| ||

John murphy explains intermarket analysis part 1

Intermarket analysis is a relationship, or a measurable correlation between certain markets. It is a form of fundamental analysis, without a time delay. Supporters of intermarket analysis state that it can be done by applying the statistical methods like correlation. Critics of intermarket analysis refute statistical methods and use only price indicators for fundamental analysis.

Contents

- John murphy explains intermarket analysis part 1

- Intermarket analysis

- Points to consider

- Opposition views

- Examples

- References

In John Murphy's first book, published in 1991 on Intermarket analysis he used the crash of 1987 to lay out his Intermarket hypothesis. Murray Ruggiero published Intermarket based trading systems in 1994.

Hence, intermarket market analysis can be thought of as a type of instantaneous fundamental analysis and is not really meant to work on a tick by tick basis. It gives you a general bias and direction. Thus, your intermarket work looks for times that these underlying relationships are moving opposite to the market you are trading.

There are many approaches to intermarket analysis like mechanical, rule based (while not mechanical via a different angle). One can use intermarket analysis of Oil along with the intermarket analysis of other key markets to help with profitable day trading of the Russell 2000 Emini ER2.

There are many supporters and detractors for this theory and the points to consider regarding the Intermarket Relationship have been clarified in the following sections.

Intermarket analysis

Points to consider

1) They are tried and time-tested intermarket relationships with easily available free data and a simple spreadsheet or charting program. The quickest function to use is the simple correlation study, wherein one variable is compared with a second variable i.e. the correlation between two data series.

If it is positive; the correlation value shall go as high as + 1.0 – representing a perfect and positive correlation between the two series of prices. Moreover, a perfect inverse (negative) correlation depicts a value as low as - 1.0. Readings near the zero line would show no discernible correlation between the two samples.

Moreover, it is rare to have a perfect correlation between any two market for a very long period of time, but most analysts would probably agree that any reading sustained over the +0.7 or under the –0.7 level (which would equate to approximately a 70% correlation) would be statistically significant. Also, if the correlation value went from a positive to a negative correlation frequently, the relationship would most likely be unstable, and probably useless for trading.

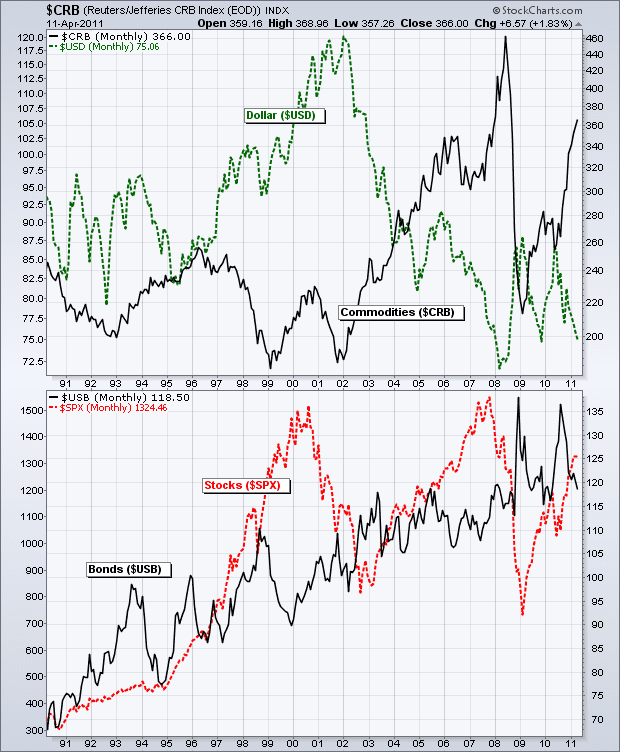

2) The most widely accepted correlation is the inverse correlation between stock prices and interest rates; for it is a general assumption that as interest rates go higher, the stock prices go lower, and conversely, as interest rates go down, the stock prices go up.

3) A really simple concept for Intermarket-based systems. For positively correlated markets, the concept is:

Various concepts are used to define an up and down trend; if we use the price relative to a moving average, then: For negatively correlated market we have as follows:

Opposition views

The views of the people who oppose the intermarket relationship along with arguments are as follows: 1) However, there is a lot of opposition against the intermarket analysis as many who have used it, are just blindly using it by optimizing parameters without giving a thought as to why a given market should work and what logic reasons, based on the premise a given intermarket relationship would decouple.

Intermarket relationships are not always constant; they go through periods of ebbing and flowing. Thus, we cannot expect perfect results or answers, but what we can have some statistics regarding the markets behavior.

Although, the intermarket relationships does decouple at times, it does not mean that it is not valid or reliable. However, by proper research, we can analyze the reason for the decoupling and predict the same. Taking for example, in 1993, both the CRB Index and the 30-year bond rallied that summer; these two markets were negatively correlated. The problem was as the interest rates were falling, prices of bonds were rising so rapidly which caused the effect - An Intermarket inversion. Research findings states that with 2-3 sigma moves; would cause these problems. The logic is that interest rates falling stimulated the economy; which caused the fear of inflation and commodity prices to rally.

2) It can be shown that many stock indexes, exchange-traded funds and even some mutual funds are useful in predicting the prices of the underlying related futures. Stock prices lead commodity prices in many cases. It can because more money is spent in the stock analyst world, so their research contains future prediction of the underlying prices of the related commodity or futures.

Some classic examples are as follows:

Above are negatively correlated as the price of chemicals increases; which shall be good for these stocks; it also indicates future inflation.

4) Some points to note regarding the relationship between stocks to each other and the relationship of commodities to each other, which are totally two different aspects; as the commodities are more closely correlated. This is a global world, so if things are priced in dollars, thus what is paid would have a component in the value of the dollars versus other currencies, like the Euro.

Taking a simple example; you have 100 gallons of gas, you live in Germany. You want 200 euro for it. Assuming that the dollar is .80 euro; you require $240 for the gas. If the dollar drops to .70 euro, you require $260.00, in order to get your 200 euro. Problems in the Middle East could change the value of your gas to 250 Euro and that is why the relationship between the dollar and crude does not always work.

5) Another argument against intermarket analysis is that count matters more which are not the Elliott's 5/3 counts. The market thus repeats a subtler, more extended series of sequences which needs to be discovered and they will lend you greater predictive power than you've ever felt.

They think that comparing related movements is beneficial like with the Dow, S/P, and NASDAQ Comp and is called the “RELATIONAL ANALYSIS.” Comparing related instruments can provide clues that would otherwise remain unknown and it is a powerful concept.

6) Moreover, the critics state that Charles Dow was about 90 years before Murray when he saw the Dow Industrials and Rails as linked and the recent research shows that markets can and do run in similar directions and create similar oscillations but no two markets oscillate identically and that's what is important. If markets act conversely just one time then their intermarket relationship cannot be trusted and can never be used to accurately determine the "true trend" of any market.

The above can be refuted as there are many profitable traders who would vouch for the above statement to be neither true nor correct. In the matter of fact it is by measuring the intermarket dynamics (which are always changing) that one can determine when different market setups are taking place, and trade accordingly.

Examples

1) Considering the interest in Crude, Natural Gas; a public source for oil and gas, exploration, refining and production type indexes is required and several of them exist on both the S&P500 and NASDAQ.

Moreover, Energy related mutual funds are also required. It has been noticed that Mutual funds are often good at predicting underlying futures markets. A good example is Fidelity Select Chemical fund to trade Thirty Year bond or Ten Year note.

An example is the symbol !EXV, "SELECT SPDR ENERGY INDEX" shows how well this intermarket technology works. The factors to consider are:

The trend in crude was then based as if the close of crude was above or below a 40-day moving average of crude. The same trend is defined in SELECT SPDR ENERGY INDEX and is based on if the close of it was above or below its 25-day moving average.

2) Considering issues as the Japanese rate hike impact market in the intermarket analysis and the building of a QQQQ PSQ rotation system for IRA account traders.

In terms of the Japanese rate hike; it would increase the value of the Yen, but that does not mean that the dollar index will decrease because of the other currencies involved. Another point is that if it is assumed that the Yen would rally due to the rate hike; however the Middle East problems and the fact the Bank of Japan talked down future rate increases has caused the dollar to rally. This is why, intermarket relationships can often decouples, during time of disasters, but if they are reliable often enough one can do well using intermarket analysis.

3) Another example of the dollar index and crude from 1984; the problem with the dollar index relationship is it can decouples sometimes for a year or more.

In addition this shows the power of the relationships with the mutual funds and exchange-traded funds as none of these combination for the dollar index made money on the short side, the best lost a few hundred dollars. The earlier example using an energy based ETF made 20K on the short side in the past 5.5 years during crude big bull market.

4) Considering the Dollar in the negatively correlated to Crude; John Murphy talked about this relationship in his original intermarket book (1991) and so did Murray Ruggiero in Cybernetic Trading Strategies. The reason is that Crude is priced in dollars; so falling dollar means it takes more dollars to buy the same amount of crude. This relationship decouples during times of unrest in the Middle East and this is why it is less reliable than the relationship with energy stocks, which can be improved upon if the trades are filtered using correlation analysis.

TradersStudio offers many intermarket trading systems including the Turtle packs