| ||

Balanced scorecard

The balanced scorecard (BSC) is a strategy performance management tool – a semi-standard structured report, supported by design methods and automation tools, that can be used by managers to keep track of the execution of activities by the staff within their control and to monitor the consequences arising from these actions.

Contents

- Balanced scorecard

- Balanced scorecard introduction

- Use

- History

- Characteristics

- Design

- First generation

- Second generation

- Third generation

- Popularity

- Variants

- Criticism

- Software tools

- References

The phrase 'balanced scorecard' is commonly used in two broad forms:

- As individual scorecards that contain measures to manage performance, those scorecards may be operational or have a more strategic intent; and

- As a Strategic Management System, as originally defined by Kaplan & Norton.

The critical characteristics that define a balanced scorecard are:

Balanced scorecard introduction

Use

Balanced scorecard is an example of a closed-loop controller or cybernetic control applied to the management of the implementation of a strategy. Closed-loop or cybernetic control is where actual performance is measured, the measured value is compared to a reference value and based on the difference between the two corrective interventions are made as required. Such control requires three things to be effective:

Within the strategy management context, all three of these characteristic closed-loop control elements need to be derived from the organisation's strategy and also need to reflect the ability of the observer to both monitor performance and subsequently intervene – both of which may be constrained. Initially, Balanced Scorecard emerged as a performance management system, over a period of time it has come to be known as a strategy management system, with its ultimate aim being the achievement of long term financial performance. Balanced scorecard is seen as a strategic management system enabling business leaders to meet the challenge of strategy execution.

Two of the ideas that underpin modern balanced scorecard designs concern facilitating the creation of such a control – through making it easier to select which data to observe, and ensuring that the choice of data is consistent with the ability of the observer to intervene.

History

Organizations have used systems consisting of a mix of financial and non-financial measures to track progress for quite some time. One such system was created by Art Schneiderman in 1987 at Analog Devices, a mid-sized semi-conductor company; the Analog Devices Balanced Scorecard. Schneiderman's design was similar to what is now recognised as a "First Generation" Balanced Scorecard design.

In 1990 Art Schneiderman participated in an unrelated research study led by Robert S. Kaplan in conjunction with US management consultancy Nolan-Norton, and during this study described his work on performance measurement. Subsequently, Kaplan and David P. Norton included anonymous details of this balanced scorecard design in a 1992 article. Kaplan and Norton's article wasn't the only paper on the topic published in early 1992 but the 1992 Kaplan and Norton paper was a popular success, and was quickly followed by a second in 1993. In 1996, the two authors published a book The Balanced Scorecard. These articles and the first book spread knowledge of the concept of balanced scorecard widely, and has led to Kaplan and Norton being seen as the creators of the concept.

While the "corporate scorecard" terminology was coined by Art Schneiderman, the roots of performance management as an activity run deep in management literature and practice. Management historians such as Alfred Chandler suggest the origins of performance management can be seen in the emergence of the complex organisation – most notably during the 19th Century in the USA. More recent influences may include the pioneering work of General Electric on performance measurement reporting in the 1950s and the work of French process engineers (who created the tableau de bord – literally, a "dashboard" of performance measures) in the early part of the 20th century. The tool also draws strongly on the ideas of the 'resource based view of the firm' proposed by Edith Penrose. However it should be noted that none of these influences is explicitly linked to original descriptions of balanced scorecard by Schneiderman, Maisel, or Kaplan & Norton.

Kaplan and Norton's first book remains their most popular. The book reflects the earliest incarnations of balanced scorecards – effectively restating the concept as described in the second Harvard Business Review article. Their second book, The Strategy Focused Organization, echoed work by others (particularly a book published the year before by Olve et al. in Scandinavia) on the value of visually documenting the links between measures by proposing the "Strategic Linkage Model" or strategy map.

As the title of Kaplan and Norton's second book highlights, even by 2000 the focus of attention among thought-leaders was moving from the design of Balanced Scorecards themselves, towards the use of Balanced Scorecard as a focal point within a more comprehensive strategic management system. Subsequent writing on Balanced Scorecard by Kaplan & Norton has focused on uses of Balanced Scorecard rather than its design (e.g. "The Execution Premium" in 2008), however many others have continued to refine the device itself (e.g. Abernethy et al.).

Characteristics

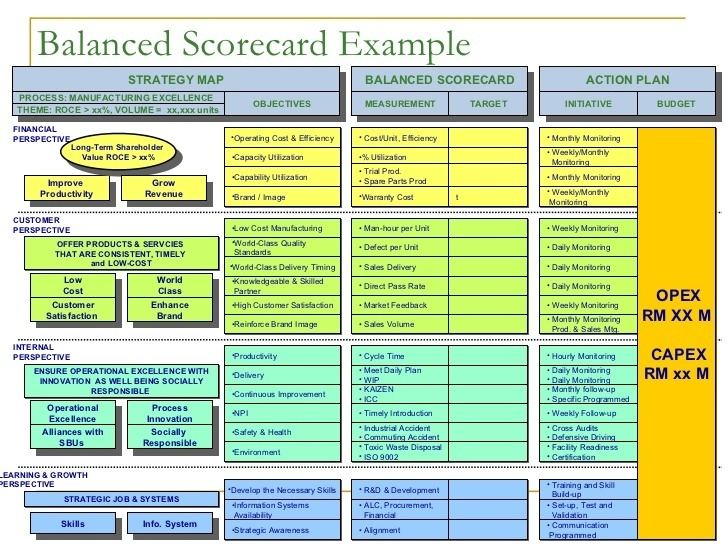

The characteristics of the balanced scorecard and its derivatives is the presentation of a mixture of financial and non-financial measures each compared to a 'target' value within a single concise report. The report is not meant to be a replacement for traditional financial or operational reports but a succinct summary that captures the information most relevant to those reading it. It is the method by which this 'most relevant' information is determined (i.e., the design processes used to select the content) that most differentiates the various versions of the tool in circulation. The balanced scorecard indirectly also provides a useful insight into an organisation's strategy – by requiring general strategic statements (e.g. mission, vision) to be precipitated into more specific/tangible forms.

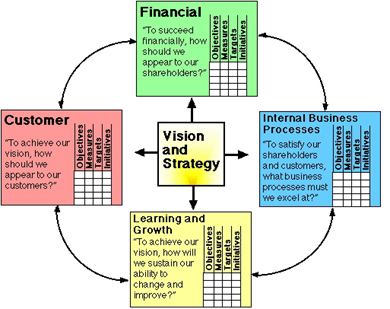

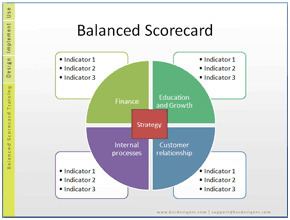

The first versions of balanced scorecard asserted that relevance should derive from the corporate strategy, and proposed design methods that focused on choosing measures and targets associated with the main activities required to implement the strategy. As the initial audience for this were the readers of the Harvard Business Review, the proposal was translated into a form that made sense to a typical reader of that journal – managers of US commercial businesses. Accordingly, initial designs were encouraged to measure three categories of non-financial measure in addition to financial outputs – those of "customer," "internal business processes" and "learning and growth." These categories were not so relevant to non-profits or units within complex organizations (which might have high degrees of internal specialization), and much of the early literature on balanced scorecard focused on suggestions of alternative 'perspectives' that might have more relevance to these groups.

Modern balanced scorecards have evolved since the initial ideas proposed in the late 1980s and early 1990s, and the modern performance management tools including Balanced Scorecard are significantly improved – being more flexible (to suit a wider range of organisational types) and more effective (as design methods have evolved to make them easier to design, and use).

Design

Design of a balanced scorecard is about the identification of a small number of financial and non-financial measures and attaching targets to them, so that when they are reviewed it is possible to determine whether current performance 'meets expectations'. By alerting managers to areas where performance deviates from expectations, they can be encouraged to focus their attention on these areas, and hopefully as a result trigger improved performance within the part of the organization they lead.

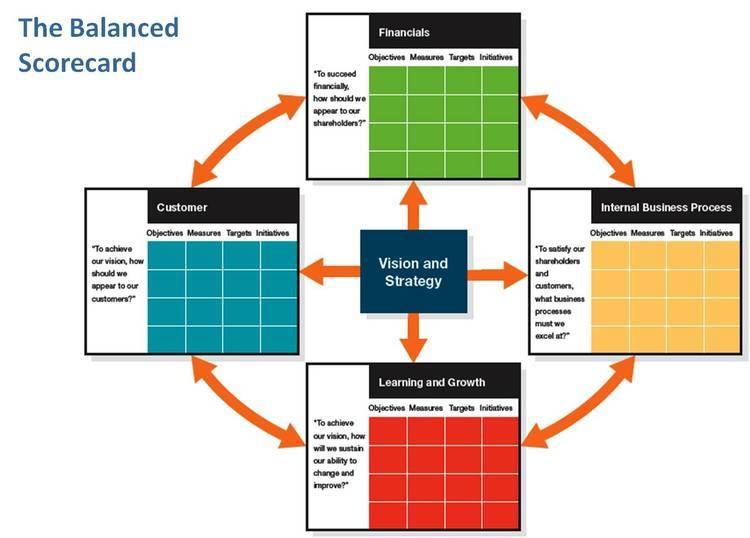

The original thinking behind a balanced scorecard was for it to be focused on information relating to the implementation of a strategy, and over time there has been a blurring of the boundaries between conventional strategic planning and control activities and those required to design a balanced scorecard. This is illustrated well by the four steps required to design a balanced scorecard included in Kaplan & Norton's writing on the subject in the late 1990s:

- Translating the vision into operational goals;

- Communicating the vision and link it to individual performance;

- Business planning; index setting

- Feedback and learning, and adjusting the strategy accordingly.

These steps go far beyond the simple task of identifying a small number of financial and non-financial measures, but illustrate the requirement for whatever design process is used to fit within broader thinking about how the resulting balanced scorecard will integrate with the wider business management process.

Although it helps focus managers' attention on strategic issues and the management of the implementation of strategy, it is important to remember that the balanced scorecard itself has no role in the formation of strategy. In fact, balanced scorecards can co-exist with strategic planning systems and other tools.

First generation

The first generation of balanced scorecard designs used a "4 perspective" approach to identify what measures to use to track the implementation of strategy. `The original four "perspectives" proposed were:

The idea was that managers used these perspective headings to prompt the selection of a small number of measures that informed on that aspect of the organisation's strategic performance. The perspective headings show that Kaplan and Norton were thinking about the needs of non-divisional commercial organisations in their initial design. These headings are not very helpful to other kinds of organisations (e.g. multi-divisional or multi-national commercial organisations, governmental organisations, non-profits, non-governmental organisations, government agencies etc.), and much of what has been written on balanced scorecard since has, in one way or another, focused on the identification of alternative headings more suited to a broader range of organisations, and also suggested using either additional or fewer perspectives (e.g. Butler et al. (1997), Ahn (2001), Elefalke (2001), Brignall (2002), Irwin (2002), Radnor et al. (2003)).

These suggestions were notably triggered by a recognition that different but equivalent headings would yield alternative sets of measures, and this represents the major design challenge faced with this type of balanced scorecard design: justifying the choice of measures made. "Of all the measures you could have chosen, why did you choose these?" These issues contribute to dis-satisfaction with early Balanced Scorecard designs, since if users are not confident that the measures within the Balanced Scorecard are well chosen, they will have less confidence in the information it provides.

Although less common, these early-style balanced scorecards are still designed and used today.

In short, first generation balanced scorecards are hard to design in a way that builds confidence that they are well designed. Because of this, many are abandoned soon after completion.

Second generation

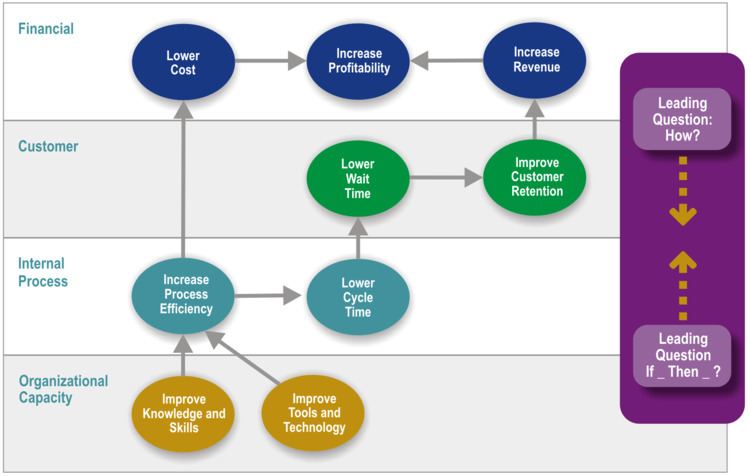

In the mid-1990s, an improved design method emerged. In the new method, measures are selected based on a set of "strategic objectives" plotted on a "strategic linkage model" or "strategy map". With this modified approach, the strategic objectives are distributed across the four measurement perspectives, so as to "connect the dots" to form a visual presentation of strategy and measures.

In this modified version of balanced scorecard design, managers select a few strategic objectives within each of the perspectives, and then define the cause-effect chain among these objectives by drawing links between them to create a "strategic linkage model". A balanced scorecard of strategic performance measures is then derived directly by selecting one or two measures for each strategic objective. This type of approach provides greater contextual justification for the measures chosen, and is generally easier for managers to work through. This style of balanced scorecard has been commonly used since 1996 or so: it is significantly different in approach to the methods originally proposed, and so can be thought of as representing the "2nd generation" of design approach adopted for balanced scorecard since its introduction.

Third generation

In the late 1990s, the design approach had evolved yet again. One problem with the "second generation" design approach described above was that the plotting of causal links amongst twenty or so medium-term strategic goals was still a relatively abstract activity. In practice it ignored the fact that opportunities to intervene, to influence strategic goals are, and need to be, anchored in current and real management activity. Secondly, the need to "roll forward" and test the impact of these goals necessitated the creation of an additional design instrument: the Vision or Destination Statement. This device was a statement of what "strategic success", or the "strategic end-state", looked like. It was quickly realized that if a Destination Statement was created at the beginning of the design process, then it was easier to select strategic activity and outcome objectives to respond to it. Measures and targets could then be selected to track the achievement of these objectives. Design methods that incorporate a Destination Statement or equivalent (e.g. the results-based management method proposed by the UN in 2002) represent a tangibly different design approach to those that went before, and have been proposed as representing a "third generation" design method for balanced scorecards.

Design methods for balanced scorecards continue to evolve and adapt to reflect the deficiencies in the currently used methods, and the particular needs of communities of interest (e.g. NGO's and government departments have found the third generation methods embedded in results-based management more useful than first or second generation design methods).

This generation refined the second generation of balanced scorecards to give more relevance and functionality to strategic objectives. The major difference is the incorporation of Destination Statements. Other key components are strategic objectives, strategic linkage model and perspectives, measures and initiatives.

Popularity

In 1997, Kurtzman found that 64 percent of the companies questioned were measuring performance from a number of perspectives in a similar way to the balanced scorecard. Balanced scorecards have been implemented by government agencies, military units, business units and corporations as a whole, non-profit organizations, and schools.

Balanced scorecard has been widely adopted, and has been found to be the most popular performance management framework in a recent survey

Many examples of balanced scorecards can be found via web searches. However, adapting one organization's balanced scorecard to another is generally not advised by theorists, who believe that much of the benefit of the balanced scorecard comes from the design process itself. Indeed, it could be argued that many failures in the early days of balanced scorecard could be attributed to this problem, in that early balanced scorecards were often designed remotely by consultants. Managers did not trust, and so failed to engage with and use, these measure suites created by people lacking knowledge of the organization and management responsibility.

Variants

Since the balanced scorecard was popularized in the early 1990s, a large number of alternatives to the original 'four box' balanced scorecard promoted by Kaplan and Norton in their various articles and books have emerged. Most have very limited application, and are typically proposed either by academics as vehicles for expanding the dialogue beyond the financial bottom line – e.g. Brignall (2002) or consultants as an attempt at differentiation to promote sales of books and / or consultancy (e.g. Bourne (2002); Niven (2002)).

Many of the structural variations proposed are broadly similar, and a research paper published in 2004 attempted to identify a pattern in these variations – noting three distinct types of variation. The variations appeared to be part of an evolution of the balanced scorecard concept, and so the paper refers to these distinct types as "generations". Broadly, the original 'measures in boxes' type design (as proposed by Kaplan & Norton) constitutes the 1st generation balanced scorecard design; balanced scorecard designs that include a 'strategy map' or 'strategic linkage model' (e.g. the Performance Prism, later Kaplan & Norton designs the Performance Driver model of Olve, Roy & Wetter (English translation 1999, 1st published in Swedish 1997)) constitute the 2nd Generation of Balanced Scorecard design; and designs that augment the strategy map / strategic linkage model with a separate document describing the long-term outcomes sought from the strategy (the "destination statement" idea) comprise the 3rd generation balanced scorecard design.

Variants that feature adaptations of the structure of balanced scorecard to suit better a particular viewpoint or agenda are numerous. Examples of the focus of such adaptations include the triple bottom line, decision support, public sector management, and health care management. The performance management elements of the UN's Results Based Management system have strong design and structural similarities to those used in the 3rd Generation Balanced Scorecard design approach.

Balanced scorecard is also often linked to quality management tools and activities. Although there are clear areas of cross-over and association, the two sets of tools are complementary rather than duplicative.

A common use of balanced scorecard is to support the payments of incentives to individuals, even though it was not designed for this purpose and is not particularly suited to it.

Criticism

The balanced scorecard has attracted criticism from a variety of sources. Most have come from the academic community, who dislike the empirical nature of the framework: Kaplan and Norton notoriously failed to include any citation of earlier articles in their initial papers on the topic. Some of this criticism focuses on technical flaws in the methods and design of the original balanced scorecard proposed by Kaplan and Norton,. Other academics have simply focused on the lack of citation support.

A second kind of criticism is that the balanced scorecard does not provide a bottom line score or a unified view with clear recommendations: it is simply a list of metrics (e.g. Jensen 2001). These critics usually include in their criticism suggestions about how the 'unanswered' question postulated could be answered, but typically the unanswered question relate to things outside the scope of balanced scorecard itself (such as developing strategies) (e.g. Brignall)

A third kind of criticism is that the model fails to fully reflect the needs of stakeholders – putting bias on financial stakeholders over others. Early forms of Balanced Scorecard proposed by Kaplan & Norton focused on the needs of commercial organisations in the USA – where this focus on investment return was appropriate. This focus was maintained through subsequent revisions. Even now over 20 years after they were first proposed, the four most common perspectives in Balanced Scorecard designs mirror the four proposed in the original Kaplan & Norton paper. However, as noted earlier in this article, there have been many studies that suggest other perspectives might better reflect the priorities of organisations – particularly but not exclusively relating to the needs of organisations in the public and Non Governmental sectors. For instance, the balanced scorecard does not address important aspects of nonprofit strategy such as social dimensions, human resource elements, political issues and the distinctive nature of competition and collaboration in nonprofit settings. Thus, the model seems to be less effective in nonprofit organisations as the model’s strategy, cause-and-effect relationships and its four linked perspectives are incompatible to the unique nonprofit environment. More modern design approaches such as 3rd Generation Balanced Scorecard and the UN's Results Based Management methods explicitly consider the interests of wider stakeholder groups, and perhaps address this issue in its entirety.

There are few empirical studies linking the use of balanced scorecards to better decision making or improved financial performance of companies, but some work has been done in these areas. However, broadcast surveys of usage have difficulties in this respect, due to the wide variations in definition of 'what a balanced scorecard is' noted above (making it hard to work out in a survey if you are comparing like with like). Single organization case studies suffer from the 'lack of a control' issue common to any study of organizational change – what the organization would have achieved if the change had not been made isn't known, so it is difficult to attribute changes observed over time to a single intervention (such as introducing a balanced scorecard). However, such studies as have been done have typically found balanced scorecard to be useful.

A few studies go further, trying to explain PMS size differences in terms of cause and effect. For example, Hvolby and Thorstenson (2000) and McAdam (2000) suggest that the Balanced Scorecard is completely unsuitable for SMEs because of their lack of a longer-term strategic focus. They also argue that the characteristics of SMEs make most, if not all, PM models inappropriate although they do not develop the argument in terms of causality. Similarly, Rompho’s (2011) study of a failed implementation of the Balanced Scorecard in an SME attributed the cause to too many changes to the organisation’s strategy. Others have suggested that SMEs have limited knowledge about performance measurement in general (Rantanen and Holtari 2000) and do not understand the benefits of PMS implementation (McAdam 2000; Bourne 2001), but none of these studies attempts to theorise the reasons behind their findings.

Software tools

It is important to recognize that the balanced scorecard by definition is not a complex thing – typically no more than about 20 measures spread across a mix of financial and non-financial topics, and easily reported manually (on paper, or using simple office software).

The processes of collecting, reporting, and distributing balanced scorecard information can be labor-intensive and prone to procedural problems (for example, getting all relevant people to return the information required by the required date). The simplest mechanism to use is to delegate these activities to an individual, and many Balanced Scorecards are reported via ad-hoc methods based around email, phone calls and office software.

In more complex organizations, where there are multiple balanced scorecards to report and/or a need for co-ordination of results between balanced scorecards (for example, if one level of reports relies on information collected and reported at a lower level) the use of individual reporters is problematic. Where these conditions apply, organizations use balanced scorecard reporting software to automate the production and distribution of these reports.

Recent surveys have consistently found that roughly one third of organizations used office software to report their balanced scorecard, one third used software developed specifically for their own use, and one third used one of the many commercial packages available.