| ||

ATM usage fees are the fees that many banks and interbank networks charge for the use of their automated teller machines (ATMs). In some cases, these fees are assessed solely for non-members of the bank; in other cases, they apply to all users. Many people oppose these fees because ATMs are actually less costly for banks than withdrawals from human tellers.

Contents

- Australia

- Brazil

- Third party networks

- Canada

- Interac ATMs

- The Exchange

- East Asia

- Japan

- European Union

- Austria

- Finland

- Germany

- Ireland

- Netherlands

- Norway

- Poland

- Portugal

- Spain

- Sweden

- United Kingdom

- Iran

- Hong Kong

- Indonesia

- Malaysia

- Thailand

- Philippines

- Pakistan

- Sri Lanka

- Bangladesh

- India

- Switzerland

- United States

- References

Two types of consumer charges exist: the surcharge and the foreign fee. The surcharge fee may be imposed by the ATM owner (the deployer or independent sales organization) and will be charged to the consumer using the machine. The foreign fee or transaction fee is a fee charged by the card issuer (financial institution, stored value provider) to the consumer for conducting a transaction outside of their network of machines in the case of a financial institution.

Australia

On 3 March 2009 Direct Charging (surcharging) on Australia’s ATM networks was introduced. The Reserve Bank of Australia says this reform will result in benefits to competition and efficiency in the Australian ATM system.

Most banks, (Commonwealth Bank [CBA], ANZ and Westpac/St.George) levy a $2 "ATM service fee" for withdrawals and balance inquiries at their ATMs by non-customers, NAB charges $2.00 (50c for an enquiry), Suncorp $2.20 (80c for an enquiry).

Independent ATM operators contend with highly variable cost bases, volatile transaction volumes, extremely low transaction volumes (compared with a high st bank) and cash floating costs. The only cost recovery method available to an independent ATM operator is the ATM fee. Arguably, the ATM fee represents a low cost payment alternative to the gouging from credit card companies to consumers and merchants.

Bendigo Bank, Bank of Queensland, and Suncorp do not charge any fee to use another bank's ATM. BankWest does not charge users for access to foreign ATMs.

ING Direct Australia reimburse domestic ATM fees provided that customers deposit AU$1000 per month as part of a loyalty program, however do not operate any of their own ATMs. .

Brazil

In Brazil, banks such as Bradesco, Banco do Brasil, Caixa Econômica Federal, Itaú and Santander operate their own nationwide ATM networks. These ATMs can be found in many locations such as the bank branch itself, kiosks spread throughout a city or even supermarkets, gas stations, shopping malls and post offices, making it very convenient for the customer to make withdrawals and check balances without incurring any fees. There are also no denial fees (i.e. when trying to withdrawal more money than what's available in your account) as Brazilian businesses cannot charge for services not rendered. However, fees are assessed if there is excessive usage of the ATMs (i.e. one makes more withdrawals than what's allowed by their monthly maintenance fee). Fees and limits can be checked at the FEBRABAN (the Brazilian Banking Federation) website.

Third-party networks

Brazilian banks have several partnerships in place in order to extend their coverage.

Correspondente bancário (Banking agent)

A partnership with store owners, who then use a small wireless ATM (much like a wireless EFT POS) to process transactions for the bank, such as deposits, payments and withdrawals. Use of a banking agent normally does not generate any fees.

Interbank network

Brazil does not have a national interbank network, but ATMs from some banks are connected to other banks' networks. These are usually indicated in the ATM itself. Use of an interbank network does generate fees.

Cash withdrawal with a Visa debit card

Brazilian acquirer Cielo (formerly known as VisaNet) offers Visa debit card holders an option to withdrawal a small amount of cash (up to R$100, approx. US$30) when paying for merchandise at any Visa-accepting store. Store owners then hand over the money to the customer at the checkout. While the purchase itself generate fees for the business (like any other credit or debit card transaction), the money withdrawal does not, and is reimbursed in full.

Third-party networks

There are third-party ATM networks such as Banco24Horas that charge fees for use. However, some banks (such as Citibank) will reimburse fees for its customers.

Canada

A short description of the fee structure one experiences while using Canadian ATMs can be found at the Interac website, while The Financial Consumer Agency of Canada maintains a chart of the fees typically charged for use of ATMs in Canada.

Interac ATMs

Most Canadian financial institutions are members of the Interac Association, a multi-bank ATM network founded by Royal Bank of Canada, CIBC, Scotiabank, Toronto-Dominion Bank, and Desjardins Group in 1984. Before the presence of white-label ATMs, most Canadian customers were only charged the standard Interac Network Transaction Fee when a customer was using an ATM not provided by the bank that held their account (historically $0.75 CAD, now $1.50 CAD). As the Interac network was opened up to more Independent sales organizations ("ISO")s and the potential for additional revenue from Service Fees were made available, most banks elected to impose the Service Fee in addition to the revenue that was generated from the Interac fee.

The Exchange

The Exchange is a multi-bank ATM network. It originated in the northwestern United States before expanding to Canada in 1983. As of 2012, many Canadian credit unions, along with The Alterna Bank, Alterna Savings, Canadian Western Bank, Citibank, Citizens Bank, HSBC, Manulife Bank of Canada, and National Bank provide surcharge-free ATM access to members of other participating financial institutions through the network.

East Asia

Several East Asian countries charge fees for ATM usage.

Japan

In Japan, usually any ATM offers free withdrawal for its respective account holders. Business weekday from morning to late evening means a free transaction (withdrawal, deposit, balance statements, sometimes bank transfers). Beyond this time limit or even on weekends / public holidays, the ATM charges minimum fees to make a transaction.

European Union

Rules are being introduced that will force banks to levy equal fees for customers of all banks in the European Union. This may mean national fees become higher. See Single Euro Payments Area.

These rules apply since 1 July 2002. Eurozone and Swedish customers are exempt from getting lower international fees outside Eurozone countries, because only fees for euro withdrawals are regulated. Non-Eurozone customers (except Swedish customers) are completely exempt from getting lower international fees, because the regulation only states that international euro withdrawals should be available at the same price as national euro withdrawals (and euro withdrawals are very uncommon in non-Eurozone customers' home countries).

Austria

Cash withdrawals are free for any owner of an Austrian Maestro card at a bank. Some independent ATM's – 67 out of 8,500 as of 2016 – charge a small (1.95 € in 2016) fee. By law a warning is given when a fee is charged. July 2016 it is discussed if a law should forbid these fees or the fee must be displayed clearly during the transaction. (Very few, small banks charge an extra fee when one of their own customers uses a different bank's ATM.)

Finland

Cash withdrawals are free for any owner of a Finnish bank card or Visa Electron cards on ATM brand "Otto." which is the largest ATM network in Finland. There are smaller rivals which have fees. "Otto." ATMs accept also Visa, MasterCard, American Express and Diners Club credit cards. They also belong to Maestro, Cirrus and PLUS networks. Fees depend on card issuer.

Germany

German banks generally charge fees for withdrawals at another bank's ATM, both within the national Girocard debit card/ATM scheme as well as when using a debit card's Maestro or V-Pay facility abroad.

Usual fees for withdrawals within the Girocard scheme are all implemented as surcharges (direktes Kundenentgelt) and starting from 1.95 EUR and can go up to 5 EUR. All ATMs are connected to the national Girocard interbank network. The ATM owners do usually join one of the ATM groups that mutually lower or waive fees, so that customers can withdraw free of charge. The most extensive network of ATMs belongs to the savings banks associations ("Sparkassen") with 24,600 ATMS. Most of the private banks are either member of the Cash Group (7,000 ATMs owned by the major banks) or Cash Pool (2,500 ATMs owned by smaller banks) - they are usually found in city centers. The credit unions ("Volksbanken" and "Raiffeisenbanken") provide around 18,000 ATMs and are associated in the BankCard ServiceNetz, very often in smaller towns and villages, but less frequently available in the big cities.

Some German banks such as Deutsche Kreditbank, ING-DiBa and Consorsbank have started issuing complementary Visa cards for cash withdrawals to their customers, in addition to the traditional Girocard. Those issuing banks will absorb the interbank fee that they are obliged to pay to the ATM operator under Visa regulations. Although the cards use the Visa credit card protocols, the funds are taken directly from a linked bank account just as with debit cards, and there are no cash advance fees. As surcharges for cash withdrawals are uncommon in Germany, almost any ATM in Germany can be used for free cash withdrawals with such a Visa card. This is however not the case of the ATMs of IC Cash, that as of July 2016 charges 6,50 EUR without informing their foreign customers.

Ireland

Section 149 of the Consumer Credit Act 1995 requires a credit institution to notify the Central Bank of Ireland of every proposal to increase a previously notified charge or to impose any charge in relation to the provision of a service to a customer that has not been previously notified to the Central Bank. Not all ATMs are operated by credit institutions. Third party charges are not subject to this notification process. The Government imposes a fee of 12 Cent Stamp Duty per ATM withdraw in the Republic on debit/ATM cards charged at the end of a calendar year and it's capped at €2.50 for cards only used at ATM's and €5.00 for cards used at ATM's and Point of Sales.

Netherlands

Cash withdrawals are usually free for an owner of a Dutch debit card, both within The Netherlands and in other places of the European Union. Cash withdrawals from another bank in The Netherlands is limited to a maximum of once a day and a lower limit per transaction. The one transaction per day limit generally does not apply to withdrawals outside the country. You may withdraw up to 2300 euro per cashpoint.

Norway

No ATM normally surcharges. However most major card issuers will demand cash advance fees, unless the client pays a higher annual fee for the card. Some cards have no ATM fees, but these are the exception - like Skandiabanken VISA and Gebyrfri VISA, both smaller foreign-based banks.

Poland

There are few but extensive independent ATM operators in Poland (e.g. Euronet, ITCARD owner of Planet Cash ATM network, eCard, Global Cash) as well as smaller bank-owned networks. Fees depend on inter-bank agreements and are explicitly stated in card contract. Typically withdrawals from own and allied networks are free while from competitor's machines are subject to percentage (3-4%) with constant minimum fee, e.g. 5 PLN (~$1.4). Premium accounts often come without any withdrawal fees, albeit at higher recurring cost. As of 2010 many banks offer optional contracts on "free" withdrawals from any ATM at flat monthly fee, usually priced similar to 1 withdrawal. The maximum amount you can withdraw in one operation is usually 30 or 40 notes (~$1,000), varying depending on the type of machine, ATM management system and banknote denominations used.

Portugal

All Multibanco withdrawals and payments in Portugal are free. Recent European Union directives allowed merchants and banks to charge the customers for transactions, but the government approved a law that forbids charging any kind of fees. Left Bloc and Portuguese Communist Party were the political parties that came up with the proposal and the ones more devoted to the idea.

Spain

There are significant variation in charges applied. A card issued by a Spanish Bank will normally expect to incurr a moderate fee from 0 to 1Euro to be applied to ATM withdrawals, where the transaction is conducted on an ATM operated and owned by the customers own bank. However outside this situation there is anecdotal evidence of significantly higher charges being applied where third party owner/operated ATMs are used, including those operated/owned by other Spanish banks. These may be in reported but unverified cases to be as high as 5+% of the value withdrawn. An effort is currently being made to research, identify and quantify the structure and nature of what from this anecdotal evidence, appear in some cases to be excessive charges. The case is complicated because the fees can originate from the ATM operator, or/and the customers own bank, for as "processing fees".

Sweden

In Sweden, most banks issue debit cards for an annual or monthly fee which includes free withdrawals in Sweden and within the eurozone. However, customers are subject to a fee if using a cash machine elsewhere. Some cards from some banks are, however, subject to fees also when used in the eurozone and some Swedish cash machines. Most of these cards are issued by savings banks.

United Kingdom

During the 1980s the number of banks and building societies charging issuer fees (i.e. charging fees to their own customers when they used another ATM operator's ATMs), gradually increased. However, in 1990 Barclays announced they were introducing an acquire fee for all non-Barclays card-holders at their ATMs. This would result in "double charging", where the customer was charged by both their card issuer and the ATM operator. Public reaction against this proposal was very strong and a campaign launched by Nationwide Building Society and the UK tabloid newspapers resulted in issuer fees being removed altogether.

Interchange, the fee which a card issuer pays to the ATM operator to cover the cost of the transaction remains and this cost is absorbed by the card issuer.

In 1999 LINK, the UK ATM network opened membership to so called independent ATM operators, ("IADs"); organisations which do not issue cards. IADs initially focussed on the pay-to-use market, where the customer covers the cost of the transaction directly and this, coupled with a low-cost business model, meant that the number of pay-to-use ATMs rose rapidly, peaking in 2007 at just over 27,000 ATMs.

Most of these machines are in low footfall locations such as convenience stores, garages, nightclubs and pubs. The fee charged in 2005 was usually between £1.00 and £1.50, but occasionally they have been known to charge up to £5 and £10.

Rules regarding signage on pay-to-use machines were introduced in 2005 and enhanced in 2006 and since 2007 the number of pay-to-use cash machines has fallen, by the end of 2010 there were around 21,000.

The large numbers of free-to-use ATMs and the low average number of transactions at pay-to-use ATMs means that 97% of cash withdrawals in the UK remain free of charge. As of 2016, there were about 54,000 free to use ATMs, of which 23,600 were provided by independent suppliers, and 16,000 ATMs that charge for withdrawals.

Iran

The Shetab (Interbank Information Transfer Network) system is an electronic banking clearance and automated payments system used in Iran. The system was introduced in 2002 with the intention of creating a uniform backbone for the Iranian banking system to handle ATM, POS and other card-based transactions. There are no charges for money withdrawal in this network. Transferring money between two accounts in a same bank is free but between different banks costs from 5,000 to 9,000 (for amounts of 50,000 to 30,000,000) per day, and checking the account balance costs IRR 1000 for other banks' cards. Other services are currently free.

Hong Kong

There are three ATM networks in Hong Kong: ETC (HSBC and Hang Seng Bank only), JETCO (all remaining banks) and AEON. ATM use is free of charge, except when a card is used outside of its respective home network. When a card is used outside the home network, HKD$15–30 is paid for service charge.

Indonesia

In Indonesia, banks generally do not charge a fee for ATM usage. However, when an ATM card is used outside the home ATM network, service charge will apply.

Malaysia

In Malaysia, ATM usage is free of charge* but users maybe required to pay a fee when used outside the home network and banks charge a fee of RM 8 - RM 24 annually for a normal savings account, under Malaysia's Basic Saving Account scheme the fee is waived but the customer is limited to only 8 free cash withdrawals, after that, banks will charge a fee of RM0.53 (Including GST) for every withdrawal until the following month. Also, under Malaysian Electronic Payment System (MEPS), users can withdraw cash from participating banks for a fee of RM 1.06 (Including GST) per withdraw. Users can also transfer their fund to another bank via IBFT (Instant Bank Fund Transfer) at a fee of RM 0.32 - RM 0.53 or via IBG (Inter-bank GIRO) at RM 0.11 . Another program called HOUSe by locally incorporated foreign banks in Malaysia also have their own network for cash withdrawals from participating banks. Users of local banks are also considered MEPS users by default and users of locally incorporated foreign banks are considered HOUSe users. MEPS users attempting to withdraw cash from HOUSe networks are subjected to a fee of RM 4 and vice versa. Some banks allow cross-border cash withdrawals, but may charge a fee of up to RM 24 (excluding GST) per withdrawal, depending on the kind of ATM network users choose.

Thailand

In Thailand, there is no fee for domestic same-bank same-province transaction. However, customers usually pay for ATM annual fee of THB200, one-off card fee of THB100 and convenience fee for withdrawal or balance inquiry at other bank ATM or at a province other than the province where the account is opened. On September 23, 2010, Bank of Thailand (BOT) has announced ATM fee ceiling framework which came into full effect one year later. Most of the banks will allow customer to have four withdrawal or balance inquiry transactions for free provided that the ATM is located in the same province with the account, then charges up to THB10 per transaction for interbank same-province ATM usage. Inter-provincial fund transfer or withdrawal fees are capped at THB20 per transaction as a result of BOT 2010 reform. However, Banks are now pushing for high annual fee card by combining personal assurance (PA) into their cards. The annual fee of PA card can be more than three times for the ordinary card (typically THB200 for a debit card). Many customers are often told that basic cards have run out off stock and they can only choose the PA card. In some cases, customers are not allowed to open an account if he or she is not willing to subscribe to ATM service and pay the card fees.

For a foreign card, the ATM service fee is 150 to 200 THB, depending on the bank.

Philippines

In the Philippines, there is a PHP 300 (Philippine peso) charge from local banks when using an international ATM card, in addition to the originating bank's charges. HSBC Bank is the only bank in the Philippines without a PHP 200 fee for oversea bank cards.

Pakistan

In Pakistan banks usually charge a fee of PKR 0 to PKR 20 per non user's ATM cash withdrawal. These fees are levied chiefly to offset banks' own costs at par only, without any profit margin whatsoever. There are two ATM switches operational in the country, 1LINK, hosted by a consortium of banks, and MNET, hosted by MCB Bank Ltd; and all Pakistani banks are members of one or the other switch as per the mandate of the State Bank of Pakistan, the country's central bank. Some banks, like Allied Bank and HSBC (now operating as Meezan Bank), absorb the costs entirely, and offer their customers totally free withdrawals at all ATMs countrywide, including Azad Jammu and Kashmir; a territory between Pakistan and India whose status is disputed.

Sri Lanka

In Sri Lanka banks usually charge a fee of LKR 5.00 (US$0.04) for the user's of the bank (which provides the ATM) and LKR 15.00 (US$0.11) to LKR 60.00 (US$0.44) per non user's bank withdrawal of cash from the machine. Most ATMs are connected to the national LankaPay interbank network. If the user used their credit card to withdraw money, banks will charge from LKR 300.00 (US$2.21) to LKR 900.00 (US$6.62) per transaction.

Bangladesh

There are multiple ATM networks in Bangladesh. Dutch-Bangla Bank has the largest ATM network and also the most member banks. Dutch-Bangla Bank customers are charged BDT 200 yearly as ATM network charge if one has any debit card of the bank.

Dutch-Bangla Bank has separate agreements with local and international banks whereby Dutch-Bangla Bank charges BDT 10 (USD 0.085) per transaction to member banks. Due to this low amount, member banks often add an extra amount as profit margin.

India

In 2014, the Reserve Bank of India (RBI), India's central bank and financial regulator, issued a directive on request from large ATM network and card-issuing banks which expressed concern about the growing cost of ATM network operations, large cash outflows, and other problems. In fact, customers of same bank withdrawing more than 5 times in month were sought to be charged. Present directive reduces Free transaction per month from as five to three with revised charges of INR 20 plus taxes levied per transaction as ATM transaction fee.

The number of ATMs, which stood at a little over 27,000 as at end-March 2007, has increased to over 160,000 across the country by end-March 2014. During the same period, POS infrastructure has increased from 330,000 to 1,065,000 terminals. Meanwhile, White Label ATMs (WLAs) have also been introduced in the country with the objective of increasing the ATM density and also building the rural and semi-urban ATM infrastructure.

In 2007, the Reserve Bank of India (RBI), the country's central bank, had issued a directive to all commercial banks to freeze ATM charges and, with effect from 1 April 2009, abolish ATM service charges altogether. Since 2009, customers of any licensed bank are able to use the ATMs of other banks without paying a service charge. Earlier, banks charged between ₹ 10 and ₹ 35 per reciprocal transaction.Today a person holding card of other banks can withdraw amount from other bank ATM's but the number of transactions is limited to 5; after 5th i.e. 6th transaction forward the person would be charged up to ₹ 20.

However, banks can still surcharge for items such as credit card ATM cash advances and at foreign ATMs. In addition, RBI imposes significant foreign exchange restrictions on the use of Indian debit VISA/MasterCard abroad. For example, Indian debit VISA cards are routinely marked "Valid in India and Nepal only" due to the country's restrictive foreign exchange reserve policy.

Switzerland

Fees are not usually charged for withdrawals at a banks' own ATMs, but may be at those of other banks. For example, at the time of writing UBS do not charge for withdrawals at other banks whereas Credit Suisse charge 2 CHF per withdrawal. Sometimes, banks provide the cardholder with 10, 12 or 24 free withdrawals, especially if the bank is a small one, with few ATMs. Most Swiss banks hand out Maestro cards to their customers, in most cases for an annual fee of around 40 CHF, so that any ATM can be used.

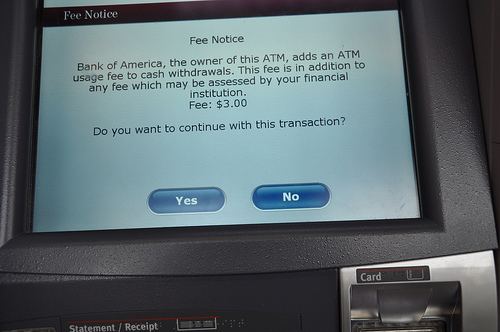

United States

Prior to 1988, there was no surcharging of cardholders by ATM owners in the U.S. In 1988 Valley Bank of Nevada began surcharging "foreign cardholders" (meaning holders of ATM cards not issued by Valley Bank) for withdrawals at Valley Bank ATMs located in/near Las Vegas casinos. Eventually, various regional ATM Networks, and ultimately the national networks, Plus and Cirrus, permitted ATM surcharging.

Before 1996, foreign ATM fees averaged $1.01 USD nationally, according to a 2001 report from the US-based State Public Interest Research Group.

As banks and third parties realized the profit potential, they raised the fees. ATM fees now commonly reach $3.00, and can be as high as $6.00, or even higher in cash-intensive places like bars and casinos. In cases where fees are paid both to the bank (for using a "foreign" ATM) and the ATM owner (the so-called "surcharge") total withdrawal fees could potentially reach $11. Independent sales organizations ("ISO"s) are the driving force in ATM deployment in the U.S. today representing over 60% of the 396,000 ATMs nationwide. Some have expressed concerns that the U.S. market is becoming too saturated, spreading the resulting fee pool too thin, which may result in a future net decrease in the number of machines. Other media reports indicate that growth in ATM usage has decreased, possibly in relation to the amount of fees imposed by banks.

According to Bank Call Reports, JPMorgan Chase, Bank of America and Wells Fargo earned more than $1.1 billion in 2016 from ATM fees. The average fee for using an out-of-network ATM has reached $4.57 in 2016 and this is the 10th straight year of increases, according to Bankrate.

A new charge that has come into the marketplace is the "Denial Fee", where a customer is charged a fee for attempting to withdraw more money than they are either allowed through their daily withdrawal limit or by having insufficient funds in their account.