| ||

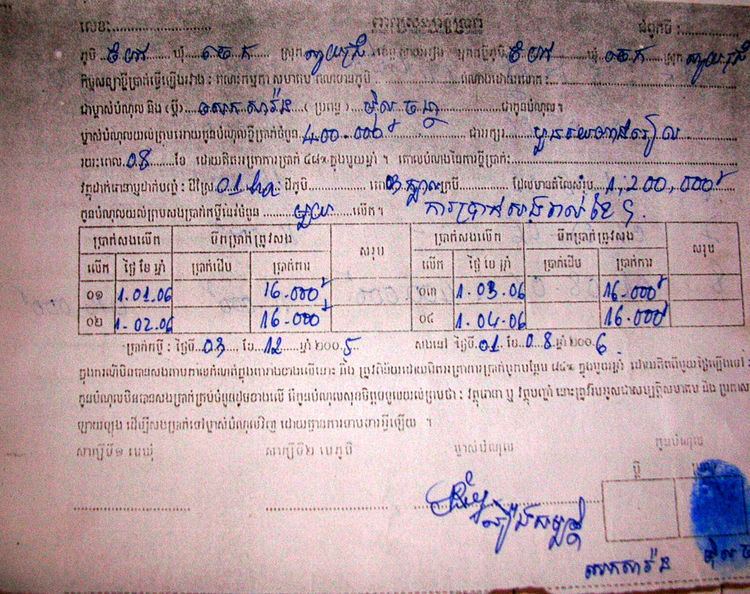

Flat interest rate mortgages and loans calculate interest based on the amount of money a borrower receives at the beginning of a loan. However, if repayment is scheduled to occur at regular intervals throughout the term, the average amount to which the borrower has access is lower and so the effective or true rate of interest is higher. Only if the principal is available in full throughout the loan term does the flat rate equate to the true rate. This is the case in the example to the right, where the loan contract is for 400,000 Cambodian riels over 4 months. Interest is set at 16,000 riels (4%) a month while principal is due in a single payment at the end.

Contents

Flat rate calculations

Loans with interest quoted using a flat rate originated before currency was invented and continued to feature regularly up to and beyond the 20th century within developed countries. More recently, they have also come to be used in the informal economy of developing countries, frequently adopted by microcredit institutions. One reason for the popularity of flat rates is their ease of use. For example, a loan of $1,200 can be structured with 12 monthly repayments of $100, plus interest, due on the same dates, of 1% ($12) a month, resulting in a total monthly payment of $112. However, the borrower only has access to $1,200 at the very beginning of the loan. Since $100 in principal is being paid each month, the average amount to which the borrower has access during the loan term is approximately half, in fact just over $600. For this reason, as mentioned above, the true rate of interest is nearly double. "A general rule known by financial managers is that when flat interest is used, the APR is almost twice as much as the quoted interest rate."

In order to show the true rate underlying a flat rate, it is necessary to use the declining balance amortization schedule, dividing the total cost to the borrower by the average amount outstanding. In the first three examples on the right the borrower is quoted 1% a month. These are loans of $1,200 each, amortized with level payments over 4, 12 and 24 months. In the 4-month example, the borrower will make four equal payments of $300 in principal and 4 equal payments of $12 (1% of $1,200) in interest. The total cost of this loan is the principal plus $48.00 in interest, whilst the average amount outstanding was approximately $600. This yields an annualized flat rate of 12%, and an annualized effective or true rate of 19.05%. The true rate can also be calculated by iteration from the amortization schedule, using the compound interest formula.

To keep quoted interest rates as low as possible, institutions also often call for one-time origination or administration fees. However, an origination fee as low as 4% of the total loan can have a large impact on the borrower's total costs. This is especially true for short-term loans, a typical characteristic of microcredit. As these fees represent an inherent cost of borrowing, they must also be added to the charge for interest in order to show the effective APR.

Benefits of flat rate lending

Flat interest rates have the following advantages:

Problems with flat rate lending

Flat interest rates have the following disadvantages:

Towards consumer protection in borrowing

The less developed an economy, the less capacity the government may have to regulate informal lenders. As a result, Brigit Helms argues for an evolutionary approach to interest rates, in which they can be expected to gradually drop as competition increases and the government gains greater capacity to effectively enforce comparable interest rate disclosures on financial sector actors.

F.W. Raiffeisen as early as 1889, writing to the credit unions then emerging in Germany, campaigned against maintaining the total charge for credit unchanged, even when a loan is repaid early. “It is immoral to charge interest in advance, and also objectionable as a business method. Every member shall have the right at any time to pay back his loan. If interest has been charged for a full year in advance, the members who have made repayments ahead of time, pay too much interest, unless the Credit Union makes a refund.”

Separately, interest rate ceilings and popular conflation of flat with true rates, has led some institutions to replace or complement interest with transaction fees and other charges, sometimes circumventing disclosure norms consistent with APR. For these reasons, interest is no longer quoted by reference to the flat rate in certain developed countries (for example, in the US, see the Truth in Lending Act), whilst many insist that loans always quote the APR.

Nevertheless, loans originally quoted and engaged with a flat rate remain contractually valid and still feature widely in both developed and developing countries.