| ||

In finance an iron butterfly, also known as the ironfly, is the name of an advanced, neutral-outlook, options trading strategy that involves buying and holding four different options at three different strike prices. It is a limited-risk, limited-profit trading strategy that is structured for a larger probability of earning smaller limited profit when the underlying stock is perceived to have a low volatility.

Contents

- Short Iron Butterfly

- Limited Risk

- Break Even Points

- Example of Strategy

- Long Iron Butterfly Reverse Iron Butterfly

- References

Short Iron Butterfly

A short iron butterfly option strategy will attain maximum profit when the price of the underlying asset at expiration is equal to the strike price at which the call and put options are sold. The trader will then receive the net credit of entering the trade when the options all expire worthless.

A short iron butterfly option strategy consists of the following options:

where X = the spot price (i.e. current market price of underlying) and a > 0.

Limited Risk

A long iron butterfly will attain maximum losses when the stock price falls at or below the lower strike price of the put or rise above or equal to the higher strike of the call purchased. The difference in strike price between the calls or puts subtracted by the premium received when entering the trade is the maximum loss accepted.

The formula for calculating maximum loss is given below:

Break Even Points

Two break even points are produced with the iron butterfly strategy.

Using the following formulas, the break even points can be calculated:

Example of Strategy

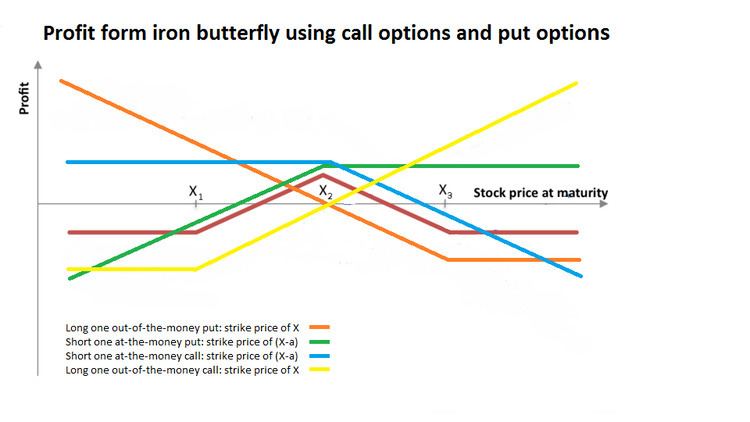

Long Iron Butterfly (Reverse Iron Butterfly)

A long iron butterfly option strategy will attain maximum profit when the price of the underlying asset at expiration is greater than the strike price set by the out-of-the-money put and less than the strike price set by the out-of-the-money call. The trader will then receive the difference between the options that expire in the money, while paying the premium on the options that expire out of the money.