| ||

The Eurozone crisis is an ongoing financial crisis that has made it difficult or impossible for some countries in the euro area to repay or re-finance their government debt without the assistance of third parties.

Contents

- EU emergency measures

- European Financial Stability Facility EFSF

- Reception by financial markets

- Usage of EFSF funds

- European Financial Stabilisation Mechanism EFSM

- Brussels agreement and aftermath

- Final agreement on the second bailout package

- European Central Bank

- Long Term Refinancing Operation LTRO

- Resignations

- Money supply growth

- Reorganization of the European banking system

- Outright Monetary Transactions OMTs

- European Stability Mechanism ESM

- European Fiscal Compact

- References

The European sovereign debt crisis resulted from a combination of complex factors, including the globalization of finance; easy credit conditions during the 2002–2008 period that encouraged high-risk lending and borrowing practices; the 2007–2012 global financial crisis; international trade imbalances; real-estate bubbles that have since burst; the 2008–2012 global recession; fiscal policy choices related to government revenues and expenses; and approaches used by nations to bail out troubled banking industries and private bondholders, assuming private debt burdens or socializing losses.

One narrative describing the causes of the crisis begins with the significant increase in savings available for investment during the 2000–2007 period when the global pool of fixed-income securities increased from approximately $36 trillion in 2000 to $70 trillion by 2007. This "Giant Pool of Money" increased as savings from high-growth developing nations entered global capital markets. Investors searching for higher yields than those offered by U.S. Treasury bonds sought alternatives globally.

The temptation offered by such readily available savings overwhelmed the policy and regulatory control mechanisms in country after country, as lenders and borrowers put these savings to use, generating bubble after bubble across the globe. While these bubbles have burst, causing asset prices (e.g., housing and commercial property) to decline, the liabilities owed to global investors remain at full price, generating questions regarding the solvency of governments and their banking systems.

How each European country involved in this crisis borrowed and invested the money varies. For example, Ireland's banks lent the money to property developers, generating a massive property bubble. When the bubble burst, Ireland's government and taxpayers assumed private debts. In Greece, the government increased its commitments to public workers in the form of extremely generous wage and pension benefits, with the former doubling in real terms over 10 years. Iceland's banking system grew enormously, creating debts to global investors (external debts) several times GDP.

The three crucial problems of the European economic governance emerged during the crisis are the asymmetry in the policy-making process for centralized policies and decentralized ones, ambiguities related to the coherent functioning of the euro area and the EU as well as of distribution of powers between national institutions and supranational ones, which implies the dilemma of legitimacy of the European economic governance and its rules.

The interconnection in the global financial system means that if one nation defaults on its sovereign debt or enters into recession putting some of the external private debt at risk, the banking systems of creditor nations face losses. For example, in October 2011, Italian borrowers owed French banks $366 billion (net). Should Italy be unable to finance itself, the French banking system and economy could come under significant pressure, which in turn would affect France's creditors and so on. This is referred to as financial contagion. Another factor contributing to interconnection is the concept of debt protection. Institutions entered into contracts called credit default swaps (CDS) that result in payment should default occur on a particular debt instrument (including government issued bonds). But, since multiple CDSs can be purchased on the same security, it is unclear what exposure each country's banking system now has to CDS.

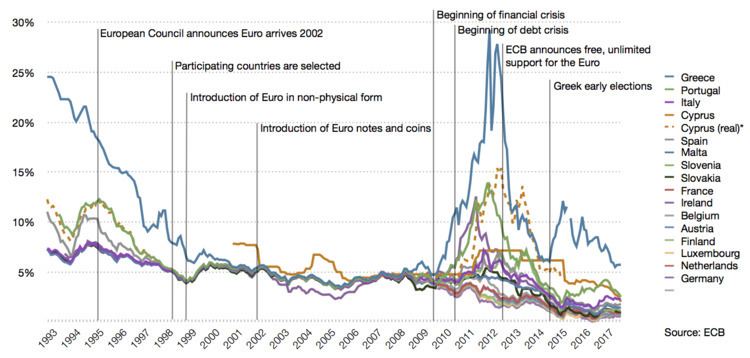

Greece hid its growing debt and deceived EU officials with the help of derivatives designed by major banks. Although some financial institutions clearly profited from the growing Greek government debt in the short run, there was a long lead-up to the crisis.

EU emergency measures

The table below provides an overview of the financial composition of all bailout programs being initiated for EU member states, since the Global Financial Crisis erupted in September 2008. EU member states outside the eurozone (marked with yellow in the table) have no access to the funds provided by EFSF/ESM, but can be covered with rescue loans from EU's Balance of Payments programme (BoP), IMF and bilateral loans (with an extra possible assistance from the Worldbank/EIB/EBRD if classified as a development country). Since October 2012, the ESM as a permanent new financial stability fund to cover any future potential bailout packages within the eurozone, has effectively replaced the now defunct GLF + EFSM + EFSF funds. Whenever pledged funds in a scheduled bailout program were not transferred in full, the table has noted this by writing "Y out of X".

European Financial Stability Facility (EFSF)

On 9 May 2010, the 27 EU member states agreed to create the European Financial Stability Facility, a legal instrument aiming at preserving financial stability in Europe by providing financial assistance to eurozone states in difficulty. The EFSF can issue bonds or other debt instruments on the market with the support of the German Debt Management Office to raise the funds needed to provide loans to eurozone countries in financial troubles, recapitalize banks or buy sovereign debt.

Emissions of bonds are backed by guarantees given by the euro area member states in proportion to their share in the paid-up capital of the European Central Bank. The €440 billion lending capacity of the facility is jointly and severally guaranteed by the eurozone countries' governments and may be combined with loans up to €60 billion from the European Financial Stabilisation Mechanism (reliant on funds raised by the European Commission using the EU budget as collateral) and up to €250 billion from the International Monetary Fund (IMF) to obtain a financial safety net up to €750 billion.

The EFSF issued €5 billion of five-year bonds in its inaugural benchmark issue 25 January 2011, attracting an order book of €44.5 billion. This amount is a record for any sovereign bond in Europe, and €24.5 billion more than the European Financial Stabilisation Mechanism (EFSM), a separate European Union funding vehicle, with a €5 billion issue in the first week of January 2011.

On 29 November 2011, the member state finance ministers agreed to expand the EFSF by creating certificates that could guarantee up to 30% of new issues from troubled euro-area governments, and to create investment vehicles that would boost the EFSF’s firepower to intervene in primary and secondary bond markets.

Reception by financial markets

Stocks surged worldwide after the EU announced the EFSF's creation. The facility eased fears that the Greek debt crisis would spread, and this led to some stocks rising to the highest level in a year or more. The euro made its biggest gain in 18 months, before falling to a new four-year low a week later. Shortly after the euro rose again as hedge funds and other short-term traders unwound short positions and carry trades in the currency. Commodity prices also rose following the announcement.

The dollar Libor held at a nine-month high. Default swaps also fell. The VIX closed down a record almost 30%, after a record weekly rise the preceding week that prompted the bailout. The agreement is interpreted as allowing the ECB to start buying government debt from the secondary market which is expected to reduce bond yields. As a result, Greek bond yields fell sharply from over 10% to just over 5%. Asian bonds yields also fell with the EU bailout.)

Usage of EFSF funds

The EFSF only raises funds after an aid request is made by a country. As of the end of July 2012, it has been activated various times. In November 2010, it financed €17.7 billion of the total €67.5 billion rescue package for Ireland (the rest was loaned from individual European countries, the European Commission and the IMF). In May 2011 it contributed one third of the €78 billion package for Portugal. As part of the second bailout for Greece, the loan was shifted to the EFSF, amounting to €164 billion (130bn new package plus 34.4bn remaining from Greek Loan Facility) throughout 2014. On 20 July 2012, European finance ministers sanctioned the first tranche of a partial bail-out worth up to €100 billion for Spanish banks. This leaves the EFSF with €148 billion or an equivalent of €444 billion in leveraged firepower.

The EFSF is set to expire in 2013, running some months parallel to the permanent €500 billion rescue funding program called the European Stability Mechanism (ESM), which will start operating as soon as member states representing 90% of the capital commitments have ratified it. (see section: ESM)

On 13 January 2012, Standard & Poor’s downgraded France and Austria from AAA rating, lowered Spain, Italy (and five other) euro members further, and maintained the top credit rating for Finland, Germany, Luxembourg, and the Netherlands; shortly after, S&P also downgraded the EFSF from AAA to AA+.

European Financial Stabilisation Mechanism (EFSM)

On 5 January 2011, the European Union created the European Financial Stabilisation Mechanism (EFSM), an emergency funding programme reliant upon funds raised on the financial markets and guaranteed by the European Commission using the budget of the European Union as collateral. It runs under the supervision of the Commission and aims at preserving financial stability in Europe by providing financial assistance to EU member states in economic difficulty. The Commission fund, backed by all 27 European Union members, has the authority to raise up to €60 billion and is rated AAA by Fitch, Moody's and Standard & Poor's.

Under the EFSM, the EU successfully placed in the capital markets a €5 billion issue of bonds as part of the financial support package agreed for Ireland, at a borrowing cost for the EFSM of 2.59%.

Like the EFSF, the EFSM was replaced by the permanent rescue funding programme ESM, which was launched in September 2012.

Brussels agreement and aftermath

On 26 October 2011, leaders of the 17 eurozone countries met in Brussels and agreed on a 50% write-off of Greek sovereign debt held by banks, a fourfold increase (to about €1 trillion) in bail-out funds held under the European Financial Stability Facility, an increased mandatory level of 9% for bank capitalisation within the EU and a set of commitments from Italy to take measures to reduce its national debt. Also pledged was €35 billion in "credit enhancement" to mitigate losses likely to be suffered by European banks. José Manuel Barroso characterised the package as a set of "exceptional measures for exceptional times".

The package's acceptance was put into doubt on 31 October when Greek Prime Minister George Papandreou announced that a referendum would be held so that the Greek people would have the final say on the bailout, upsetting financial markets. On 3 November 2011 the promised Greek referendum on the bailout package was withdrawn by Prime Minister Papandreou.

In late 2011, Landon Thomas in the New York Times noted that some, at least, European banks were maintaining high dividend payout rates and none were getting capital injections from their governments even while being required to improve capital ratios. Thomas quoted Richard Koo, an economist based in Japan, an expert on that country's banking crisis, and specialist in balance sheet recessions, as saying:

I do not think Europeans understand the implications of a systemic banking crisis.... When all banks are forced to raise capital at the same time, the result is going to be even weaker banks and an even longer recession – if not depression.... Government intervention should be the first resort, not the last resort.

Beyond equity issuance and debt-to-equity conversion, then, one analyst "said that as banks find it more difficult to raise funds, they will move faster to cut down on loans and unload lagging assets" as they work to improve capital ratios. This latter contraction of balance sheets "could lead to a depression”, the analyst said. Reduced lending was a circumstance already at the time being seen in a "deepen[ing] crisis" in commodities trade finance in western Europe.

Final agreement on the second bailout package

In a marathon meeting on 20/21 February 2012 the Eurogroup agreed with the IMF and the Institute of International Finance on the final conditions of the second bailout package worth €130 billion. The lenders agreed to increase the nominal haircut from 50% to 53.5%. EU Member States agreed to an additional retroactive lowering of the interest rates of the Greek Loan Facility to a level of just 150 basis points above the Euribor. Furthermore, governments of Member States where central banks currently hold Greek government bonds in their investment portfolio commit to pass on to Greece an amount equal to any future income until 2020. Altogether this should bring down Greece's debt to between 117% and 120.5% of GDP by 2020.

European Central Bank

The European Central Bank (ECB) has taken a series of measures aimed at reducing volatility in the financial markets and at improving liquidity.

In May 2010 it took the following actions:

The move took some pressure off Greek government bonds, which had just been downgraded to junk status, making it difficult for the government to raise money on capital markets.

On 30 November 2011, the ECB, the U.S. Federal Reserve, the central banks of Canada, Japan, Britain and the Swiss National Bank provided global financial markets with additional liquidity to ward off the debt crisis and to support the real economy. The central banks agreed to lower the cost of dollar currency swaps by 50 basis points to come into effect on 5 December 2011. They also agreed to provide each other with abundant liquidity to make sure that commercial banks stay liquid in other currencies.

Long Term Refinancing Operation (LTRO)

Though the ECB's main refinancing operations (MRO) are from repo auctions with a (bi)weekly maturity and monthly maturation, the ECB now conducts Long Term Refinancing Operations (LTROs), maturing after three months, six months, 12 months and 36 months. In 2003, refinancing via LTROs amounted to 45 bln euro which is about 20% of overall liquidity provided by the ECB.

The ECB's first supplementary longer-term refinancing operation (LTRO) with a six-month maturity was announced March 2008. Previously the longest tender offered was three months. It announced two 3-month and one 6-month full allotment of Long Term Refinancing Operations (LTROs). The first tender was settled 3 April, and was more than four times oversubscribed. The €25 billion auction drew bids amounting to €103.1 billion, from 177 banks. Another six-month tender was allotted on 9 July, again to the amount of €25 billion. The first 12-month LTRO in June 2009 had close to 1100 bidders.

On 22 December 2011, the ECB started the biggest infusion of credit into the European banking system in the euro's 13-year history. Under its Long Term Refinancing Operations (LTROs) it loaned €489 billion to 523 banks for an exceptionally long period of three years at a rate of just one percent. Previous refinancing operations matured after three, six and twelve months. The by far biggest amount of €325 billion was tapped by banks in Greece, Ireland, Italy and Spain.

This way the ECB tried to make sure that banks have enough cash to pay off €200 billion of their own maturing debts in the first three months of 2012, and at the same time keep operating and loaning to businesses so that a credit crunch does not choke off economic growth. It also hoped that banks would use some of the money to buy government bonds, effectively easing the debt crisis. On 29 February 2012, the ECB held a second auction, LTRO2, providing 800 Eurozone banks with further €529.5 billion in cheap loans. Net new borrowing under the €529.5 billion February auction was around €313 billion; out of a total of €256 billion existing ECB lending (MRO + 3m&6m LTROs), €215 billion was rolled into LTRO2.

ECB lending has largely replaced inter-bank lending. Spain has €365 billion and Italy has €281 billion of borrowings from the ECB (June 2012 data). Germany has €275 billion on deposit.

Resignations

In September 2011, Jürgen Stark became the second German after Axel A. Weber to resign from the ECB Governing Council in 2011. Weber, the former Deutsche Bundesbank president, was once thought to be a likely successor to Jean-Claude Trichet as bank president. He and Stark were both thought to have resigned due to "unhappiness with the ECB’s bond purchases, which critics say erode the bank’s independence". Stark was "probably the most hawkish" member of the council when he resigned. Weber was replaced by his Bundesbank successor Jens Weidmann, while Belgium's Peter Praet took Stark's original position, heading the ECB's economics department.

Money supply growth

In April, 2012, statistics showed a growth trend in the M1 "core" money supply. Having fallen from an over 9% growth rate in mid-2008 to negative 1% +/- for several months in 2011, M1 core has built to a 2-3% range in early 2012. "'It is still early days but a further recovery in peripheral real M1 would suggest an end to recessions by late 2012,' said Simon Ward from Henderson Global Investors who collects the data." While attributing the money supply growth to ECB's LTRO policies, an analysis in The Telegraph said lending "continued to fall across the eurozone in March [and] ... [t]he jury is out on the ... three-year lending adventure (LTRO)".

Reorganization of the European banking system

On June 16, 2012, the European Central Bank together with other European leaders hammered out plans for the ECB to become a bank regulator and to form a deposit insurance program to augment national programs. Other economic reforms promoting European growth and employment were also proposed.

Outright Monetary Transactions (OMTs)

On 6 September 2012, the ECB announced to offer additional financial support in the form of some yield-lowering bond purchases (OMT), for all eurozone countries involved in a sovereign state bailout program from EFSF/ESM. A eurozone country can benefit from the program if – and for as long as – it is found to suffer from stressed bond yields at excessive levels; but only at the point of time where the country possesses/regains a complete market access – and only if the country still comply with all terms in the signed Memorandum of Understanding (MoU) agreement. Countries receiving a precautionary programme rather than a sovereign bailout, will per definition have complete market access and thus qualify for OMT support if also suffering from stressed interest rates on its government bonds. In regards of countries receiving a sovereign bailout (Ireland, Portugal and Greece), they will on the other hand not qualify for OMT support before they have regained complete market access, which will normally only happen after having received the last scheduled bailout disbursement. Despite none OMT programmes were ready to start in September/October, the financial markets straight away took notice of the additionally planned OMT packages from ECB, and started slowly to price-in a decline of both short-term and long-term interest rates in all European countries previously suffering from stressed and elevated interest levels (as OMTs were regarded as an extra potential back-stop to counter the frozen liquidity and highly stressed rates; and just the knowledge about their potential existence in the very near future helped to calm the markets).

If Spain signs a negotiated Memorandum of Understanding with the Troika (EC, ECB and IMF) outlining ESM shall offer a precautionary programme with credit lines for the Spanish government to potentially draw on if needed (beside of the bank recapitalisation package they already applied for), this would qualify Spain also to receive the OMT support from ECB, as the sovereign state would still continue to operate with a complete market access with the precautionary conditioned credit line. In regards of Ireland, Portugal and Greece, they on the other hand have not yet regained complete market access, and thus do not yet qualify for OMT support.

European Stability Mechanism (ESM)

The European Stability Mechanism (ESM) is a permanent rescue funding programme to succeed the temporary European Financial Stability Facility and European Financial Stabilisation Mechanism in July 2012 but it had to be postponed until after the Federal Constitutional Court of Germany had confirmed the legality of the measures on 12 September 2012. The permanent bailout fund entered into force for 16 signatories on 27 September 2012. It became effective in Estonia on 4 October 2012 after the completion of their ratification process.

On 16 December 2010 the European Council agreed a two line amendment to the EU Lisbon Treaty to allow for a permanent bail-out mechanism to be established including stronger sanctions. In March 2011, the European Parliament approved the treaty amendment after receiving assurances that the European Commission, rather than EU states, would play 'a central role' in running the ESM. The ESM is an intergovernmental organisation under public international law. It is located in Luxembourg.

Such a mechanism serves as a "financial firewall." Instead of a default by one country rippling through the entire interconnected financial system, the firewall mechanism can ensure that downstream nations and banking systems are protected by guaranteeing some or all of their obligations. Then the single default can be managed while limiting financial contagion.

European Fiscal Compact

In March 2011 a new reform of the Stability and Growth Pact was initiated, aiming at straightening the rules by adopting an automatic procedure for imposing of penalties in case of breaches of either the 3% deficit or the 60% debt rules. By the end of the year, Germany, France and some other smaller EU countries went a step further and vowed to create a fiscal union across the eurozone with strict and enforceable fiscal rules and automatic penalties embedded in the EU treaties. On 9 December 2011 at the European Council meeting, all 17 members of the eurozone and six countries that aspire to join agreed on a new intergovernmental treaty to put strict caps on government spending and borrowing, with penalties for those countries who violate the limits. All other non-eurozone countries apart from the UK are also prepared to join in, subject to parliamentary vote. The treaty will enter into force on 1 January 2013, if by that time 12 members of the euro area have ratified it.

Originally EU leaders planned to change existing EU treaties but this was blocked by British prime minister David Cameron, who demanded that the City of London be excluded from future financial regulations, including the proposed EU financial transaction tax. By the end of the day, 26 countries had agreed to the plan, leaving the United Kingdom as the only country not willing to join. Cameron subsequently conceded that his action had failed to secure any safeguards for the UK. Britain's refusal to be part of the fiscal compact to safeguard the eurozone constituted a de facto refusal (PM David Cameron vetoed the project) to engage in any radical revision of the Lisbon Treaty. John Rentoul of The Independent concluded that "Any Prime Minister would have done as Cameron did".