FUNDAMENTALS OF FINANCIAL ACCOUNTING

Objectives

To develop conceptual understanding of fundamentals of financial accounting system and to impart skills in accounting for various kinds of business transactions.

Introduction

Meaning of Book Keeping and Accountancy

Bookkeeping, in business, is the recording of financial transactions, and is part of the process of accounting. Transactions include purchases, sales, receipts and payments by an individual or organization. The accountant creates reports from the recorded financial transactions recorded by the bookkeeper and files forms with government agencies. There are some common methods of bookkeeping such as the single-entry bookkeeping system and the double-entry bookkeeping system. But while these systems may be seen as "real" bookkeeping, any process that involves the recording of financial transactions is a bookkeeping process.

Bookkeeping is usually performed by a bookkeeper. A bookkeeper (or book-keeper), also known as an accounting clerk or accounting technician, is a person who records the day-to-day financial transactions of an organization. A bookkeeper is usually responsible for writing the "daybooks". The daybooks consist of purchases, sales, receipts, and payments. The bookkeeper is responsible for ensuring all transactions are recorded in the correct day book, suppliers ledger, customer ledger and general ledger.

The bookkeeper brings the books to the trial balance stage. An accountant may prepare the income statement and balance sheet using the trial balance and ledgers prepared by the bookkeeper.

Definition of Accounting

The systematic and comprehensive recording of financial transactions pertaining to a business. Accounting also refers to the process of summarizing, analyzing and reporting these transactions. The financial statements that summarize a large companys operations, financial position and cash flows over a particular period are a concise summary of hundreds of thousands of financial transactions it may have entered into over this period. Accounting is one of the key functions for almost any business; it may be handled by a bookkeeper and accountant at small firms or by sizable finance departments with dozens of employees at larger companies.

Accountancy is the process of communicating financial information about a business entity to users such as shareholders and managers.The communication is generally in the form of financial statements that show in money terms the economic resources under the control of management; the art lies in selecting the information that is relevant to the user and is reliable.Accountancy is a branch of mathematical science that is useful in discovering the causes of success and failure in business. The principles of accountancy are applied to business entities in three divisions of practical art, named accounting, bookkeeping, and auditing.

Types and rules of debit and credit

Under the double entry system, every financial transactions of a business has a double effect. That is, each transaction involves at least two accounts. One aspect of the transaction is debited in an account and the other credited in another account. The debiting and crediting of the accounts are done on the basis of certain rules. These rules are called rules of journalizing i.e debit and credit. There are two alternative bases for the rules of debit and credit such as follows.

1. Rules Of Debit And Credit Based On The Types Of Account

2. Rules Of Debit And credit Based On The Accounting Equation

1. Rules Of Debit And Credit Based On The Types Of Account

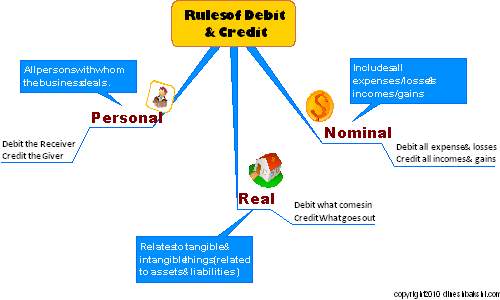

Under double-entry system an account is classified into three types. They are personal account, real account and nominal account. For each of these types of account, there are three separate rules of debiting and crediting the financial transactions. The rules of debit and credit under different types of account are as follows.

A. Personal Account

Personal account is a account of a person. A person can be a natural person such as people like us, an artificial person such as firms, organizations and institutions and a representative person such as debtors and creditors. Since a person, be it a natural, artificial or representative, can be the receiver of benefits or giver of benefits, the rule of debiting and crediting the account of the person is as follows:

* Debit the receiver of benefits

* Credit the giver of benefits

This rule states that whenever a person receives benefits is debited by the amount of the benefit received. On the contrary, whenever the person gives the benefits is credited by the amount of benefits given. For example, if cash is paid to Michael (Michael is a natural person), his account (Michaels account) is debited since he is the receiver of the benefit (cash). If cash is received from City Enterprises (City Enterprises is an artificial person), its account (City enterprises account) is credited because it is the giver of benefits (cash).

B. Real Account

Real account is a record of an asset. An asset can be current asset such as cash, a fixed asset such as building and intangible asset such as goodwill. Since an asset, is a current, fixed or an intangible asset , can either come in the business through its purchase or go out of the business through its sales, the rule of debiting and crediting the real (asset) account is as follows:

* Debit what comes in

* Credit what goes out

This rule states that whenever some benefit in the form of asset come into the business through its purchase, its (asset) account is debited. Conversely, whenever some benefit in the form of asset goes out of the business through its sales, its (asset) account is credited. For example, if cash is invested in the business, cash (current asset) account is debited by the amount of cash. If furniture is purchased for cash, furniture (fixed asset) account is debited because it comes into and cash (current asset) account is credited because it goes out from the business in exchange for furniture.

C. Nominal Account

Nominal account is a record of expense or loss or income or gain. An expense or loss is the sacrifice of benefits in exchange for service used and an income or gain is the benefit earned in exchange for service rendered. Since the business makes expenses and earns incomes, the rule of debiting and crediting the expense and income (nominal) account is as follows:

* Debit all expenses and losses

* Credit all incomes and gains

This rule states that whenever some benefit is sacrificed in exchange for service used ( expense made or loss suffered), its (expense) account is debited. On other hand, whenever some benefit is earned in exchange for service rendered, its (income or gain) account is credited. For example, when salary is paid, an expense is made by the business, therefore salary account is debited. On the other hand , when interest is received, an income is earned by the business, hence, interest received account is credited.

2. Rules Of Debit And Credit Based On The Accounting Equation

Accounting equation is a statement of equality between the three basic elements of accounting. They are assets, capital and liabilities. Each and every financial transaction affects the three basic elements. However, the total of all assets is always equal to the total of capital and liabilities at any point in time.

Accounting Concepts and Conventions

Accounting concepts and conventions evolved as a result of information needed by the users of accounting information which became conflicting over time because of different methodology or procedure used in its preparation .it was thereby adopted to ensure that accounting information is presented accurately and consistently.

Accounting concepts and conventions could be defined as ground or laid down rules of accounting that should be followed in preparation of all accounts and financial statements.

There are different kinds of accounting concepts and conventions

The concepts include

i. GOING CONCERN CONCEPT

Giving the fact that a business entity is solvent and viable this concept assumes the notion that the business unit will have a perpetual existence and will not be sold or liquidated

IT’S IMPORTANCE

It supports the use of historical cost concept in measuring assets such as; supplies equipments etc. that will be used in operation of a business. Without the Going concern concept accounts will be drawn up on a winding up basis.

ii. ENTITY CONCEPT

This concept states that every business unit not withstanding its legal existence is treated a separate entity from the body or bodies that owe it, this implies that its existence is distinct from its owner(s).

IT’S IMPORTANCE

It records and reflects the financial activity of the specific business organization and not of its owner(s) or employees. It is also important because it ensures that a company and its owner(s) can contract and sue each other incase of any misunderstanding arising in the future.

iii. MATCHING OR ACCURAL CONCEPT

This concept states that in an accounting period the earned income and the incurred cost which earned the income should be properly matched and reported for the period. This concept is also universally accepted in Manufacturing, Trading organization.

IT’S IMPORTANCANCE

Accrual concept attempt to correctly match all the accounting expenses (cost) to income (revenue) to the time it occurs at that accounting period. It also enables all revenue and expenditure of an accounting period to be recognized. It helps specify the profit of the organization in the accounting period.

iv. REALISATION CONCEPT

Realization concept encourages the periodic recognition of revenue as soon as it can be measured and the value of the assets is reasonably certain

In realization the revenue are realized in three basis

1. Basis of cash

2. Basis of sale

3. Basis of production.

ITS importance

It encourages the recognition of transaction and profit arising from them at the point of sale or transfer of ownership

v. HISTORICAL COST CONCEPT

This concept implies that all assets acquired, service rendered or received, expenses incurred etc. should be recorded in the books at the price at which it was acquired

(It’s cost price). The cost is distinct from its value and the record does not signify the value. It also holds that cost is the most reliable and verifiable value at which a good is or services should be initially recognized.

ITS importance

It allows the record of all transaction no matter how minute it may be before it might or might not be subjected to depreciation.

vi. DUAL ASPECT CONCEPT

This concept ensures that transaction are recorded in books at least in two accounts, if one account is debited it’s also credited with the same amount in a different account. The recording system is also known as double entry system. Assets = Liabilities + Capital.

vii. MONEY MEASUREMENT CONCEPT

This concept states that an item should not be recorded unless it can be quantified in monetary terms in other words it specifies that accountants should not record facts that are not expressed in money terms.

ITS importance

This concept could be said to be efficient because money enables various things of diverse nature to be added together and dealt with.

THE VARIOUS KINDS OF CONVENTION INCLUDE

i. CONSISTENCY: It states that accounting method used in one accounting period should be the same as the method used for events or transactions which are materially similar in other period (i.e. accounting practices should remain unchanged from period to period ). This also involves treatment of transaction and valuation method. Consistency is also advisable so that the comparison of accounting figures over time is meaningful. Consistency also states that if a change becomes necessary, the change and its effect should be clearly stated.

ITS importance

As stated by D.VICTOR consistency in accounting is an important assumption that facilitates comparability for information users. It also encourages reliability and fair presentation.

ii. MATERIALITY

According to AMERICAN ACCOUNITNG ASSOCIATION, an item should be regarded as material if there is reason to believe that knowledge of it would influence decision of informed investors. An item is also considered material if its omission or misstatement could distort the financial statement such that it influences the economic decision of users taken on the basis of financial statement.

ITS importance

It helps prevent records to be unnecessarily being over burden with minute details.

iii. PRUDENCE OR CONSERVATISM

This is an accounting practice that emphasizes great care in the anticipation of possible gains while possible losses are efficiently provided for. Prudence requires an accountant to attempt to ensure that the degree of success is not overstated. It also makes provision for possible bad and doubtful debts out of current year’s profit.

ITS importance

A strict application of prudence convention would ensure that profits and assets of the firm are not overstated.

iv. OBJECTIVITY

This convention states that the financial statement should be made on verifiable evidence.

ITS importance

It gives proof of a transaction in an objective manner in contrast to subjectivity or dependence on the verifiable opinion o the accountant preparing the financial statement.

v. DISCLOSURE

It states that information relating to the economic affairs of the enterprise which are of material interest should be clearly disclosed to the readers.

ITS importance

it discloses sufficient information which is of material in trust to owners,present and potential creditors and investors. It also helps the reader not to be misled in anyway by hearsay.

Ledger balance

The balance of a customer account as shown on the bank statement. The ledger balance is found by subtracting the total number of debits from the total number of credits for a given accounting period. The ledger balance is used solely in the reconciliation of book balances.

The ledger balance should not be confused with the customers available balance, which is the amount of funds available for withdrawal. The ledger balance includes any and all checks outstanding that have not yet cleared the account. This is partly why it differs from the available balance.

Trial balance

A trial balance is a list of all the General ledger accounts (both revenue and capital) contained in the ledger of a business. This list will contain the name of the nominal ledger account and the value of that nominal ledger account. The value of the nominal ledger will hold either a debit balance value or a credit balance value. The debit balance values will be listed in the debit column of the trial balance and the credit value balance will be listed in the credit column. The profit and loss statement and balance sheet and other financial reports can then be produced using the ledger accounts listed on the trial balance.

The name comes from the purpose of a trial balance which is to prove that the value of all the debit value balances equal the total of all the credit value balances. Trialing, by listing every nominal ledger balance, ensures accurate reporting of the nominal ledgers for use in financial reporting of a businesss performance. If the total of the debit column does not equal the total value of the credit column then this would show that there is an error in the nominal ledger accounts. This error must be found before a profit and loss statement and balance sheet can be produced.

The trial balance is usually prepared by a bookkeeper or accountant who has used daybooks to record financial transactions and then post them to the nominal ledgers and personal ledger accounts. The trial balance is a part of the double-entry bookkeeping system and uses the classic T account format for presenting values.

Rectification of Errors

In financial accounting, every single event occurring in monetary terms is recorded. Sometimes, it just so happens that some events are either not recorded or it is recorded in the wrong head of account or wrong figure is recorded in the correct head of account.

Whatever the reason may be, there is always a chance of error in the books of accounts. These errors in accounting require rectification. The procedure adopted to rectify errors in financial accounting is called "Rectification of error".

HOW TO RECTIFY THESE ERRORS

One way of rectification is that we can simply erase or overwrite the incorrect entry and replace it with the correct one. But this practice is not allowed in accounting. We have to Rectify / correct the mistake by recording another entry.

TYPES OF ERRORS

Before going to the rectification process, lets first see the different kinds of errors that can appear in our books of accounts:

ERROR OF OMISSION

One of the most common errors is that an event escapes recording. This means that an event occurred but we did not record it. For example, we discussed about bank charges being deducted by banks without our knowledge or our payments made by banks on our standing orders etc. There can be other reasons as well. Such errors are called ERRORS OF OMISSION.

ERROR OF COMMISSION

Then, there is a chance that the event is classified and recorded correctly but within wrong classification of account. For example, a payment to Mr. A, who is a debtor, is recorded in the account of Mr. B, who is also a debtor. Now the classification is correct but entry is posted in the wrong account. Such errors are called ERRORS OF COMMISSION.

ERROR OF PRINCIPLE

Then there are errors in which an entry is recorded in the wrong class of account. For example a purchase of fixed asset, say, a vehicle is recorded in an expense account. These errors are called ERRORS OF PRINCIPLE.

ERROR OF ORIGINAL ENTRY

The errors in which recording is in correct account but the figure is incorrect are called ERRORS OF ORIGINAL ENTRY. For example, a receipt of Rs. 50,000 from a debtor is recorded as Rs. 5,000 in his account.

Bank Reconciliation Statement

A Bank reconciliation is a process that explains the difference between the bank balance shown in an organisations bank statement, as supplied by the bank, and the corresponding amount shown in the organizations own accounting records at a particular point in time.

Such differences may occur, for example, because a cheque or a list of cheques issued by the organization has not been presented to the bank, a banking transaction, such as a credit received, or a charge made by the bank, has not yet been recorded in the organisations books, or either the bank or the organization itself has made an error.

It may be easy to reconcile the difference by looking at very recent transactions in either the bank statement or the organisations own accounting records (cash book) and seeing if some combination of them tallies with the difference to be explained. Otherwise it may be necessary to go through and match every single transaction in both sets of records since the last reconciliation, and see what transactions remain unmatched. The necessary adjustments should then be made in the cash book, or any timing differences recorded to assist with future reconciliations.

For this reason, and to minimise the amount of work involved, it is good practice to carry out such reconciliations at reasonably frequent intervals. Reconciliations are generally performed by specialised accounting software though the understanding of what occurs is important for a successful reconciliation. Also, Bank reconciliation statement is a statement prepared on a particular day to reconcile the bank balance as per Cash book or Bank statement showing entries causing difference between the two balances.

Cause of difference between cash book and pass book

Bank reconciliation means some of the transaction entered in the cash book not in the pass book and some transaction entered in the pass book not in the cash book. In other words we can say that always opposite entry in cash book and pass book. The bank pass book indicates the amount paid into the bank and the amount withdrawn there form. The pass book balance or any given data must be the same as the balance shown by the bank column of the cash book on the same date.The reason responsible for the difference may be delay in intimation, time gap between recordings of transaction in cash book and pass book due to errors and omissions in cash book and pass book.

Reasons of difference between cash book & pass book balance:

1. Cheque issued but not presented for payment: When cheque are issued then immediately make entry in the cash book. The cheque issued can be presented for payment to the bank within six month from the date of cheque as per banking law. The cheque are presented for payment after the expiry of the above period then payment is refused by the bank. This cheque is also known as stale cheque. It is posssible at the time when the balance of the two books are being compared, thus more chances of causing a disagreement b/w the two balances.

2. Cheque paid into the bank but not yet cleared: As soon as the cheque are deposited into the bank, the immediately entry is passed in the cash book. This will make entry in pass book only when cheque are cleared. It is posssible at the time when the balance of the two books are being compared, thus more chances of causing a disagreement b/w the two balances.

3. Interst allowed by the bank: Bank might have credited the account of the customer with the interest and may have made the entry in the pass book. It is possible that the entry of such interest may not have been made by the customer in the cash book, thus causing a disagreement b/w the two balances.

4. Interest and Bank charges debited by bank: Sometime bank charges interest from the customer then immediately entry in the pass book but not in cash book. so, in this case when check the balance b/w cash and bank book then disagreement b/w the two balances. So, it is the main reason to create difference b/w two books.

5. Interst, dividend collected by the bank: sometime interest on government security or dividend on share is collected by the bank and is credited to customer account. If the entry does not appear in the cash book then balance will differ.

6. Direct payment by bank: Sometimes, understanding instruction from the clients certain payment like insurance premium, club fees instalment etc. are made by the bank. then this entry is recorded only in the pass book. This entry is made in the cash book only when the necessary intimation to that effect is received from the bank by the client. The entries in the cash and pass book may be on different dates.

7. Direct payment into the bank by a customer: Sometimes, our customer deposit money direct into the account in the bank. It is only recorded in the pass book not in the cash book. It is posssible at the time when the balance of the two books are being compared, thus more chances of causing a disagreement b/w the two balances.

8. Dishonour of bill discounted with the bank: Sometimes, customer get their bills discounted with the bank. If the bank is not able to get payment of these bills on the due date. it will debit the customer account with the amount of the bills together with the nothing charges if any.The customer will pass the entry in the cash book only. when balance of the two books are being compared, thus more chances of causing a disagreement b/w the two balances.

9. Dishonour of cheque: When the received cheque are deposited into bank, these are immediately recorded in the cash book. As a result cash book balance is increased. but the deposited cheque is dishonoured due to lack of funds or due to other reasons. Bank doesnot credit the amount of the depositor. as a result disagreement b/w the two balances.

10. Error and ommissions: If any error is committed either by the bank or by a customer in the cash book While recording a transaction in their respective books, it causing a disagreement b/w the two balances. the error may be:

a) undercast/overcast of receipt side or payment side.

b) bank charges omitted from the banks or recorded twice in the books.

c) wrong carry forward of cash book balance.

Final Accounts of Sole Trader

Sole traders are people who are in business on their own: they run shops, factories, farms, garages, local franchises, etc. The businesses are generally small because the owner usually has a limited amount of capital to invest. Profits are often small and, after the owner has taken out drawings, are usually ploughed back into the business.

The final accounts (or financial statements) of a sole trader comprise:

a trading and profit and loss account which shows the profit or loss of the business a balance sheet, which shows the assets and liabilities of the business together with the owner’s capital These final accounts can be produced more often than once a year in order to give information to the owner on how the business is progressing. However, it is customary to produce annual accounts for the benefit of the Inland Revenue, bank manager and other interested parties. In this way the trading and profit and loss account covers an accounting period of a financial year (which can end at any date – it doesn’t have to be the calendar year), and the balance sheet shows the state of the business at the end of the accounting period.

Departmental Accounts

Departmental accounts are associated with a department rather than just an individual. Even if the owner of a departmental account leaves the university or transfers to a different department the account will remain active. Our goal is to make it easier for a department to retain accounts and just transfer ownership when the need arises. At the same time, we will always know who the current owner is if we need a contact for a departmental resource.

Modern life is very mechanical specially in big cities. The citizens of such cities expect all the goods and services just under a single roof. Contemplating the need of the consumers, the business men are also providing the expected service to the consumer just under a roof by opening large scale departmental stores. The departmental stores are the example of large scale retail selling just under a single roof. Different departments are involved for different goods to be sold out. To calculate the net result of the whole organization, a full fledged trading and profit and loss account is to be prepared. But to evaluate individual department, it will be credit worthy to prepare individual trading and profit and loss account. Such individual accounts will help to evaluate and control the different departments.

Objectives Of Departmental Accounting

The main objectives of departmental accounting are:

1. to check out interdepartmental performance

2. To evaluate the performance of the department with previous period result.

3. To help the owner for formulating right policy for future.

4. To assist the management for making decision to drop or add a department

5. To provide detail information of the entire organization

6. To assist management for cost control

A business entity where diversified natures of economic activities are undertaken is split into number of departments for accounting purposes. Generally it is management who will decide the number of departments in which the whole business is to be divided, but the criteria for identifying the departments in an examination question is always the separate sales/work-done revenue. Each department is considered as a profit centre, though none of the departments is separated geographically from the rest of the departments. This type of organizational subdivision creates a need for internal information about the operating results (profitability) of each department. Based upon the departmental knowledge of profitability and growth rate the management takes certain decisions e.g. pricing, costing, sales promotion, closure etc.

Allocation of Incomes and Expenses

Until unless the size of the business entity is very large, the entire book keeping system for the entity is kept by a central accounts department along with some departmental specific records e.g. sales, purchases, stocks and staff salaries etc. Rest of the operating expenses and other incomes need to be allocated among the departments based on their nature, utility, economic benefits and belongingness.

For allocation and division purposes the expenses/incomes can be categorized as:

1. Separately identified

2. Obvious just ratio

3. Specific ratio/sales ratio

4. Un-allocable

Objectives

To develop conceptual understanding of fundamentals of financial accounting system and to impart skills in accounting for various kinds of business transactions.

Introduction

Meaning of Book Keeping and Accountancy

Bookkeeping, in business, is the recording of financial transactions, and is part of the process of accounting. Transactions include purchases, sales, receipts and payments by an individual or organization. The accountant creates reports from the recorded financial transactions recorded by the bookkeeper and files forms with government agencies. There are some common methods of bookkeeping such as the single-entry bookkeeping system and the double-entry bookkeeping system. But while these systems may be seen as "real" bookkeeping, any process that involves the recording of financial transactions is a bookkeeping process.

Bookkeeping is usually performed by a bookkeeper. A bookkeeper (or book-keeper), also known as an accounting clerk or accounting technician, is a person who records the day-to-day financial transactions of an organization. A bookkeeper is usually responsible for writing the "daybooks". The daybooks consist of purchases, sales, receipts, and payments. The bookkeeper is responsible for ensuring all transactions are recorded in the correct day book, suppliers ledger, customer ledger and general ledger.

The bookkeeper brings the books to the trial balance stage. An accountant may prepare the income statement and balance sheet using the trial balance and ledgers prepared by the bookkeeper.

Definition of Accounting

The systematic and comprehensive recording of financial transactions pertaining to a business. Accounting also refers to the process of summarizing, analyzing and reporting these transactions. The financial statements that summarize a large companys operations, financial position and cash flows over a particular period are a concise summary of hundreds of thousands of financial transactions it may have entered into over this period. Accounting is one of the key functions for almost any business; it may be handled by a bookkeeper and accountant at small firms or by sizable finance departments with dozens of employees at larger companies.

Accountancy is the process of communicating financial information about a business entity to users such as shareholders and managers.The communication is generally in the form of financial statements that show in money terms the economic resources under the control of management; the art lies in selecting the information that is relevant to the user and is reliable.Accountancy is a branch of mathematical science that is useful in discovering the causes of success and failure in business. The principles of accountancy are applied to business entities in three divisions of practical art, named accounting, bookkeeping, and auditing.

Types and rules of debit and credit

Under the double entry system, every financial transactions of a business has a double effect. That is, each transaction involves at least two accounts. One aspect of the transaction is debited in an account and the other credited in another account. The debiting and crediting of the accounts are done on the basis of certain rules. These rules are called rules of journalizing i.e debit and credit. There are two alternative bases for the rules of debit and credit such as follows.

1. Rules Of Debit And Credit Based On The Types Of Account

2. Rules Of Debit And credit Based On The Accounting Equation

1. Rules Of Debit And Credit Based On The Types Of Account

Under double-entry system an account is classified into three types. They are personal account, real account and nominal account. For each of these types of account, there are three separate rules of debiting and crediting the financial transactions. The rules of debit and credit under different types of account are as follows.

A. Personal Account

Personal account is a account of a person. A person can be a natural person such as people like us, an artificial person such as firms, organizations and institutions and a representative person such as debtors and creditors. Since a person, be it a natural, artificial or representative, can be the receiver of benefits or giver of benefits, the rule of debiting and crediting the account of the person is as follows:

* Debit the receiver of benefits

* Credit the giver of benefits

This rule states that whenever a person receives benefits is debited by the amount of the benefit received. On the contrary, whenever the person gives the benefits is credited by the amount of benefits given. For example, if cash is paid to Michael (Michael is a natural person), his account (Michaels account) is debited since he is the receiver of the benefit (cash). If cash is received from City Enterprises (City Enterprises is an artificial person), its account (City enterprises account) is credited because it is the giver of benefits (cash).

B. Real Account

Real account is a record of an asset. An asset can be current asset such as cash, a fixed asset such as building and intangible asset such as goodwill. Since an asset, is a current, fixed or an intangible asset , can either come in the business through its purchase or go out of the business through its sales, the rule of debiting and crediting the real (asset) account is as follows:

* Debit what comes in

* Credit what goes out

This rule states that whenever some benefit in the form of asset come into the business through its purchase, its (asset) account is debited. Conversely, whenever some benefit in the form of asset goes out of the business through its sales, its (asset) account is credited. For example, if cash is invested in the business, cash (current asset) account is debited by the amount of cash. If furniture is purchased for cash, furniture (fixed asset) account is debited because it comes into and cash (current asset) account is credited because it goes out from the business in exchange for furniture.

C. Nominal Account

Nominal account is a record of expense or loss or income or gain. An expense or loss is the sacrifice of benefits in exchange for service used and an income or gain is the benefit earned in exchange for service rendered. Since the business makes expenses and earns incomes, the rule of debiting and crediting the expense and income (nominal) account is as follows:

* Debit all expenses and losses

* Credit all incomes and gains

This rule states that whenever some benefit is sacrificed in exchange for service used ( expense made or loss suffered), its (expense) account is debited. On other hand, whenever some benefit is earned in exchange for service rendered, its (income or gain) account is credited. For example, when salary is paid, an expense is made by the business, therefore salary account is debited. On the other hand , when interest is received, an income is earned by the business, hence, interest received account is credited.

2. Rules Of Debit And Credit Based On The Accounting Equation

Accounting equation is a statement of equality between the three basic elements of accounting. They are assets, capital and liabilities. Each and every financial transaction affects the three basic elements. However, the total of all assets is always equal to the total of capital and liabilities at any point in time.

Accounting Concepts and Conventions

Accounting concepts and conventions evolved as a result of information needed by the users of accounting information which became conflicting over time because of different methodology or procedure used in its preparation .it was thereby adopted to ensure that accounting information is presented accurately and consistently.

Accounting concepts and conventions could be defined as ground or laid down rules of accounting that should be followed in preparation of all accounts and financial statements.

There are different kinds of accounting concepts and conventions

The concepts include

i. GOING CONCERN CONCEPT

Giving the fact that a business entity is solvent and viable this concept assumes the notion that the business unit will have a perpetual existence and will not be sold or liquidated

IT’S IMPORTANCE

It supports the use of historical cost concept in measuring assets such as; supplies equipments etc. that will be used in operation of a business. Without the Going concern concept accounts will be drawn up on a winding up basis.

ii. ENTITY CONCEPT

This concept states that every business unit not withstanding its legal existence is treated a separate entity from the body or bodies that owe it, this implies that its existence is distinct from its owner(s).

IT’S IMPORTANCE

It records and reflects the financial activity of the specific business organization and not of its owner(s) or employees. It is also important because it ensures that a company and its owner(s) can contract and sue each other incase of any misunderstanding arising in the future.

iii. MATCHING OR ACCURAL CONCEPT

This concept states that in an accounting period the earned income and the incurred cost which earned the income should be properly matched and reported for the period. This concept is also universally accepted in Manufacturing, Trading organization.

IT’S IMPORTANCANCE

Accrual concept attempt to correctly match all the accounting expenses (cost) to income (revenue) to the time it occurs at that accounting period. It also enables all revenue and expenditure of an accounting period to be recognized. It helps specify the profit of the organization in the accounting period.

iv. REALISATION CONCEPT

Realization concept encourages the periodic recognition of revenue as soon as it can be measured and the value of the assets is reasonably certain

In realization the revenue are realized in three basis

1. Basis of cash

2. Basis of sale

3. Basis of production.

ITS importance

It encourages the recognition of transaction and profit arising from them at the point of sale or transfer of ownership

v. HISTORICAL COST CONCEPT

This concept implies that all assets acquired, service rendered or received, expenses incurred etc. should be recorded in the books at the price at which it was acquired

(It’s cost price). The cost is distinct from its value and the record does not signify the value. It also holds that cost is the most reliable and verifiable value at which a good is or services should be initially recognized.

ITS importance

It allows the record of all transaction no matter how minute it may be before it might or might not be subjected to depreciation.

vi. DUAL ASPECT CONCEPT

This concept ensures that transaction are recorded in books at least in two accounts, if one account is debited it’s also credited with the same amount in a different account. The recording system is also known as double entry system. Assets = Liabilities + Capital.

vii. MONEY MEASUREMENT CONCEPT

This concept states that an item should not be recorded unless it can be quantified in monetary terms in other words it specifies that accountants should not record facts that are not expressed in money terms.

ITS importance

This concept could be said to be efficient because money enables various things of diverse nature to be added together and dealt with.

THE VARIOUS KINDS OF CONVENTION INCLUDE

i. CONSISTENCY: It states that accounting method used in one accounting period should be the same as the method used for events or transactions which are materially similar in other period (i.e. accounting practices should remain unchanged from period to period ). This also involves treatment of transaction and valuation method. Consistency is also advisable so that the comparison of accounting figures over time is meaningful. Consistency also states that if a change becomes necessary, the change and its effect should be clearly stated.

ITS importance

As stated by D.VICTOR consistency in accounting is an important assumption that facilitates comparability for information users. It also encourages reliability and fair presentation.

ii. MATERIALITY

According to AMERICAN ACCOUNITNG ASSOCIATION, an item should be regarded as material if there is reason to believe that knowledge of it would influence decision of informed investors. An item is also considered material if its omission or misstatement could distort the financial statement such that it influences the economic decision of users taken on the basis of financial statement.

ITS importance

It helps prevent records to be unnecessarily being over burden with minute details.

iii. PRUDENCE OR CONSERVATISM

This is an accounting practice that emphasizes great care in the anticipation of possible gains while possible losses are efficiently provided for. Prudence requires an accountant to attempt to ensure that the degree of success is not overstated. It also makes provision for possible bad and doubtful debts out of current year’s profit.

ITS importance

A strict application of prudence convention would ensure that profits and assets of the firm are not overstated.

iv. OBJECTIVITY

This convention states that the financial statement should be made on verifiable evidence.

ITS importance

It gives proof of a transaction in an objective manner in contrast to subjectivity or dependence on the verifiable opinion o the accountant preparing the financial statement.

v. DISCLOSURE

It states that information relating to the economic affairs of the enterprise which are of material interest should be clearly disclosed to the readers.

ITS importance

it discloses sufficient information which is of material in trust to owners,present and potential creditors and investors. It also helps the reader not to be misled in anyway by hearsay.

Ledger balance

The balance of a customer account as shown on the bank statement. The ledger balance is found by subtracting the total number of debits from the total number of credits for a given accounting period. The ledger balance is used solely in the reconciliation of book balances.

The ledger balance should not be confused with the customers available balance, which is the amount of funds available for withdrawal. The ledger balance includes any and all checks outstanding that have not yet cleared the account. This is partly why it differs from the available balance.

Trial balance

A trial balance is a list of all the General ledger accounts (both revenue and capital) contained in the ledger of a business. This list will contain the name of the nominal ledger account and the value of that nominal ledger account. The value of the nominal ledger will hold either a debit balance value or a credit balance value. The debit balance values will be listed in the debit column of the trial balance and the credit value balance will be listed in the credit column. The profit and loss statement and balance sheet and other financial reports can then be produced using the ledger accounts listed on the trial balance.

The name comes from the purpose of a trial balance which is to prove that the value of all the debit value balances equal the total of all the credit value balances. Trialing, by listing every nominal ledger balance, ensures accurate reporting of the nominal ledgers for use in financial reporting of a businesss performance. If the total of the debit column does not equal the total value of the credit column then this would show that there is an error in the nominal ledger accounts. This error must be found before a profit and loss statement and balance sheet can be produced.

The trial balance is usually prepared by a bookkeeper or accountant who has used daybooks to record financial transactions and then post them to the nominal ledgers and personal ledger accounts. The trial balance is a part of the double-entry bookkeeping system and uses the classic T account format for presenting values.

Rectification of Errors

In financial accounting, every single event occurring in monetary terms is recorded. Sometimes, it just so happens that some events are either not recorded or it is recorded in the wrong head of account or wrong figure is recorded in the correct head of account.

Whatever the reason may be, there is always a chance of error in the books of accounts. These errors in accounting require rectification. The procedure adopted to rectify errors in financial accounting is called "Rectification of error".

HOW TO RECTIFY THESE ERRORS

One way of rectification is that we can simply erase or overwrite the incorrect entry and replace it with the correct one. But this practice is not allowed in accounting. We have to Rectify / correct the mistake by recording another entry.

TYPES OF ERRORS

Before going to the rectification process, lets first see the different kinds of errors that can appear in our books of accounts:

ERROR OF OMISSION

One of the most common errors is that an event escapes recording. This means that an event occurred but we did not record it. For example, we discussed about bank charges being deducted by banks without our knowledge or our payments made by banks on our standing orders etc. There can be other reasons as well. Such errors are called ERRORS OF OMISSION.

ERROR OF COMMISSION

Then, there is a chance that the event is classified and recorded correctly but within wrong classification of account. For example, a payment to Mr. A, who is a debtor, is recorded in the account of Mr. B, who is also a debtor. Now the classification is correct but entry is posted in the wrong account. Such errors are called ERRORS OF COMMISSION.

ERROR OF PRINCIPLE

Then there are errors in which an entry is recorded in the wrong class of account. For example a purchase of fixed asset, say, a vehicle is recorded in an expense account. These errors are called ERRORS OF PRINCIPLE.

ERROR OF ORIGINAL ENTRY

The errors in which recording is in correct account but the figure is incorrect are called ERRORS OF ORIGINAL ENTRY. For example, a receipt of Rs. 50,000 from a debtor is recorded as Rs. 5,000 in his account.

Bank Reconciliation Statement

A Bank reconciliation is a process that explains the difference between the bank balance shown in an organisations bank statement, as supplied by the bank, and the corresponding amount shown in the organizations own accounting records at a particular point in time.

Such differences may occur, for example, because a cheque or a list of cheques issued by the organization has not been presented to the bank, a banking transaction, such as a credit received, or a charge made by the bank, has not yet been recorded in the organisations books, or either the bank or the organization itself has made an error.

It may be easy to reconcile the difference by looking at very recent transactions in either the bank statement or the organisations own accounting records (cash book) and seeing if some combination of them tallies with the difference to be explained. Otherwise it may be necessary to go through and match every single transaction in both sets of records since the last reconciliation, and see what transactions remain unmatched. The necessary adjustments should then be made in the cash book, or any timing differences recorded to assist with future reconciliations.

For this reason, and to minimise the amount of work involved, it is good practice to carry out such reconciliations at reasonably frequent intervals. Reconciliations are generally performed by specialised accounting software though the understanding of what occurs is important for a successful reconciliation. Also, Bank reconciliation statement is a statement prepared on a particular day to reconcile the bank balance as per Cash book or Bank statement showing entries causing difference between the two balances.

Cause of difference between cash book and pass book

Bank reconciliation means some of the transaction entered in the cash book not in the pass book and some transaction entered in the pass book not in the cash book. In other words we can say that always opposite entry in cash book and pass book. The bank pass book indicates the amount paid into the bank and the amount withdrawn there form. The pass book balance or any given data must be the same as the balance shown by the bank column of the cash book on the same date.The reason responsible for the difference may be delay in intimation, time gap between recordings of transaction in cash book and pass book due to errors and omissions in cash book and pass book.

Reasons of difference between cash book & pass book balance:

1. Cheque issued but not presented for payment: When cheque are issued then immediately make entry in the cash book. The cheque issued can be presented for payment to the bank within six month from the date of cheque as per banking law. The cheque are presented for payment after the expiry of the above period then payment is refused by the bank. This cheque is also known as stale cheque. It is posssible at the time when the balance of the two books are being compared, thus more chances of causing a disagreement b/w the two balances.

2. Cheque paid into the bank but not yet cleared: As soon as the cheque are deposited into the bank, the immediately entry is passed in the cash book. This will make entry in pass book only when cheque are cleared. It is posssible at the time when the balance of the two books are being compared, thus more chances of causing a disagreement b/w the two balances.

3. Interst allowed by the bank: Bank might have credited the account of the customer with the interest and may have made the entry in the pass book. It is possible that the entry of such interest may not have been made by the customer in the cash book, thus causing a disagreement b/w the two balances.

4. Interest and Bank charges debited by bank: Sometime bank charges interest from the customer then immediately entry in the pass book but not in cash book. so, in this case when check the balance b/w cash and bank book then disagreement b/w the two balances. So, it is the main reason to create difference b/w two books.

5. Interst, dividend collected by the bank: sometime interest on government security or dividend on share is collected by the bank and is credited to customer account. If the entry does not appear in the cash book then balance will differ.

6. Direct payment by bank: Sometimes, understanding instruction from the clients certain payment like insurance premium, club fees instalment etc. are made by the bank. then this entry is recorded only in the pass book. This entry is made in the cash book only when the necessary intimation to that effect is received from the bank by the client. The entries in the cash and pass book may be on different dates.

7. Direct payment into the bank by a customer: Sometimes, our customer deposit money direct into the account in the bank. It is only recorded in the pass book not in the cash book. It is posssible at the time when the balance of the two books are being compared, thus more chances of causing a disagreement b/w the two balances.

8. Dishonour of bill discounted with the bank: Sometimes, customer get their bills discounted with the bank. If the bank is not able to get payment of these bills on the due date. it will debit the customer account with the amount of the bills together with the nothing charges if any.The customer will pass the entry in the cash book only. when balance of the two books are being compared, thus more chances of causing a disagreement b/w the two balances.

9. Dishonour of cheque: When the received cheque are deposited into bank, these are immediately recorded in the cash book. As a result cash book balance is increased. but the deposited cheque is dishonoured due to lack of funds or due to other reasons. Bank doesnot credit the amount of the depositor. as a result disagreement b/w the two balances.

10. Error and ommissions: If any error is committed either by the bank or by a customer in the cash book While recording a transaction in their respective books, it causing a disagreement b/w the two balances. the error may be:

a) undercast/overcast of receipt side or payment side.

b) bank charges omitted from the banks or recorded twice in the books.

c) wrong carry forward of cash book balance.

Final Accounts of Sole Trader

Sole traders are people who are in business on their own: they run shops, factories, farms, garages, local franchises, etc. The businesses are generally small because the owner usually has a limited amount of capital to invest. Profits are often small and, after the owner has taken out drawings, are usually ploughed back into the business.

The final accounts (or financial statements) of a sole trader comprise:

a trading and profit and loss account which shows the profit or loss of the business a balance sheet, which shows the assets and liabilities of the business together with the owner’s capital These final accounts can be produced more often than once a year in order to give information to the owner on how the business is progressing. However, it is customary to produce annual accounts for the benefit of the Inland Revenue, bank manager and other interested parties. In this way the trading and profit and loss account covers an accounting period of a financial year (which can end at any date – it doesn’t have to be the calendar year), and the balance sheet shows the state of the business at the end of the accounting period.

Departmental Accounts

Departmental accounts are associated with a department rather than just an individual. Even if the owner of a departmental account leaves the university or transfers to a different department the account will remain active. Our goal is to make it easier for a department to retain accounts and just transfer ownership when the need arises. At the same time, we will always know who the current owner is if we need a contact for a departmental resource.

Modern life is very mechanical specially in big cities. The citizens of such cities expect all the goods and services just under a single roof. Contemplating the need of the consumers, the business men are also providing the expected service to the consumer just under a roof by opening large scale departmental stores. The departmental stores are the example of large scale retail selling just under a single roof. Different departments are involved for different goods to be sold out. To calculate the net result of the whole organization, a full fledged trading and profit and loss account is to be prepared. But to evaluate individual department, it will be credit worthy to prepare individual trading and profit and loss account. Such individual accounts will help to evaluate and control the different departments.

Objectives Of Departmental Accounting

The main objectives of departmental accounting are:

1. to check out interdepartmental performance

2. To evaluate the performance of the department with previous period result.

3. To help the owner for formulating right policy for future.

4. To assist the management for making decision to drop or add a department

5. To provide detail information of the entire organization

6. To assist management for cost control

A business entity where diversified natures of economic activities are undertaken is split into number of departments for accounting purposes. Generally it is management who will decide the number of departments in which the whole business is to be divided, but the criteria for identifying the departments in an examination question is always the separate sales/work-done revenue. Each department is considered as a profit centre, though none of the departments is separated geographically from the rest of the departments. This type of organizational subdivision creates a need for internal information about the operating results (profitability) of each department. Based upon the departmental knowledge of profitability and growth rate the management takes certain decisions e.g. pricing, costing, sales promotion, closure etc.

Allocation of Incomes and Expenses

Until unless the size of the business entity is very large, the entire book keeping system for the entity is kept by a central accounts department along with some departmental specific records e.g. sales, purchases, stocks and staff salaries etc. Rest of the operating expenses and other incomes need to be allocated among the departments based on their nature, utility, economic benefits and belongingness.

For allocation and division purposes the expenses/incomes can be categorized as:

1. Separately identified

2. Obvious just ratio

3. Specific ratio/sales ratio

4. Un-allocable