| ||

Taxes in India are levied by the Central Government and the state governments. Some minor taxes are also levied by the local authorities such as the Municipality.

Contents

- History

- Constitutionally established scheme of taxation

- State governments

- Central Board of Direct Taxes

- Income Tax Department

- Central Board of Excise and Customs

- Organisational Structure

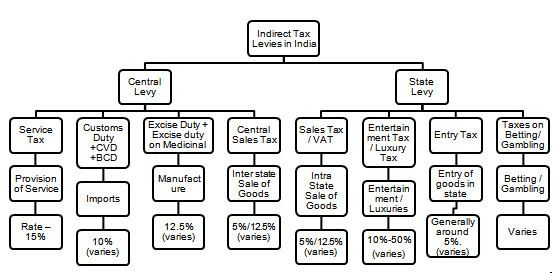

- Central Taxes

- Direct Taxes

- Income Tax

- Service tax

- Excise and Customs

- State Taxes

- Goods and Service Tax

- Local Body Taxes

- Property Tax

- References

The authority to levy a tax is derived from the Constitution of India which allocates the power to levy various taxes between the Central and the State. An important restriction on this power is Article 265 of the Constitution which states that "No tax shall be levied or collected except by the authority of law". Therefore, each tax levied or collected has to be backed by an accompanying law, passed either by the Parliament or the State Legislature. In 2015-2016, the gross tax collection of the Centre amounted to ₹14.60 trillion (US$220 billion).

History

India has abolished multiple taxes with passage of time and imposed new ones. Few of such taxes include interest tax, gift tax, wealth tax, etc. Wealth Tax Act, 1957 was repealed in the year 2015.

Constitutionally established scheme of taxation

Article 246 of the Indian Constitution, distributes legislative powers including taxation, between the Parliament of India and the State Legislature. Schedule VII enumerates these subject matters with the use of three lists:

Separate heads of taxation are no head of taxation in the Concurrent List (Union and the States have no concurrent power of taxation). The list of thirteen Union heads of taxation and the list of nineteen State heads are given below:

State governments

Any tax levied by the government which is not backed by law or is beyond the powers of the legislating authority may be struck down as unconstitutional.

The Central Board of Revenue or Department of Revenue is the apex body charged with the administration of taxes. It is a part of Ministry of Finance which came into existence as a result of the Central Board of Revenue Act, 1924.

Initially the Board was in charge of both direct and indirect taxes. However, when the administration of taxes became too unwieldy for one Board to handle, the Board was split up into two, namely the Central Board of Direct Taxes (CBDT) and Central Board of Excise and Customs (CBEC) with effect from 1 January 1964. This bifurcation was brought about by constitution of the two Boards under Section 3 of the Central Boards of Revenue Act, 1963.

Central Board of Direct Taxes

The Central Board of Direct Taxes (CBDT) provides essential inputs for policy and planning of direct taxes in India and is also responsible for administration of the direct tax laws through Income Tax Department. The CBDT is a statutory authority functioning under the Central Board of Revenue Act, 1963. It is India’s official FATF unit.

Organisational Structure

The CBDT is headed by CBDT Chairman and also comprises six members. The Chairperson holds the rank of Special Secretary to Government of India while the members rank of Additional Secretary to Government of India.

The CBDT Chairman and Members of CBDT are selected from Indian Revenue Service (IRS), a premier civil service of India, whose members constitute the top management of Income Tax Department.

Income Tax Department

Income Tax Department functions under the Department of Revenue in Ministry of Finance. It is responsible for administering following direct taxation acts passed by Parliament.

Income Tax Department is also responsible for enforcing Double Taxation Avoidance Agreements and deals with various aspects of international taxation such as Transfer Pricing. Finance Bill 2012 seeks to grant Income Tax Department powers to combat aggressive Tax avoidance by enforcing General Anti Avoidance Rules.

Central Board of Excise and Customs

Central Board of Excise and Customs (CBEC) is a part of the Department of Revenue under the Ministry of Finance, Government of India. It deals with the tasks of formulation of policy concerning levy and collection of Customs & Central Excise duties and Service Tax, prevention of smuggling and administration of matters relating to Customs, Central Excise, Service Tax and Narcotics to the extent under CBEC's purview. The Board is the administrative authority for its subordinate organizations, including Custom Houses, Central Excise and Service Tax Commissionerates and the Central Revenues Control Laboratory.

Organisational Structure

The CBEC is headed by CBEC Chairman and also comprises five members. The Chairperson holds the rank of Special Secretary to Government of India while the members rank of Additional Secretary to Government of India.

Central Taxes

In 2015-2016, the gross tax collection of the Centre amounted to ₹14.60 trillion (US$220 billion).

Direct Taxes

Direct Taxes in India were governed by two major legislations, Income Tax Act, 1961 and Wealth Tax Act, 1957. A new legislation, Direct Taxes Code (DTC), was proposed to replace the two acts. However, the Wealth Tax Act was repealed in 2015 and the idea of DTC was dropped.

As of 2015, Income Tax is the major source of direct tax in India.

Income Tax

The major tax enactment in India is the Income Tax Act, 1961 passed by the Parliament, which imposes a tax on the income of persons. This Act imposes a tax on income under the following five heads:

- Income from house property

- Income from business and profession

- Income from salaries

- Income in the form of capital gains

- Income from other sources

In terms of the Income Tax Act, 1961, a person includes

- Individual

- Hindu Undivided Family (HUF)

- Association of Persons (AOP)

- Body of Individuals (BOI)

- Company

- Firm

- Local authority

- Artificial Judicial person not falling in any of the preceding categories

The tax rate is prescribed every year by Parliament in the Finance Act, popularly called the Budget. In terms of the Finance Act, 2015, the rate of tax for individuals, HUF, Association of Persons (AOP) and Body of individuals (BOI) is as under;

Service tax

It is a tax levied on services provided in India, except the State of Jammu and Kashmir. The responsibility of collecting the tax lies with the Central Board of Excise and Customs(CBEC). From 2012, service tax is imposed on all services, except those which are specifically exempted under law(e.g. Exempt under Negative List, Exempt as exclusion from Service definition as per Service Tax, Exempt under MEN(Mega exemption notification)). In budget presented for 2008-2009, it was announced that all small service providers whose turnover does not exceed ₹10 lakh (US$15,000) need not pay service tax. Service tax at a rate of 14 percent(Inclusive of EC & SHEC) will be imposed on all applicable services from 1 June 2015. From 15th November 2015, Swacch Bharat cess of 0.5% has been added to all taxable service leading the new Service Tax rate to be 14.5 percent (Inclusive of EC, SHEC & Swacch Bharat cess). On 29 February 2016, Current Finance Minister Mr. Arun Jaitley announces a new Cess, Krishi Kalyan Cess that would be levied from the 1st June 2016 at the rate of 0.5% on all taxable services. The purpose of introducing Krishi Kalyan Cess is to improve agriculture activities and welfare of Indian farmers. Thus, the new Service Tax rate would be 15% incorporating EC, SHEC, Swachh Bharat Cess and Krishi Kalyan Cess.

From 2015 to currently, the gross tax collection of the Centre from service tax has amounted in excess of ₹2.10 trillion (US$31 billion).

Excise and Customs

In 2015-2016, the gross tax collection of the Centre from excise amounted to ₹2.80 trillion (US$42 billion).

- Central Excise Act, 1944, which imposes a duty of excise on goods manufactured or produced in India;

- Customs Act, 1962, which imposes duties of customs, countervailing duties, and anti-dumping duties on goods imported in India;

- Central Sales Tax, 1956, which imposes sales tax on goods sold in inter-state trade or commerce in Indisale of property situated within the state

State Taxes

Value Added Tax (VAT) is a major source of revenue for Indian States. Other state level taxes include Entertainment tax, Entry Tax and Octroi.

Goods and Service Tax

The ex-Finance Minister of India, P.Chidambaram in his Budget speech has indicated the government's intent of merging all taxes like Service Tax, Excise and VAT into a common Goods and Service Tax by the year 2011. To achieve this objective, the rate of Central Excise and Service Tax will be progressively altered and brought to a common rate.. As of October 2015, Goods and Services Tax Bill has been passed by the Parliament and ratified by the states. The GST council is in deliberation with concerned authorities to arrive at an agreed rate of interest.

The Rajya Sabha passed the Constitutional Amendment Bill required for introduction of GST bills on 3 August 2016 with more than two-third majority.

The IT framework and services for implementation of the new taxation system will be managed by "Goods and Services Tax Network (GSTN)", a non-government company set up by the Centre and states.

Local Body Taxes

"Local Body Tax", popularly known by its abbreviation as "LBT", is the tax imposed by the local civic bodies of India on the entry of goods into a local area for consumption, use or sale therein. The tax is imposed based on the Entry 52 of the State List from the Schedule VII of the Constitution of India which reads; "Taxes on the entry of goods into a local area for consumption, use or sale therein." The tax is to be paid by the trader to the civic bodies and the rules and regulations of these vary amongst different States in India. The LBT is now partially abolished as of August 1, 2015.

Property Tax

Property tax or 'house tax' is a local tax on buildings, along with appurtenant land, and imposed on Possessor (certainly, not true custodian of property as per 1978, 44th amendment of constitution). It resembles the US-type wealth tax and differs from the excise-type UK rate. The tax power is vested in the states and it is delegated by law to the local bodies, specifying the valuation method, rate band, and collection procedures. The tax base is the annual rental value (ARV) or area-based rating. Owner-occupied and other properties not producing rent are assessed on cost and then converted into ARV by applying a percentage of cost, usually six percent. Vacant land is generally exempt. Central government properties are exempt. Instead a 'service charge' is permissible under executive order. Properties of foreign missions also enjoy tax exemption without an insistence for reciprocity. The tax is usually accompanied by a number of service taxes, e.g., water tax, drainage tax, conservancy (sanitation) tax, lighting tax, all using the same tax base. The rate structure is flat on rural (panchayat) properties, but in the urban (municipal) areas it is mildly progressive with about 80% of assessments falling in the first two slabs.