| ||

In actuarial science and applied probability ruin theory (sometimes risk theory collective risk theory) uses mathematical models to describe an insurer's vulnerability to insolvency/ruin. In such models key quantities of interest are the probability of ruin, distribution of surplus immediately prior to ruin and deficit at time of ruin.

Contents

Classical model

The theoretical foundation of ruin theory, known as the Cramér–Lundberg model (or classical compound-Poisson risk model, classical risk process or Poisson risk process) was introduced in 1903 by the Swedish actuary Filip Lundberg. Lundberg's work was republished in the 1930s by Harald Cramér.

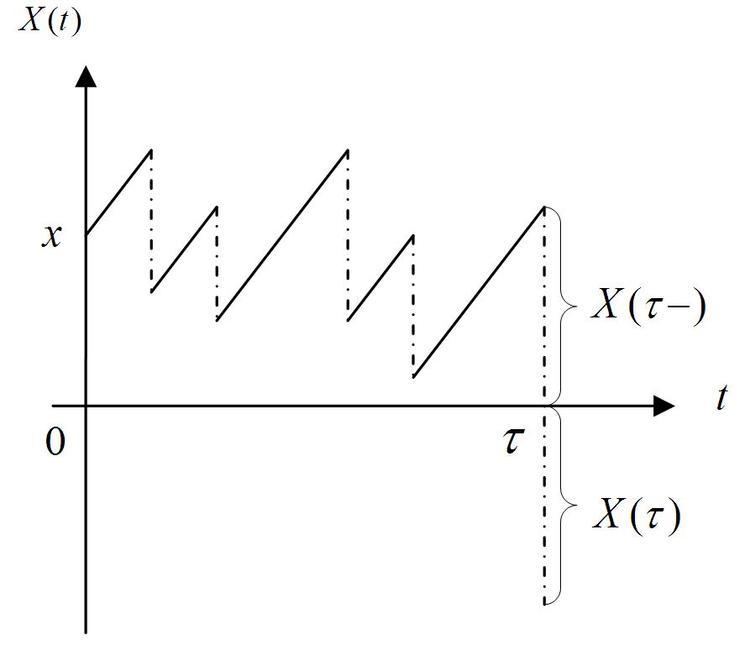

The model describes an insurance company who experiences two opposing cash flows: incoming cash premiums and outgoing claims. Premiums arrive a constant rate c > 0 from customers and claims arrive according to a Poisson process with intensity λ and are independent and identically distributed non-negative random variables with distribution F and mean μ (they form a compound Poisson process). So for an insurer who starts with initial surplus x,

The central object of the model is to investigate the probability that the insurer's surplus level eventually falls below zero (making the firm bankrupt). This quantity, called the probability of ultimate ruin, is defined as

where the time of ruin is

where

In the case where the claim sizes are exponentially distributed, this simplifies to

Sparre Andersen model

E. Sparre Andersen extended the classical model in 1957 by allowing claim inter-arrival times to have arbitrary distribution functions.

where the claim number process

Expected discounted penalty function

Michael R. Powers and Gerber and Shiu analyzed the behavior of the insurer's surplus through the expected discounted penalty function, which is commonly referred to as Gerber-Shiu function in the ruin literature. It is arguable whether the function should have been called Powers-Gerber-Shiu function due to the contribution of Powers.

In Powers’ notation, this is defined as

where

In Gerber and Shiu’s notation, it is given as

where

It is quite intuitive to interpret the expected discounted penalty function. Since the function measures the actuarial present value of the penalty that occurs at

There are a great variety of ruin-related quantities that fall into the category of the expected discounted penalty function.

Other finance-related quantities belonging to the class of the expected discounted penalty function include the perpetual American put option, the contingent claim at optimal exercise time, and more.