| ||

In economics, "rational expectations" are model-consistent expectations, in that agents inside the model on average assume the model's predictions are valid. Rational expectations ensure internal consistency in aggregate stochastic models. To obtain consistency within a model, the predictions of the future value of economically relevant variables are optimal given the decision-makers' information set and model structure. The rational expectations assumption is used especially in many contemporary macroeconomic models. Rational expectations does not imply individual rationality and should not be confused with rational choice theory, which is used extensively in, among others, game theory.

Contents

Since most macroeconomic models today study decisions over many periods, the expectations of workers, consumers and firms about future economic conditions are an essential part of the model. How to model these expectations has long been controversial, and it is well known that the macroeconomic predictions of the model may differ depending on the assumptions made about expectations (see Cobweb model). To assume rational expectations is to assume that agents' expectations may be wrong, but are correct on average over time. In other words, although the future is not fully predictable, agents' expectations are assumed not to be systematically biased and use all relevant information in forming expectations of economic variables.

This way of modeling expectations was originally proposed by John F. Muth (1961) and later became influential when it was used by Robert Lucas, Jr. and others. Modeling expectations is crucial in all models which study how a large number of individuals, firms and organizations make choices under uncertainty. For example, negotiations between workers and firms will be influenced by the expected level of inflation, and the value of a share of stock is dependent on the expected future income from that stock.

Deirdre McCloskey emphasized that "rational expectations" is an expression of intellectual modesty: "Muth's notion was that the professors [of economics], even if correct in their model of man, could do no better in predicting than could the hog farmer or steelmaker or insurance company. The notion is one of intellectual modesty. The common sense is "rationality": therefore Muth called the argument "rational expectations"."

Theory

Rational expectations theory defines this kind of expectations as being the best guess of the future (the optimal forecast) that uses all available information. Thus, it is assumed that outcomes that are being forecast do not differ systematically from the market equilibrium results. As a result, rational expectations do not differ systematically or predictably from equilibrium results. That is, it assumes that people do not make systematic errors when predicting the future, and deviations from perfect foresight are only random. In an economic model, this is typically modelled by assuming that the expected value of a variable is equal to the expected value predicted by the model.

For example, suppose that P is the equilibrium price in a simple market, determined by supply and demand. The theory of rational expectations says that the actual price will only deviate from the expectation if there is an 'information shock' caused by information unforeseeable at the time expectations were formed. In other words, ex ante the price is anticipated to equal its rational expectation:

where

Implications

Rational expectations theories were developed in response to perceived flaws in theories based on adaptive expectations. Under adaptive expectations, expectations of the future value of an economic variable are based on past values. For example, people would be assumed to predict inflation by looking at inflation last year and in previous years. Under adaptive expectations, if the economy suffers from constantly rising inflation rates (perhaps due to government policies), people would be assumed to always underestimate inflation. Many economists have regarded this as unrealistic, believing that rational individuals would sooner or later realize the trend and take it into account in forming their expectations.

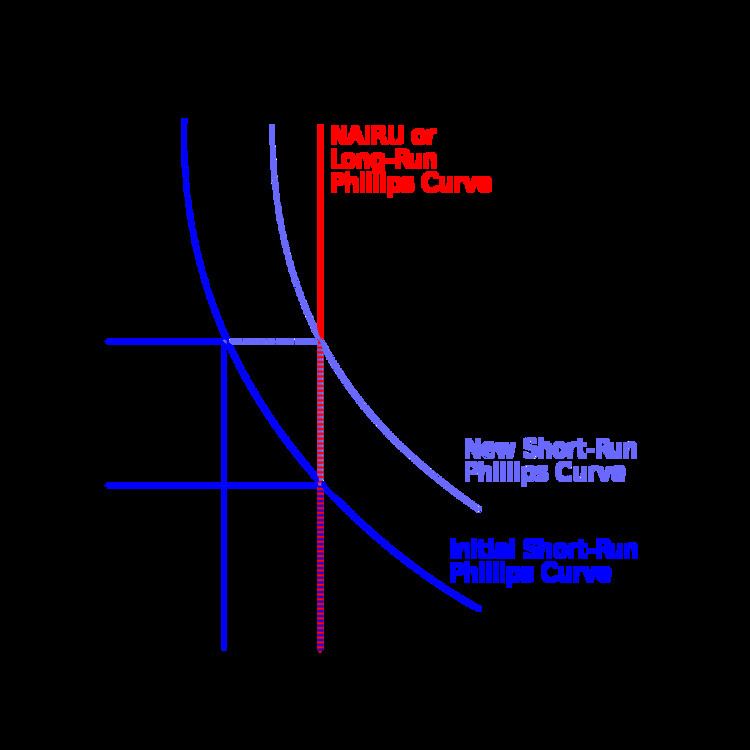

The rational expectations hypothesis has been used to support some strong conclusions about economic policymaking. An example is the policy ineffectiveness proposition developed by Thomas Sargent and Neil Wallace. If the Federal Reserve attempts to lower unemployment through expansionary monetary policy economic agents will anticipate the effects of the change of policy and raise their expectations of future inflation accordingly. This in turn will counteract the expansionary effect of the increased money supply. All that the government can do is raise the inflation rate, not employment. This is a distinctly New Classical outcome. During the 1970s rational expectations appeared to have made previous macroeconomic theory largely obsolete, which culminated with the Lucas critique. However, rational expectations theory has been widely adopted as a modelling assumption even outside of New Classical macroeconomics thanks to the work of New Keynesians such as Stanley Fischer.

If agents do not (or cannot) form rational expectations or if prices are not completely flexible, discretional and completely anticipated economic policy actions can trigger real changes.