| ||

Financial risk modeling refers to the use of formal econometric techniques to determine the aggregate risk in a financial portfolio. Risk modeling is one of many subtasks within the broader area of financial modeling.

Risk modeling uses a variety of techniques including market risk, value at risk (VaR), historical simulation (HS), or extreme value theory (EVT) in order to analyze a portfolio and make forecasts of the likely losses that would be incurred for a variety of risks. Such risks are typically grouped into credit risk, liquidity risk, market risk, and operational risk categories.

Many large financial intermediary firms use risk modeling to help portfolio managers assess the amount of capital reserves to maintain, and to help guide their purchases and sales of various classes of financial assets.

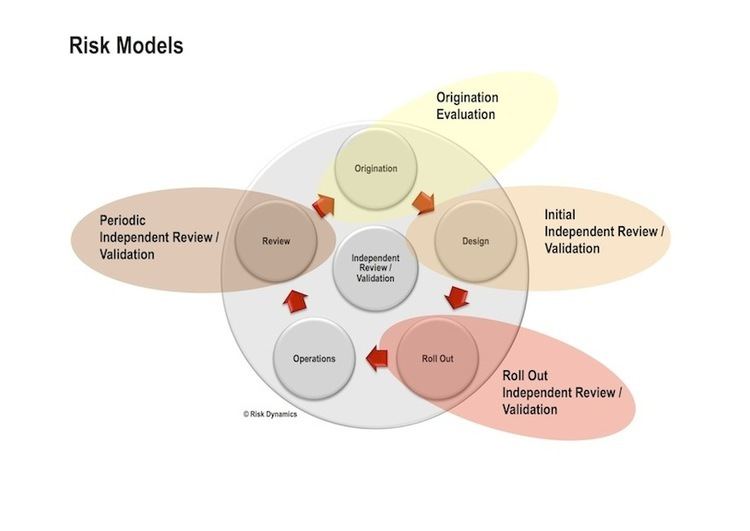

Formal risk modeling is required under the Basel II proposal for all the major international banking institutions by the various national depository institution regulators. In the past, risk analysis was done qualitatively but now with the advent of powerful computing software, quantitative risk analysis can be done quickly and effortlessly.

Modeling the changes by distributions with finite variance is now known to be inappropriate. Benoît Mandelbrot found in the 1960s that changes in prices in financial markets do not follow a Gaussian distribution, but are rather modeled better by Lévy stable distributions. The scale of change, or volatility, depends on the length of the time interval to a power a bit more than 1/2. Large changes up or down, also called fat tails, are more likely than what one would calculate using a Gaussian distribution with an estimated standard deviation.

Criticism

Quantitative risk analysis and its modeling have been under question in the light of corporate scandals in the past few years (most notably, Enron), Basel II, the revised FAS 123R and the Sarbanes-Oxley Act, and for their failure to predict the financial crash of 2008.