| ||

Revenue assurance (RA) is a niche business activity most commonly undertaken within businesses that provide telecommunication services. The activity is the use of data quality and process improvement methods that improve profits, revenues and cash flows without influencing demand. This was defined by a TM Forum working group based on research documented in its Revenue Assurance Technical Overview [1]. In many telecommunications service providers, revenue assurance is led by a dedicated revenue assurance department.

Contents

- Overview

- The value of revenue assurance

- Revenue Assurance in Telecom

- What causes the problem

- Where is the problem

- Revenue assurance discipline

- Maturity of Revenue Assurance

- RA Process Categories

- Detective Processes

- Corrective Processes

- Preventive Processes

- Tool for Revenue Assurance

- Extract Transform and Load

- Reconciliations

- Analysis and KPIs

- Dash boarding

- Case Management

- References

Overview

"Revenue assurance" is a broad umbrella term. It is used both to describe an activity performed within telecommunications service providers, and is a common name for a small business unit associated with that activity. Revenue assurance is a practical response to perceived or actual issues with operational under performance, most commonly relating to billing and collection of revenue. Some of the procedures associated with identifying, remedying or preventing errors may be undertaken by a dedicated Revenue Assurance department, though responsibility for revenue assurance is often diffuse and varies greatly with the organizational structure of the provider. Assuming a provider with a typical organizational split, responsibilities for revenue assurance primarily sit between the Finance and Technology directorates, however, revenue assurance initiatives are often started in a business unit or marketing group.

The relevance to Finance rests with the responsibility for financial control, audit and reporting, while the subject matter would be network and IS systems as implemented or operated by the Technology side of the business. Marketing groups and / or business units (e.g. wholesale or retail business lines) will often embark on revenue assurance projects in an effort to improve product line margins. Furthermore, marketing and business units are pivotal in providing input into the "should be" state of customer bills and products.

The sphere of influence described by revenue assurance varies greatly between telecommunications service providers, but is usually closely related to back office functions where small errors may have a disproportionately large impact on revenues or costs. The processing of transaction data in modern telecommunications providers exhibits many attributes akin to a complex system. However, there is significant disagreement about the ultimate aims and legitimate scope of revenue assurance teams. This is in part caused by:

(1) the cross-functional nature of the activity and the consequent need for a variety of skills from IT, marketing, finance, et al.;

(2) the difficulty of generalizing across businesses with different objectives and business models;

(3) political infighting within each telco about responsibility for revenue leakages and assurance; and

(4) the difficulty in reliably measuring the value added by revenue assurance as separable from underlying performance.

There is high-level agreement between practitioners about the goals and methods of revenue assurance, though reaching a consensus on defining the boundaries of revenue assurance has proved elusive so far. The goals relate to improving the financial performance by eliminating mistakes in the processing of transaction data. Some take a more encompassing view of what counts as a mistake, which may extend as far as questioning the policy set by executives even when this has been executed correctly. Others take a more open-ended view of the data that is the subject matter. For example, in decreasing order of frequency, revenue assurance may cover:

(1) revenues from retail and corporate sales;

(2) revenues and costs from interconnect and wholesale contracts; and

(3) margins and profitability of investment in networks and information systems.

Other markets have different or more refined priorities. For example, in the U.S.A. management of wholesale contracts has often been the first objective because of the complexity of the domestic market resulting from the Federal Communications Commission's regulatory framework. In contrast, telcos in developing countries may prioritize management of international interconnect arrangements because of the risks posed by fraud and arbitrage. A cable supplier or internet service provider that predominantly offers retail customers flat monthly charges and no limits on usage may be most interested in assuring the profitability of network investments.

Revenue assurance is often regarded by practitioners as a low-cost mechanism to generate significant financial returns for telecommunications service providers. However, the returns are unpredictable as well as being hard to measure, which encourages many executives to take a sceptical view of its worth. Comparable revenue assurance activities do occur in other industries, such as with billing of utilities or with the licensing of software, and there are many parallels with financial and operational control activities undertaken by most large businesses. The rationale for why revenue assurance has come to be considered particularly important in telecommunications, unlike other industries, is disputed. Reasonable conjectures are that:

(1) the fast pace of change and intense commercial competition increase the likelihood of mistakes;

(2) there is significant complexity in determining the combined effect of interacting systems and processes; and

(3) the high-volume, low-value nature of transactions amplifies the financial implications of "small" errors.

Another conjecture is that revenue assurance is a response to changing market conditions. The thinking is that as markets reach saturation and growth potential falls off, so the value of maximizing returns from existing sales increases. This observation has some merit but does not explain the increasing popularity of revenue assurance in telcos serving growth markets. It also in part contradicts the assumption of a compelling costs versus benefits argument for revenue assurance, which would be enhanced in businesses undergoing rapid change. It is also important to recognize that there is a long history of revenue assurance activities in some telcos that predates the coining of the term "revenue assurance".

The revenue assurance techniques applied in practice cover a broad spectrum, from analysis and implementation of business controls to automated data interrogation. At one end of the spectrum, revenue assurance can appear very similar to the kinds of review and process mapping techniques applied for other financial controlling objectives like accounting integrity, as exemplified by those derived from clause 404 of the Sarbanes-Oxley Act. This form of revenue assurance is most commonly promoted by consultancies. The size of such consultancies covers the entire range; the Big 4 all offer some form of revenue assurance consulting, but there are also niche specialist consultancies. At the other end of the spectrum, revenue assurance is treated as a form of reactive automated data interrogation, seeking to find anomalies in transaction data that may indicate errors and potential revenue loss. This form of revenue assurance is most commonly promoted by software houses that aim to provide databases and configurable tools to extract and interrogate a telco's source data. A less popular form of reactive automated assurance involves using both software and specialised hardware as a means of extracting additional data on transactions, for example by creating actual network events or interfacing directly with network elements to replicate dummy events. As with consultancies, IT-oriented revenue assurance solutions are offered by both large vendors like providers of billing and mediation software, and by specialized niche providers.

There is some debate about the relative merits of the different techniques that can be employed in revenue assurance.

As yet, there is no professional body, no qualifications, and no academic research that would help to drive consensus about the purpose or methods of revenue assurance. In part this is addressed by individuals working in the sector through membership and qualification in related fields such as accountancy and information systems audit. Some scientific research in other fields is also applicable to revenue assurance, though most revenue assurance "facts" rely heavily on anecdotes and oft-repeated truisms. Some of the most helpful and progressive initiatives in addressing the problem of consensus and scientific basis are listed below.

The value of revenue assurance

Revenue assurance is usually understood as a means to identify and remedy, and perhaps also to prevent, problems that result in financial under performance without seeking to generate additional sales. The most common metaphor is that of leaking water from a pipe, where water stands in place of revenues or cash flows, and the leaks represent waste. The value of revenue assurance is hence determined by the size of the leaks "plugged", and possibly also those leaks prevented before they occur, although estimating the value of the latter is very problematic. The value added also includes the recovery of "lost" revenues or costs (through issuing additional bills, chasing uncollected payments, renegotiating with suppliers a refund of costs etc.) after the fact. This last form of reactive revenue assurance is the easiest to put a value to, but is in many ways the least efficient form of revenue assurance; effort is directed towards repeatedly addressing the consequences of known flaws, and not on addressing the flaws themselves. This can lead to a parasitical relationship between a Revenue Assurance department or vendor and the wider business, where the department/vendor finds it easiest to justify its ongoing existence/contract by repeatedly fixing symptoms and not the root causes.

The TM Forum conducted a benchmark survey in 2008 that concluded average leakage, not including losses due to fraud, was 1% of the gross revenues for those telcos that took part. The number of participating telcos was relatively small compared to some other surveys, but the survey technique was more demanding than any comparable survey to date. The survey used the most detailed and prescriptive definition of how to calculate leakage of any survey of its type. The definition was taken from the TM Forum's own standard on how to calculate revenue assurance metrics [2]. To increase confidence that participants calculated their leakages correctly, the TM Forum's benchmark program independently reviewed the results and corroborated them with representatives of the participating companies. The survey's average of 1% leakage of gross revenue, whilst still significant, is notably lower than many other quoted estimates and reported survey findings about average leakage. This may be because the survey used a very strict definition of leakage. The survey measured only actual under-billed and unbilled amounts discovered by the participants; it excluded other types of leakages such as cost leakages and loss of opportunity leakages, and it excluded projected leakage estimations that are commonly used (i.e., what would have been the amount of leakage, if the leakage would not been discovered by revenue assurance activities). It may also reflect a reduction in bias or exaggeration in reported leakages, or at least the exclusion of guesswork. Respondents were given authoritative instructions on how to quantify leakage based on actual data and were instructed to avoid making suppositions in the absence of such data.

The best known estimates of "typical" revenue leakage come from a series of annual surveys conducted by the Analysys consultancy and research business. In these surveys, leakage was commonly estimated as being worth between 5% and 15% of the total revenue of the business. Similar research by other businesses has generated results in the same range, with none concluding leakage of less than 1% of gross revenue, and some suggesting leakage of 20% or more was not uncommon. Reasons to doubt these estimates are as follows:

(1) All the estimates of leakage were derived from the subjective opinions of staff working in service providers;

(2) All the research was conducted by businesses wishing to promote their revenue assurance products;

(3) Increased annual spend on revenue assurance has not resulted in a clear downward trend in estimates;

(4) The estimates were broadly similar even when the criteria for what losses to include varied greatly; and

(5) Genuine losses of this scale should be a severe corporate governance issue in any publicly listed business.

What can be said with some confidence is that revenue assurance practitioners are able to provide a vast number of consistent anecdotes relating to the causes of leakage and means to resolve them. Though there is little objective evidence relating to actual leakages approaching this scale in the public domain as this information per se is highly confidential, there are some indirect measures of data integrity that help give a sense of potential leakage. For example, in reconciling interconnect costs and revenues between telcos, a 5% variance is the common practice to accept before a disputed invoice can lead one party to withhold payment, and a 0.5% variance would be considered industry-leading practice according to best practice advice issued by the UK Revenue Assurance Group.

Revenue Assurance in Telecom

Although Revenue Assurance has always been present in the telecom parlance it has recently been brought at the forefront of the top management. This is due to several factors including

Revenue Assurance has been a problem for the telecom companies since the very early stages. Tracking of pulses, minutes, counts, bytes etc. has never been more difficult. One would think these would be easy for the tech-savvy telco companies. However, the truth has been just the opposite. In a hurry to release new technologies in the market, the Revenue Assurance systems are always lagging behind. Revenue Assurance in a telco environment covers a wide range of technical and business aspects. An RA operator needs to be aware of both OSS & BSS processes and internal dependencies to accurately decipher the revenue code.

What causes the problem

A telecom organization's revenue chain is usually a very complex set of inter-related technologies and processes providing a seamless set of services to the end consumer. As the set of technologies and business processes grows bigger and more complex, the chance of failure increases in each of its connections. A revenue leakage is typically attributed to when a telco organization is unable to bill correctly for a given service or to receive the correct payment. As the organization grows the probability of revenue leakage only increases.

Where is the problem

The most debated part of revenue assurance is where to start checking, i.e. at the network side, the rating side, the billing side, the interconnect side, the CRM side, etc. However, most surveys and reports state that the maximum leakage happens during the flow of Call Detail Records (CDRs) or Event Detail Records (EDRs) from the Switch to the respective rating / billing engines. Some of the common problem areas are :

Revenue assurance discipline

Among the disciplines in revenue assurance are:

1. The CORE functions of a revenue assurance group: Monitoring, Baselining, Auditing, Synchronizing, Investigating and Compliance.

2. Decomposing an organization's revenue assurance scope (The Revenue Management Chain).

3. Assessing and minimizing revenue loss risk.

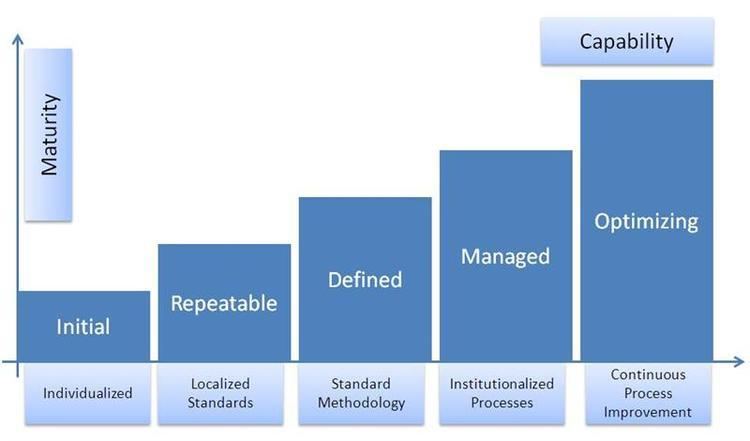

Maturity of Revenue Assurance

There is no formal maturity model for Revenue Assurance which is universally accepted. However the Revenue Assurance processes can be pegged against a generic five stage maturity model. The five stages are listed below and are described in terms of a Revenue Assurance Strategy, People, Process and technological advances.

RA Process Categories

The Revenue Assurance processes in many ways can be regarded as an auditing process. The objective is to ensure that policies of the organization are well implemented and that no or minimal revenue leakage is occurring. The RA processes have the capability to cover all departments and service lines in a telecommunications organization. There are many ways in which RA processes can be classified, however in view of an audit function; the RA processes can be categorized into Detective, Corrective and Preventive activities, controls or processes. Let's understand the difference with the help of an example. Supposing the objective is to ensure trunk groups correctly entered in the MSCs. The detective control would be to monitor Trunk Groups appearing in CDRs are harmonized with the master list and any deviations are reported. The corrective control would be to initiative a process and confirm with the Network / Wholesale team of all deviations found. The preventive control would be to set up a process with the Network / Wholesale team where all new trunk groups are first informed to the RA, Mediation, Wholesale and other essential departments and then made live on the Network.

Detective Processes

Revenue Assurance Detection is the process of spotting a change in value of a dimension relative to its movement from System A to System B or within a given systems itself. The change in the value is relative to a dimension is question. Detection in RA can be achieved by both manual and automated means. Typical detection activities include monitoring, summarization, investigation and auditing.

Corrective Processes

Correction is the set of activities and processes related around getting the process structures correct in order to minimize the changes identified as per the detection techniques. Correction itself is the act or method of correcting a discrepancy. Typically some information, configuration, amount or quantity needs to be added, edited or removed from a system, process or procedure in order to correct the anomaly. In Revenue Assurance activities, the process of correction of a root cause could involve correction of information, processes, technology or people.

Telecom Network technologies evolve at a rapid pace. Sometimes technologies need to be balanced in the Network. For example, having multiple vendors on the Network side could lead to a requirement of having time synchronizer equipment installed just to have CDRs showing consistent time and date related information. Any current implementation of Revenue Assurance becomes obsolete rapidly. As technologies evolve revenue assurance tools and coverage of the tools also need to evolve. This essentially means technology corrections need to be performed either on the hardware side or on the tool / application side. Technology corrections are rare and need to be performed with due diligence as technology corrections can be very expensive to an organization.

Preventive Processes

Prevention is the process of performing an activity in order to avoid a high risk situation. It is essentially an action carried out to de-risk a threat. For example, if there is risk that a tariff plan is not correctly implemented, then the preventive action could be to simulate calls on test SIMs on the new tariff plans prior to launch and confirm the tariffs coming in the test CDRs against the marketing or advertising department rates. Preventive activities lead to effective risk management around Revenue Assurance.

Tool for Revenue Assurance

Since Revenue Assurance is a very niche area in the telecommunications environment, there are some specific products and solutions supporting this subject. There are various vendors in the market which address either the complete suite of Revenue Assurance requirements or specialize in the specific domains. This section describes the basic features of a generic Revenue Assurance tool.

One must keep in mind that software RA solutions can only help in pointing toward the error locations or problem areas. When one addresses the question of developing an RA solution they need to consider the magnitude, scope and capacity of the systems available along with the intellect, skills, and the number of people accessible. Finally it is the people, their skills and knowledge that make a complete RA solution. An organization should be careful when automating revenue assurance as it may end up with an expensive and inflexible solution which no one can manage effectively. There are a variety of specialized RA products which have different characteristics including probing, RA add on modules on respective OSS / BSS elements. However the most common tool adopted by most Telecommunication companies is one which can simulate the natural process of the CDR flow from Network generation to Invoicing. Given below are some of the requirements (not exhaustive) of such a Revenue Assurance product.

Extract, Transform and Load

Telecommunications is an environment where there are many heterogeneous systems creating a multitude of data. Typically a single day’s information runs into many Giga Bytes or in some cases Tera Bytes also. This creates a need to have very proficient and rigorous extraction, transformation and loading tool for a Revenue Assurance application. Some of the common features of this tool are:

Reconciliations

One of the primary focus areas of a Revenue Assurance tool is to compare CDRs or XDRs from 2 different sources and checking if all the records from the first system have transferred properly to the second system keeping the appropriate business rules in consideration. This is achieved via comparative analysis of the records between the 2 systems either at the details record level or summary level by evaluating the common dimensions between the 2 data sets. Given below are some of the requirements (not exhaustive) which a Revenue Assurance Reconciliation side of the product should provide.

Analysis and KPIs

Once all the information has been received into the Revenue Assurance systems it time to crunch numbers and generate reports. The critical part is the analytical capabilities of the tool. The tool needs to have the ability to make sense of the problems in the vast set of data that it has gathered. This can only be done by a high performance analytical engine which should be capable of the following activities (non exhaustive):

Dash boarding

A Revenue Assurance dashboard is an easy to read, often single page, real-time user interface, showing a graphical presentation of the current status (snapshot) and historical trends of an organization’s Key Performance Indicators (KPIs) to enable instantaneous and informed decisions to be made at a glance. For example, a prepaid dashboard may show KPIs related to prepaid CDRs reconciliation, prepaid user profile reconciliation, balance reconciliations and voucher reconciliations carried out in real time or near real time.

Case Management

A case management capability in Revenue Assurance should be able to provide a 360 degree view of a given case. The tool should be able to track and resolve the identified discrepancies. The tool should handle each “case” in the system from the point where the system detected it, and manage follow up through the correction and reclamation processes, until the case is resolved. Based on a discrepancy in one given area, It should be able connect relevant information from various sources. For example, if a CDRs reconciliation has a problem, the case tool should be able to co-relate with respective user profiles, non-usage information, credits risks, network configurations etc. The case management component may have some of the following non exhaustive capabilities: