise tax.

At the state level, gross receipts on most types of transactions are taxed at a rate of 5.125%. Local jurisdictions also levy gross receipt taxes at rates that vary around the state. The lowest combined state and local GRT rate, as of 2012-13, is 5.5% in unincorporated Lea County. The highest combined rate is 8.6875%, in Taos Ski Valley. Albuquerque, the state's largest city, has a combined rate of 7.1875%.

The gross receipts of state and local governments other than school districts are taxed by the state at a rate of 5%. Governmental receipts typically subject to this tax include revenues from:

Property tax

Property tax is imposed on real property by the state, by counties, and by school districts. Personal-use personal property is not subject to property taxation, but property tax is levied on most business-use personal property. The taxable value of property is one-third of the assessed value. A tax rate of about 30 mills is applied to the taxable value, resulting in an effective tax rate of about 1%. In the 2005 tax year the average millage was about 26.47 for residential property and 29.80 for non-residential property. Assessed values of residences cannot be increased by more than 3% per year unless the residence is remodeled or sold. Property tax deductions are available for military veterans and heads of household.