| ||

Taxes provide the most important revenue source for the Government of the People's Republic of China. As the most important source of fiscal revenue, tax is a key component of macro-economic policy, and greatly affects China's economic and social development. With the changes made since the 1994 tax reform, China has preliminarily set up a streamlined tax system geared to the socialist market economy.

Contents

- Types of taxes

- Tax legislation

- Current Tax Legislation Table

- Foreign investment taxation

- Urban and Township Land Use Tax

- City Maintenance and Construction Tax

- Fixed Assets Investment Orientation Regulation Tax

- Land Appreciation Tax

- Urban Real Estate Tax

- Vehicle and Vessel Usage License Plate Tax

- Individual income tax

- Tax governance

- Revenue statistics

- Revenue breakdown in 1997

- References

China's tax revenue came to 11.05 trillion yuan (1.8 trillion U.S. dollars) in 2013, up 9.8 percent on 2012. The 2017 the World Bank “Doing Business” rankings estimated that China’s total tax rate for corporations was 68% a percentage of profits through direct and indirect tax. As a percentage of GDP, according to the State Administration of Taxation, overall tax revenues were 30% in China.

The government agency in charge of tax policy is the Ministry of Finance. For tax collection, State Administration of Taxation.

As part of US$586 billion economic stimulus package of November 2008, the government planned to reform the VAT, stating the plan could cut corporation taxes by 120 billion yuan.

Types of taxes

Under the current tax system in China, there are 26 types of taxes, which, according to their nature and function, can be divided into the following 8 categories:

Tax legislation

State organs that have the authority to formulate tax laws or tax policy include the National People's Congress and its Standing Committee, the State Council, the Ministry of Finance, the State Administration of Taxation, the Tariff and Classification Committee of the State Council, and the General Administration of Customs.

Tax laws are enacted by the National People's Congress, e.g., the Individual Income Tax Law of the People's Republic of China; or enacted by the Standing Committee of the National People's Congress, e.g., the Tax Collection and Administration Law of the People's Republic of China.

The administrative regulations and rules concerning taxation are formulated by the State Council, e.g., the Detailed Rules for the Implementation of the Tax Collection and Administration Law of the People' s Republic of China, the Detailed Regulations for the Implementation of the Individual Income Tax Law of the People's Republic of China, the Provisional Regulations of the People's Republic of China on Value Added Tax.

The departmental rules concerning taxation are formulated by the Ministry of Finance, the State Administration of Taxation, the Tariff and Classification Committee of the State Council, and the General Administration of Customs, e.g., the Detailed Rules for the Implementation of the Provisional Regulations of the People's Republic of China on Value Added Tax, the Provisional Measures for Voluntary Reporting of the Individual Income Tax.

The formulation of tax laws follow four steps: drafting, examination, voting and promulgation. The four steps for the formulation of tax administrative regulations and rules are: planning, drafting, verification and promulgation. The four steps mentioned above take place in accordance with laws, regulations and rules.

Besides, the laws of China stipulates that within the framework of the national tax laws and regulations, some local tax regulations and rules may be formulated by the People's Congress at the provincial level and its Standing Committee, the People's Congress of minority nationality autonomous prefectures and the People's Government at provincial level.

The following table summarises up the current tax laws, regulations and rules and relevant legislation in China.

Current Tax Legislation Table

Note: The provisions of criminal responsibilities in Supplementary Rules of the Standing Committee of NPC of the People's Republic of China on Penalizing Tax Evasions and Refusal to Pay Taxes and Resolutions of the Standing Committee of NPC of the People's Republic of China on Penalizing Any False Issuance, Forgery and/or Illegal Sales of VAT Invoices have been integrated into the Criminal Law of the People's Republic of China revised and promulgated on 14 March 1997.

Foreign investment taxation

There are 14 kinds of taxes currently applicable to the enterprises with foreign investment, foreign enterprises and/or foreigners, namely: Value Added Tax, Consumption Tax, Business Tax, Income Tax on Enterprises with Foreign Investment and Foreign Enterprises, Individual Income Tax, Resource Tax, Land Appreciation Tax, Urban Real Estate Tax, Vehicle and Vessel Usage License Plate Tax, Stamp Tax, Deed Tax, Slaughter Tax, Agriculture Tax, and Customs Duties.

Hong Kong, Macau and Taiwan and overseas Chinese and the enterprises with their investment are taxed in reference to the taxation on foreigners, enterprises with foreign investment and/or foreign enterprises. In an effort to encourage inward flow of funds, technology and information, China provides numerous preferential treatments in foreign taxation, and has successively concluded tax treaties with 60 countries (by July 1999): Japan, the USA, France, UK, Belgium, Germany, Malaysia, Norway, Denmark, Singapore, Finland, Canada, Sweden, New Zealand, Thailand, Italy, the Netherlands, Poland, Australia, Bulgaria, Pakistan, Kuwait, Switzerland, Cyprus, Spain, Romania, Austria, Brazil, Mongolia, Hungary, Malta, the UAE, Luxembourg, South Korea, Russia, Papua New Guinea, India, Mauritius, Croatia, Belarus, Slovenia, Israel, Vietnam, Turkey, Ukraine, Armenia, Jamaica, Iceland, Lithuania, Latvia, Uzbekistan, Bangladesh, Yugoslavia, Sudan, Macedonia, Egypt, Portugal, Estonia, and Laos, 51 of which have been in force.

Urban and Township Land Use Tax

(1) Taxpayers

The taxpayers of Urban and Township Land Use Tax include all enterprises, units, individual household businesses and other individuals (excluding enterprises with foreign investment, foreign enterprises and foreigners).

(2) Tax payable per unit

The tax payable per unit is differentiated with different ranges for different regions, i.e., the annual amount of tax payable per square meter is: 0.5-10 yuan for large cities, 0.4-8 yuan for medium-size cities, 0.3-6 yuan for small cities, or 0.2-4 yuan for mining districts. Upon approval, the tax payable per unit for poor area may be lowered or that for developed area may be raised to some extent.

(3) Computation

The amount of tax payable is computed on the basis of the actual size of the land occupied by the taxpayers and by applying the specified applicable tax payable per unit. The formula is:

Tax payable = Size of land occupied ×Tax payable per unit

(4) Major exemptions

Tax exemptions may be given on land occupied by governmental organs, people's organizations and military units for their own use; land occupied by units for their own use which are financed by the institutional allocation of funds from financial departments of the State; land occupied by religious temples, parks and historic scenic spots for their own use; land for public use occupied by Municipal Administration, squares and green land; land directly utilized for production in the fields of agriculture, forestry, animal husbandry and fishery industries; land used for water reservation and protection; and land occupied for energy and transportation development upon approval of the State.

City Maintenance and Construction Tax

(1) Taxpayers

The enterprises of any nature, units, individual household businesses and other individuals (excluding enterprises with foreign investment, foreign enterprises and foreigners) who are obliged to pay Value Added Tax, consumption Tax and/or Business Tax are the taxpayers of City Maintenance and Construction Tax.

(2) Tax rates and computation of tax payable

Differential rates are adopted: 7% rate for city area, 5% rate for county and township area and 1% rate for other area. The tax is based on the actual amount of VAT, Consumption Tax and/or Business Tax paid by the taxpayers, and paid together with the three taxes mentioned above. The formula for calculating the amount of the tax payable:

Tax payable = Tax base × tax rate Applicable

Fixed Assets Investment Orientation Regulation Tax

(1) Taxpayers

This tax is imposed on enterprises, units, individual household businesses and other individuals who invest into fixed assets within the territory of the People's Republic of China (excluding enterprises with foreign investment, foreign enterprises and foreigners).

(2) Taxable items and tax rates

Table of Taxable Items and Tax Rates:

(* For some residential building investment projects, the rate is 5%.)

(3) Computation of tax payable

This tax is based on the total investment actually put into fixed assets. For renewal and transformation projects, the tax is imposed on the investment of the completed part of the construction project. The formula for calculating the tax payable is:

Tax payable - Amount of investment completed or amount of investment in construction project × Applicable rate

Land Appreciation Tax

(3) Computation of tax payable

To calculate the amount of Land Appreciation Tax payable, the first step is to arrive at the appreciation amount derived by the taxpayer from the transfer of real estate, which equals to the balance of proceeds received by the taxpayer on the transfer of real estate after deducting the sum of relevant deductible items. Then the amount of tax payable shall be calculated respectively for different parts of the appreciation by applying the applicable tax rates in line with the percentages of the appreciation amount over the sum of the deductible items. The sum of the amount of tax payable for different parts of the appreciation shall be the full amount of tax payable by the taxpayers. The formula is:

Tax payable = Σ (Part of appreciation ×Applicable rate)

(4) Major exemptions

The Land Appreciation Tax shall be exempt in situations where the appreciation amount on the sale of ordinary standard residential buildings construction by taxpayers for sale does not exceed 20% of the sum of deductible items and when the real estate is taken over or repossessed in accordance to the laws due to the construction requirements of the State.

Urban Real Estate Tax

(1) Taxpayers

At present, this tax is only applied to enterprises with foreign investment, foreign enterprises and foreigners, and levied on house property only.

Taxpayers are owners, mortgagees custodians and/or users of house property.

(2) Tax base, tax rates and computation of tax payable

Two different rates are applied to two different bases: one rate of 1. 2% is applied to the value of house property, and the other rate of 18% is applied to the rental income from the property. The formula for calculating House Property Tax payable is:

Tax payable = Tax base ×Applicable rate

(3) Major exemptions and reductions

Newly constructed buildings shall be exempt from the tax for three years commencing from the month in which the construction is completed. Renovated buildings for which the renovation expenses exceed one half of the expenses of the new construction of such buildings shall be exempt from the tax for two years commencing from the month in which the renovation is completed. Other house property may be granted tax exemption or reduction for special reasons by the People's Government at provincial level or above.

Vehicle and Vessel Usage License Plate Tax

(1) Taxpayers

At this moment, this tax is only applied to the enterprises with foreign investment, foreign enterprises, and foreigners. The users of the taxable vehicles and vessels are taxpayers of this tax.

(2) Tax amount per unit

The tax amount per unit is different for vehicles and vessels:

a. Tax amount per unit for vehicles: 15-80 yuan per passenger vehicle per quarter; 4-15 yuan per net tonnage per quarter for cargo vehicles; 5-20 yuan per motorcycle per quarter. 0.3-8 yuan per non-motored vehicle per quarter.

b. Tax amount per unit for vessels: 0.3- 1.1 yuan per net tonnage per quarter for motorized vessels; 0.15-0.35 yuan per non-motorized vessel.

(3) Computation

The tax base for vehicles is the quantity or the net tonnage of taxable vehicles The tax base for vessels is the net-tonnage or the deadweight tonnage of the taxable vessels. The formula for computing the tax payable is:

a. Tax payable = Quantity (or net-tonnage ) of taxable vehicles × Applicable tax amount per unit b. Tax payable = Net-tonnage (or deadweight tonnage) of taxable vessels × Applicable tax amount per unit

(4) Exemptions

a. Tax exemptions may be given on the vehicles used by Embassies and Consulates in China; the vehicles used by diplomatic representatives, consuls, administrative and technical staffs and their spouses and non-grown-up children living together with them.

b. Tax exemptions may be given as stipulated in some provinces and municipalities on the fire vehicles, ambulances, water sprinkling vehicles and similar vehicles of enterprises with foreign investment and foreign enterprises.

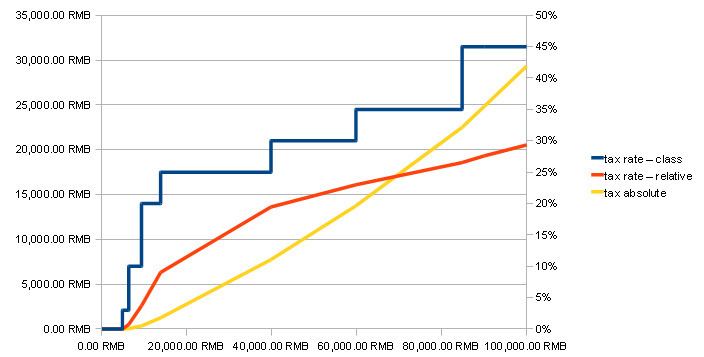

Individual income tax

tax exemption: 3500 for regular employees, 4800 RMB non residents

monthly tax = (taxable income - tax exemption) * tax rate - quick deduction

Tax governance

As of 2007, a paper reported that about two-thirds of tax revenue was spent at the local level and that "the ratio of central revenue to total tax revenues reached a low of 22 per cent in 1993, before rising to the 50 per cent level following the 1994 tax reform".

Revenue statistics

The table details China's revenue statistics from 1952 to 1997.

Note: For three years, the tax revenue exceeded the fiscal revenue due to the excessive amount of losses by enterprises that largely reduced the fiscal revenue.

Revenue breakdown in 1997

Revenue breakdown by Type of Taxes in 1997: