| ||

In finance, the rule of 72, the rule of 70 and the rule of 69.3 are methods for estimating an investment's doubling time. The rule number (e.g., 72) is divided by the interest percentage per period to obtain the approximate number of periods (usually years) required for doubling. Although scientific calculators and spreadsheet programs have functions to find the accurate doubling time, the rules are useful for mental calculations and when only a basic calculator is available.

Contents

- Using the rule to estimate compounding periods

- Choice of rule

- History

- Adjustments for higher accuracy

- E M rule

- Periodic compounding

- Continuous compounding

- References

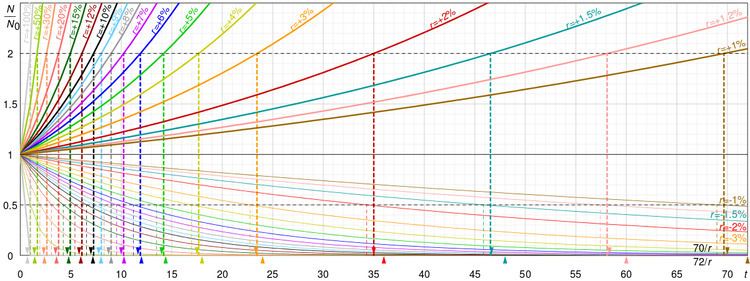

These rules apply to exponential growth and are therefore used for compound interest as opposed to simple interest calculations. They can also be used for decay to obtain a halving time. The choice of number is mostly a matter of preference: 69 is more accurate for continuous compounding, while 72 works well in common interest situations and is more easily divisible. There are a number of variations to the rules that improve accuracy. For periodic compounding, the exact doubling time for an interest rate of r per period is

where T is the number of periods required. The formula above can be used for more than calculating the doubling time. If one wants to know the tripling time, for example, simply replace the constant 2 in the numerator with 3. As another example, if one wants to know the number of periods it takes for the initial value to rise by 50%, replace the constant 2 with 1.5.

Using the rule to estimate compounding periods

To estimate the number of periods required to double an original investment, divide the most convenient "rule-quantity" by the expected growth rate, expressed as a percentage.

Similarly, to determine the time it takes for the value of money to halve at a given rate, divide the rule quantity by that rate.

Choice of rule

The value 72 is a convenient choice of numerator, since it has many small divisors: 1, 2, 3, 4, 6, 8, 9, and 12. It provides a good approximation for annual compounding, and for compounding at typical rates (from 6% to 10%). The approximations are less accurate at higher interest rates.

For continuous compounding, 69 gives accurate results for any rate. This is because ln(2) is about 69.3%; see derivation below. Since daily compounding is close enough to continuous compounding, for most purposes 69, 69.3 or 70 are better than 72 for daily compounding. For lower annual rates than those above, 69.3 would also be more accurate than 72.

History

An early reference to the rule is in the Summa de arithmetica (Venice, 1494. Fol. 181, n. 44) of Luca Pacioli (1445–1514). He presents the rule in a discussion regarding the estimation of the doubling time of an investment, but does not derive or explain the rule, and it is thus assumed that the rule predates Pacioli by some time.

Roughly translated:

Adjustments for higher accuracy

For higher rates, a bigger numerator would be better (e.g., for 20%, using 76 to get 3.8 years would be only about 0.002 off, where using 72 to get 3.6 would be about 0.2 off). This is because, as above, the rule of 72 is only an approximation that is accurate for interest rates from 6% to 10%. For every three percentage points away from 8% the value 72 could be adjusted by 1.

or for the same result, but simpler:

E-M rule

The Eckart–McHale second-order rule (the E-M rule) provides a multiplicative correction for the rule of 69.3 that is very accurate for rates from 0% to 20%. The rule of 69.3 is normally only accurate at the lowest end of interest rates, from 0% to about 5%. To compute the E-M approximation, simply multiply the rule of 69.3 result by 200/(200−r) as follows:

For example, if the interest rate is 18%, the rule of 69.3 says t = 3.85 years. The E-M rule multiplies this by 200/(200−18), giving a doubling time of 4.23 years, where the actual doubling time at this rate is 4.19 years. (The E-M rule thus gives a closer approximation than the rule of 72.)

Note that the numerator here is simply 69.3 times 200. As long as the product stays constant, the factors can be modified arbitrarily. The E-M rule could thus be written also as

in order to keep the product mostly unchanged. In these variants, the multiplicative correction becomes 1 respectively for r=2 and r=8, the values for which the rule of 70 (respectively 72) is most precise.

Similarly, the third-order Padé approximant gives a more accurate answer over an even larger range of r, but it has a slightly more complicated formula:

Periodic compounding

For periodic compounding, future value is given by:

where

The future value is double the present value when the following condition is met:

This equation is easily solved for

If r is small, then ln(1 + r) approximately equals r (this is the first term in the Taylor series). Together with the approximation

which improves in accuracy as the compounding of interest becomes continuous (see derivation below).

However, humans tend to prefer performing mental calculations with percentages, so the formula is often restated as follows:

In order to derive the more precise adjustments presented above, it is noted that

Replacing the "R" in R/200 on the third line with 7.79 gives 72 on the numerator. This shows that the rule of 72 is most precise for periodically composed interests around 8%.

Alternatively, the E-M rule is obtained if the second-order Taylor approximation is used directly.

Continuous compounding

For continuous compounding, the derivation is simpler and yields a more accurate rule: