| ||

China's electric power industry is the world's largest electricity consumer, passing the United States in 2011 after rapid growth since the early 1990s.

Contents

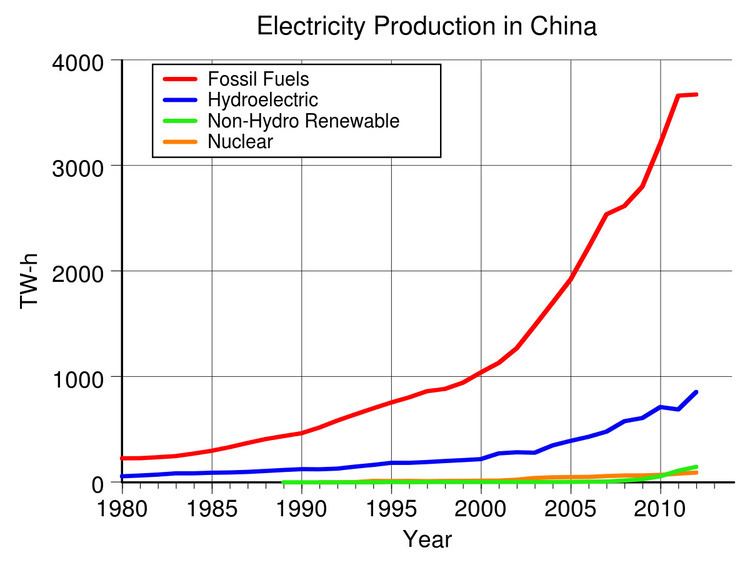

Most of the electricity comes from coal which accounted for an estimated 73% of domestic electricity production in 2014. Coal-fired electricity production has declined since 2013 coinciding with a major boom in renewable energy.

China currently lacks a single national grid. There are currently 6 wide area synchronous grids. The lack of a single grid frequently creates power shortages.

China has abundant energy with the world's third-largest coal reserves and massive hydroelectric resources. There is however a geographical mismatch between the location of the coal fields in the north-east (Heilongjiang, Jilin, and Liaoning) and north (Shanxi, Shaanxi, and Henan), hydropower in the south-west (Sichuan, Yunnan, and Tibet), and the fast-growing industrial load centers of the east (Shanghai-Zhejiang) and south (Guangdong, Fujian).

History

In April 1996, an Electric Power Law was implemented, a major event in China's electric power industry. The law set out to promote the development of the electric power industry, to protect legal rights of investors, managers and consumers, and to regulate generation, distribution and consumption.

Before 1994 electricity supply was managed by electric power bureaus of the provincial governments. Now utilities are managed by corporations outside of the government administration structure.

To end the State Power Corporation's (SPC) monopoly of the power industry, China's State Council dismantled the corporation in December 2002 and set up 11 smaller companies. SPC had owned 46% of the country's electrical generation assets and 90% of the electrical supply assets. The smaller companies include two electric power grid operators, five electric power generation companies and four relevant business companies. Each of the five electric power generation companies owns less than 20% (32 GW of electricity generation capacity) of China's market share for electric power generation. Ongoing reforms aim to separate power plants from power-supply networks, privatize a significant amount of state-owned property, encourage competition, and revamp pricing mechanisms.

It is expected that the municipal electric power companies will be divided into electric power generating and electric power supply companies. A policy of competition between the different generators will be implemented in the next years.

South China from the Changjiang valley down to the South China Sea was the first part of the economy to liberalize in the 1980s and 1990s and is home to much of the country's most modern and often foreign-invested manufacturing industries. Northern and north-eastern China's older industrial base has fallen behind, remains focused on the domestic economy and has suffered relative decline.

In recent history, China's power industry is characterized by fast growth and an enormous installed base. In 2014, it had the largest installed electricity generation capacity in the world with 1505 GW and generated 5583 TWh China also has the largest thermal power capacity, the largest hydropower capacity, the largest wind power capacity and the largest solar capacity in the world. Despite an expected rapid increase in installed capacity scheduled in 2014 for both wind and solar, and expected increase to 60 GW in nuclear by 2020, coal will still account between 65% and 75% of capacity in 2020.

In Spring, 2011, it was reported by The New York Times that due to increased demand and price controls shortages of electricity existed and power outages should be anticipated. The government-regulated price electricity could be sold for had not matched rising prices for coal.

Problems

Price caps encourage wasteful use of cheap electricity and therefore producers are struggling to generate enough power. It seems likely the cost of power will need to rise substantially over the medium term (2–5 years) to curb wasteful energy consumption and slow the rate of growth in electricity demand. In theory, the government could raise power costs by a similar amount across the whole of China in the interests of inter-regional equity.

China's power transmission system remains under-developed. Regional power shortages occur frequently when generation drops in one province or region and the lack of long-distance power transmission capacity means that power cannot be routed in from other regions where there is surplus capacity. There is no unified national grid. Instead there are six major regional grids: five managed by the giant State Grid Corporation (north, north-east, east, central and north-west) and an independent grid in the south managed by the South China State Grid Corp, covering the light manufacturing hub around Guangzhou-Shenzhen and the inland areas of Guangdong, Guangxi and Guizhou. Northern areas experience shortages in winter due to increased heating demand and problems with coal deliveries. Eastern and southern areas are prone to shortages in late spring/early summer as temperatures and airconditioning demand rise, while reservoir levels and hydro output fall until the arrival of the summer rains in July and August. Guangdong and other southern provinces import substantial quantities of expensive fuel oil and diesel to run additional generation capacity to cope with the resulting power gap.

The lack of a unified national grid system also hampers the efficiency of power generation nationwide and heightens the risk of localised shortages. Even within these grids transmission capacity is limited. Many towns and enterprises rely on local off-grid generating plants. More importantly, inter-connections between the grids are weak and long distance transmission capacity is small.

The rail system has struggled to deliver adequate quantities of coal to the generators. Ice storms, flooding or droughts which disrupt rail and river deliveries quickly lead to shortages and power outages. The enormous volume of coal burning also generates massive pollution.

Transmission infrastructure

The central government has made creation of a unified national grid system a top economic priority to improve the efficiency of the whole power system and reduce the risk of localised energy shortages. It will also enable the country to tap the enormous hydro potential from western China to meet booming demand from the eastern coastal provinces. China is planning for smart grid and related Advanced Metering Infrastructure.

Ultra-high-voltage transmission

The main problem in China is the voltage drop when power is sent over very long distances from one region of the country to another.

Long distance inter-regional transmission have been implemented by using ultra-high voltages (UHV) of 800 kV, based on an extension of technology already in use in other parts of the world.

The government plans as many as eight long-distance UHV lines by 2015 and 15 by 2020.

- HVDC Gezhouba -

- HVDC Three Gorges-Guangdong

Following research and testing, SGCC has announced construction of the first long-distance UHV line from Sichuan, which is rich in hydro-electric potential, to the eastern load center of Shanghai.

Shanghai already receives hydro-electric power from the massive Three Gorges Dam on the Changjiang (Yangtze) at Sandouping in Hubei province. But the new DC 800 kV UHV line would enable it to receive power from twice as far west from the Xiangjiaba dam on the Jinsha river (a tributary of the Changjiang much further upstream).

Xiangjiaba will have total generating capacity of 6,400 MW. When completed, the nearby Xiluodu Dam will add a further 12,600 MW (about 55 percent of the size of the planned Three Gorges output), making it the world's third-largest hydro-electric dam, ranking after the Three Gorges and Brazil's Itaipu.

Xiluodu and Xiangjiaba are two of a series of massive new hydro projects that the government plans in south-western and western China to take advantage of the massive run off from the Himalayas and the Tibet plateau.

SGCC plans to bring a single pole of the Xiangjiaba-Shanghai line into commercial operation within two years (2010) and the second pole a year later (2011). SGCC plans to complete a total of 10 UHV projects by 2015 and 15 by 2020. [1] In most cases, these will bring power from massive new hydro facilities in south-western China to the industrial and residential centers of the east.

Companies

In terms of the investment amount of China's listed power companies, the top three regions are Guangdong province, Inner Mongolia Autonomous Region and Shanghai, whose investment ratios are 15.33%, 13.84% and 10.53% respectively, followed by Sichuan and Beijing.

China's listed power companies invest mostly in thermal power, hydropower and thermoelectricity, with their investments reaching CNY216.38 billion, CNY97.73 billion and CNY48.58 billion respectively in 2007. Investment in gas exploration and coal mining follow as the next prevalent investment occurrences.

Major players in China's electric power industry include:

The five majors, and their listed subsidiaries: The five majors are all SOEs directly administered by SASAC. Their listed subsidiaries are substantially independent, hence counted as IPPs, and are major power providers in their own right. Typically each of the big 5 has about 10% of national installed capacity, and their listed subsidiary an extra 4 or 5% on top of that.

Additionally two other SOEs also have listed IPP subsidiaries:

Secondary companies:

Nuclear and hydro:

Grid operators include: