| ||

In econometrics, a structural break is an unexpected shift in a (macroeconomic) time series. This can lead to huge forecasting errors and unreliability of the model in general. This issue was popularised by David Hendry.

Contents

Test

In general, the CUSUM (cumulative sum) and CUSUM-sq (CUSUM squared) tests can be used to test the constancy of the coefficients in a model. The bounds test can also be used.

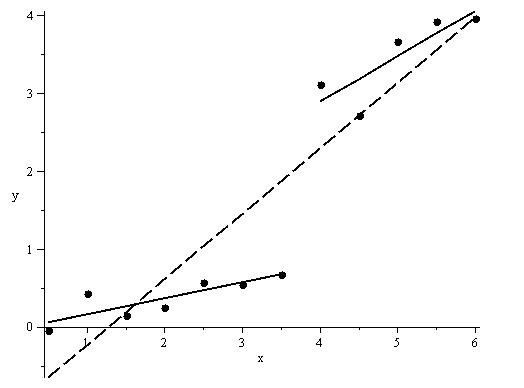

For a linear model with one known single break in mean, the Chow test is often used. If the single break in mean is unknown, then Hartley's test may be appropriate. Other challenges are where there are:

Case 1: a known number of unknown breaks in mean; Case 2: an unknown number of (unknown) breaks in mean; Case 3: breaks in variance.The Chow test is not applicable for these situations; however, for cases 1 and 2, the sup-Wald, sup-LM, and sup-LR tests developed by Andrews (1993, 2003) may be used to test for parameter instability when the change points (the structural break locations) are unknown.

For nonstationary process, there are many more challenges. For a cointegration model, the Gregory–Hansen test (1996) is used for one unknown structural break, and the Hatemi-J test (2006) is used for two unknown breaks.

There are several programs that can be used to find structural breaks, including R and GAUSS.

More sophisticated model

The latest method has been used by Bai and Perron (2003) in which multiple structural breaks can be automatically detected from data. The literature in this regard is very vast starting right from 1987 to 2010. Recently economists are going for both growth rate analysis and also econometric analysis in order to find break points.