| ||

In mathematics, a Bessel process, named after Friedrich Bessel, is a type of stochastic process.

Contents

Formal definition

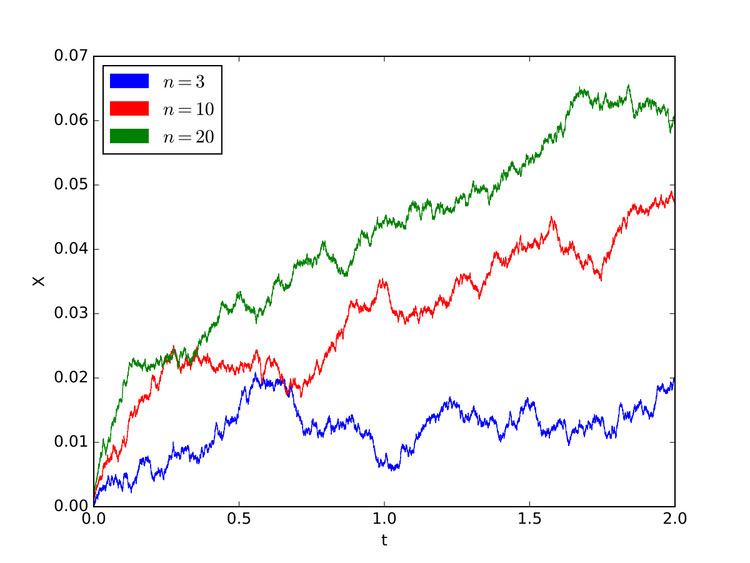

The Bessel process of order n is the real-valued process X given by

where ||·|| denotes the Euclidean norm in Rn and W is an n-dimensional Wiener process (Brownian motion) started from the origin. The n-dimensional Bessel process is the solution to the stochastic differential equation

where Z is a 1-dimensional Wiener process (Brownian motion). Note that this SDE makes sense for any real parameter

Notation

A notation for the Bessel process of dimension n' started at zero is BES0(n).

In specific dimensions

For n ≥ 2, the n-dimensional Wiener process is transient from its starting point: with probability one, i.e., Xt > 0 for all t > 0. It is, however, neighbourhood-recurrent for n = 2, meaning that with probability 1, for any r > 0, there are arbitrarily large t with Xt < r; on the other hand, it is truly transient for n > 2, meaning that Xt ≥ r for all t sufficiently large.

For n ≤ 0, the Bessel process is usually started at points other than 0, since the drift to 0 so strong that the process becomes stuck at 0 as soon as it hits 0.

Relationship with Brownian motion

0- and 2-dimensional Bessel processes are related to local times of Brownian motion via the Ray-Knight theorems.

The law of a Brownian motion near x-extrema is the law of a 3-dimensional Bessel process (theorem of Tanaka).