| ||

An information technology audit, or information systems audit, is an examination of the management controls within an Information technology (IT) infrastructure. The evaluation of obtained evidence determines if the information systems are safeguarding assets, maintaining data integrity, and operating effectively to achieve the organization's goals or objectives. These reviews may be performed in conjunction with a financial statement audit, internal audit, or other form of attestation engagement.

Contents

- Purpose

- Types of IT audits

- IT Audit process

- Security

- History of IT Auditing

- Qualifications

- Professional certifications

- Principles of an IT Audit

- Emerging Issues

- Web Presence Audits

- Enterprise Communications Audits

- References

IT audits are also known as "automated data processing (ADP) audits" and "computer audits". They were formerly called "electronic data processing (EDP) audits".

Purpose

An IT audit is different from a financial statement audit. While a financial audit's purpose is to evaluate whether an organization is adhering to standard accounting practices, the purposes of an IT audit are to evaluate the system's internal control design and effectiveness. This includes, but is not limited to, efficiency and security protocols, development processes, and IT governance or oversight. Installing controls are necessary but not sufficient to provide adequate security. People responsible for security must consider if the controls are installed as intended, if they are effective if any breach in security has occurred and if so, what actions can be done to prevent future breaches. These inquiries must be answered by independent and unbiased observers. These observers are performing the task of information systems auditing. In an Information Systems (IS) environment, an audit is an examination of information systems, their inputs, outputs, and processing.

The primary functions of an IT audit are to evaluate the systems that are in place to guard an organization's information. Specifically, information technology audits are used to evaluate the organization's ability to protect its information assets and to properly dispense information to authorized parties. The IT audit aims to evaluate the following:

Will the organization's computer systems be available for the business at all times when required? (known as availability) Will the information in the systems be disclosed only to authorized users? (known as security and confidentiality) Will the information provided by the system always be accurate, reliable, and timely? (measures the integrity) In this way, the audit hopes to assess the risk to the company's valuable asset (its information) and establish methods of minimizing those risks.

IT audits are also known as Information Systems Audit, ADP audits, EDP audits, or computer audits

Types of IT audits

Various authorities have created differing taxonomies to distinguish the various types of IT audits. Goodman & Lawless state that there are three specific systematic approaches to carry out an IT audit:

Others describe the spectrum of IT audits with five categories of audits:

And some lump all IT audits as being one of only two type: "general control review" audits or "application control review" audits.

A number of IT Audit professionals from the Information Assurance realm consider there to be three fundamental types of controls regardless of the type of audit to be performed, especially in the IT realm. Many frameworks and standards try to break controls into different disciplines or arenas, terming them “Security Controls“, ”Access Controls“, “IA Controls” in an effort to define the types of controls involved. At a more fundamental level, these controls can be shown to consist of three types of fundamental controls: Protective/Preventative Controls, Detective Controls and Reactive/Corrective Controls.

In an IS system, there are two types of auditors and audits: internal and external. IS auditing is usually a part of accounting internal auditing, and is frequently performed by corporate internal auditors. An external auditor reviews the findings of the internal audit as well as the inputs, processing and outputs of information systems. The external audit of information systems is frequently a part of the overall external auditing performed by a Certified Public Accountant (CPA) firm.

IS auditing considers all the potential hazards and controls in information systems. It focuses on issues like operations, data, integrity, software applications, security, privacy, budgets and expenditures, cost control, and productivity. Guidelines are available to assist auditors in their jobs, such as those from Information Systems Audit and Control Association.

IT Audit process

The following are basic steps in performing the Information Technology Audit Process:

- Planning IN

- Studying and Evaluating Controls

- Testing and Evaluating Controls

- Reporting

- Follow-up

- reports

Security

Auditing information security is a vital part of any IT audit and is often understood to be the primary purpose of an IT Audit. The broad scope of auditing information security includes such topics as data centers (the physical security of data centers and the logical security of databases, servers and network infrastructure components), networks and application security. Like most technical realms, these topics are always evolving; IT auditors must constantly continue to expand their knowledge and understanding of the systems and environment& pursuit in system company.

Several training and certification organizations have evolved. Currently, the major certifying bodies, in the field, are the Institute of Internal Auditors (IIA), the SANS Institute (specifically, the audit specific branch of SANS and GIAC) and ISACA. While CPAs and other traditional auditors can be engaged for IT Audits, organizations are well advised to require that individuals with some type of IT specific audit certification are employed when validating the controls surrounding IT systems.

History of IT Auditing

The concept of IT auditing was formed in the mid-1960s. Since that time, IT auditing has gone through numerous changes, largely due to advances in technology and the incorporation of technology into business.

Currently, there are many IT dependent companies that rely on the Information Technology in order to operate their business e.g. Telecommunication or Banking company. For the other types of business, IT plays the big part of company including the applying of workflow instead of using the paper request form, using the application control instead of manual control which is more reliable or implementing the ERP application to facilitate the organization by using only 1 application. According to these, the importance of IT Audit is constantly increased. One of the most important role of the IT Audit is to audit over the critical system in order to support the Financial audit or to support the specific regulations announced e.g. SOX.

Qualifications

The CISM and CAP credentials are the two newest security auditing credentials, offered by the ISACA and (ISC)², respectively. Strictly speaking, only the CISA or GSNA title would sufficiently demonstrate competences regarding both information technology and audit aspects with the CISA being more audit focused and the GSNA being more information technology focused.

Outside of the US, various credentials exist. For example, the Netherlands has the RE credential (as granted by the NOREA [Dutch site] IT-auditors' association), which among others requires a post-graduate IT-audit education from an accredited university, subscription to a Code of Ethics, and adherence to continuous education requirements.

Professional certifications

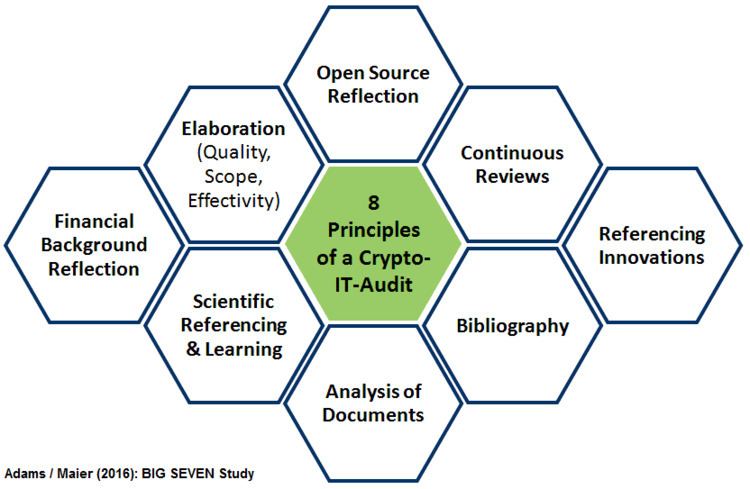

Principles of an IT Audit

The following principles of an audit should find a reflection:

This list of audit principles for crypto applications describes - beyond the methods of technical analysis - particularly core values, that should be taken into account

Emerging Issues

There are also new audits being imposed by various standard boards which are required to be performed, depending upon the audited organization, which will affect IT and ensure that IT departments are performing certain functions and controls appropriately to be considered compliant. Examples of such audits are SSAE 16, ISAE 3402, and ISO27001:2013.

Web Presence Audits

The extension of the corporate IT presence beyond the corporate firewall (e.g. the adoption of social media by the enterprise along with the proliferation of cloud-based tools like social media management systems) has elevated the importance of incorporating web presence audits into the IT/IS audit. The purposes of these audits include ensuring the company is taking the necessary steps to:

Enterprise Communications Audits

The rise of VOIP networks and issues like BYOD and the increasing capabilities of modern enterprise telephony systems causes increased risk of critical telephony infrastructure being mis-configured, leaving the enterprise open to the possibility of communications fraud or reduced system stability. Banks, Financial institutions, and contact centers typically set up policies to be enforced across their communications systems. The task of auditing that the communications systems are in compliance with the policy falls on specialized telecom auditors. These audits ensure that the company's communication systems:

Enterprise Communications Audits are also called voice audits, but the term is increasingly deprecated as communications infrastructure increasingly becomes data-oriented and data-dependent. The term "telephony audit" is also deprecated because modern communications infrastructure, especially when dealing with customers, is omni-channel, where interaction takes place across multiple channels, not just over the telephone. One of the key issues that plagues enterprise communication audits is the lack of industry-defined or government-approved standards. IT audits are built on the basis of adherence to standards and policies published by organizations such as NIST and PCI, but the absence of such standards for enterprise communications audits means that these audits have to be based an organization's internal standards and policies, rather than industry standards. As a result, enterprise communications audits are still manually done, with random sampling checks. Policy Audit Automation tools for enterprise communications have only recently become available.