| ||

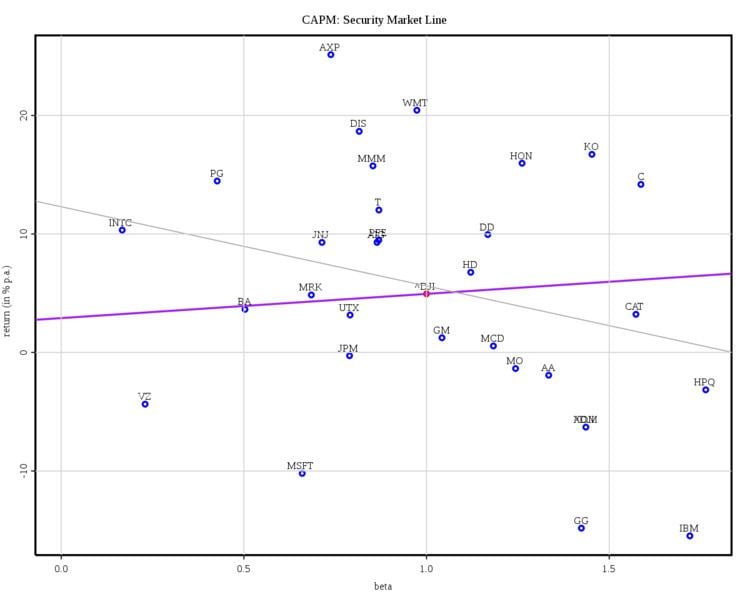

The low-volatility anomaly is that portfolios of low-volatility stocks have produced higher risk-adjusted returns than portfolios with high-volatility stocks in most markets studied. The capital asset pricing model made some predictions of return versus beta. First, return should be a linear function of beta, and nothing else. Also, the return of a stock with average beta should be the average return of stocks (this is easy to show given the first assumption). Second, the intercept should be equal to the risk-free rate. Then the slope can be computed from these two points. Almost immediately these predictions were challenged on the grounds that they are empirically not true. Studies find that the correct slope is either less than predicted, not significantly different from zero, or even negative. Also, additional factors are predictive of return independent of beta.

Black proposed a theory where there is a zero-beta return which is different from the risk-free return. This fits the data better since the zero-beta return is different from the risk-free return. It still presumes, on principle, that there is higher return for higher beta.

The low-volatility anomaly has now been found in the United States over an 85-year period and in global markets for at least the past 20 years.

Research challenging CAPM's underlying assumptions about risk has been mounting for decades. One challenge was in 1972, when Jensen, Black and Scholes published a study showing what CAPM would look like if one could not borrow at a risk-free rate. Their results indicated that the relationship between beta and realized return was flatter than predicted by CAPM.

Shortly after, Robert Haugen and A. James Heins produced a working paper titled “On the Evidence Supporting the Existence of Risk Premiums in the Capital Market”. Studying the period from 1926 to 1971, they concluded that "over the long run stock portfolios with lesser variance in monthly returns have experienced greater average returns than their ‘riskier’ counterparts".

The evidence of the anomaly has been mounting due to numerous studies by both academics and practitioners which confirm the presence of the anomaly throughout the forty years since its initial discovery. Examples include Baker and Haugen (1991), Chan, Karceski and Lakonishok (1999), Jangannathan and Ma (2003), Clarke De Silva and Thorley, (2006) and Baker, Bradley and Wurgler (2011).

For global equity markets, Blitz and van Vliet (2007),Nielsen and Aylursubramanian (2008), Carvalho, Xiao, Moulin (2011), Blitz, Pang, van Vliet (2012), Baker and Haugen (2012), all find similar results.