A markup rule refers to the pricing practice of a producer with market power, where a firm charges a fixed mark up over its marginal cost.

Mathematically, the markup rule can be derived for a firm with price-setting power by maximizing the following equation for "Economic Profit":

π = P ( Q ) ⋅ Q − C ( Q ) whereQ = quantity sold,P(Q) =

inverse demand function, and thereby the Price at which Q can be sold given the existing DemandC(Q) = Total (Economic) Cost of producing Q.

π = Economic Profit

Profit maximization means that the derivative of π with respect to Q is set equal to 0. Profit of a firm is given by total revenue (price times quantity sold) minus total cost:

P ′ ( Q ) ⋅ Q + P − C ′ ( Q ) = 0 whereQ = quantity sold,P'(Q) = the partial derivative of the inverse

demand function.C'(Q) = Marginal Cost, or the partial derivative of Total Cost with respect to output.

This yields:

P ′ ( Q ) ⋅ Q + P = C ′ ( Q ) or "Marginal Revenue" = "Marginal Cost".

P ⋅ ( P ′ ( Q ) ⋅ Q / P + 1 ) = M C By definition P ′ ( Q ) ⋅ Q / P is the reciprocal of the price elasticity of demand (or 1 / ϵ ). Hence

P ⋅ ( 1 + 1 / ϵ ) = P ⋅ ( 1 + ϵ ϵ ) = M C Letting η be the reciprocal of the price elasticity of demand,

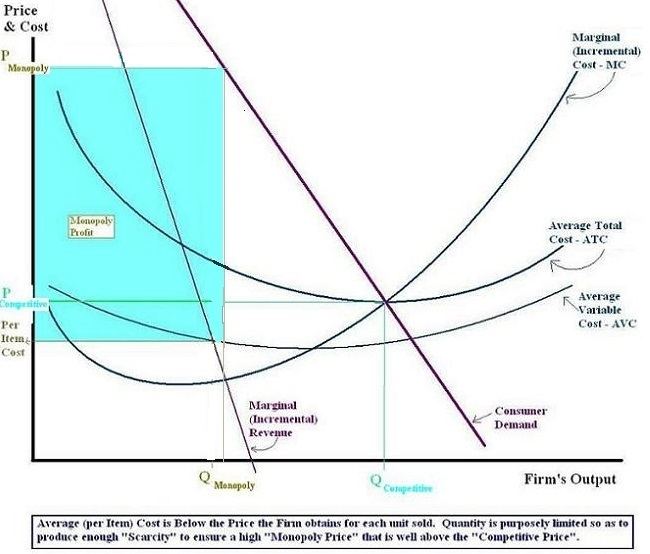

P = ( 1 1 + η ) ⋅ M C Thus a firm with market power chooses the quantity at which the demand price satisfies this rule. Since for a price setting firm η < 0 this means that a firm with market power will charge a price above marginal cost and thus earn a monopoly rent. On the other hand, a competitive firm by definition faces a perfectly elastic demand, hence it believes η = 0 which means that it sets price equal to marginal cost.

The rule also implies that, absent menu costs, a firm with market power will never choose a point on the inelastic portion of its demand curve.